Specialist in Asia Pacific, Japan, China, India and South East Asia and Global Emerging Market equities.

Discover moreformerly Realindex Investments

Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreInvestment strategies

Insights

At Stewart Investors, we believe in putting people first. Our investment world-view is of a series of partnerships – with each other, with our clients, with the companies we invest in, the people who buy their goods and services, and with the wider society in which we all live and work.

Discover more

Well, that question is a bit of a click-bait: like the holy grail itself, it probably doesn’t exist. Or at the very least, it is impossible to guarantee those specific outcomes in advance; investing in any stock entails too much uncertainty and that is precisely what the last two years have taught us.

At the very best, we can build a robust portfolio of stocks that approximates that ideal outcome. So going into 2022, how do we go about this?

Our starting point is to look backwards. Given how difficult the last two years were, it is tempting to move on and to forget that they existed. But it would be remiss of us as long-term investors not to reflect on the lessons that the COVID crisis taught us about dividend income investing.

Certainly some of the conventional wisdom regarding investing for dividends was challenged. And hopefully the lessons learnt will help income investors to develop a more resilient equity income investment strategy – one that better navigates different market outcomes and moves the focus beyond ‘the next dividend’.

Lesson 1: Dividends are discretionary payments, not annuities

When viewed over the long term, Australian shares have reliably paid a dividend yield around the 5% level. However, this meant little during the COVID crisis, when dividends where materially cut or even abandoned altogether with little warning.

This was a reminder whether a dividend is paid or not is entirely up to the discretion of the Board of Directors. Even companies that remained profitable cut dividends in the face of the uncertainty as Boards prioritised balance sheet strength over returning capital to investors.

Equity income investors often seek to overcome this inherent uncertainty by analysing financial statements for indicators of consistency. Examples of these metrics include dividend payout ratios, recurring revenues and free cashflow stability. The challenge is that this focus on reducing the uncertainty of discretionary dividend payments can encourage investors to only focus on the near-term outcomes and miss the potential longer-term opportunities for attractive income.

Lesson 2: High yield stocks are not necessarily lower risk

High yield stocks are not, by their nature, necessarily lower risk. This is contrary to conventional wisdom, as high yield stocks are often described as ‘mature businesses’ - the inference being their share prices are less volatile. COVID challenged this simple assumption. Many of these high dividend yield stocks were sold down aggressively and experienced large drawdowns after they announced dividend cuts. Those with longer memories may recall that the same situation played out during the global financial crisis in 2008.

Income focused investors often have a lower risk tolerance: without an income from work, they need to protect the capital they spent years building up. But accessing dividend income requires accepting the share price volatility risk of the underlying company, so this capital risk needs to be carefully managed.

Lesson 3: Dividend cuts are not always bad

Conventional equity investing tells us that a company doing well should be able to maintain a steady return of capital to investors. By this logic, when a company cuts dividends it must have done something wrong!

Perhaps this may be the case in the normal course of operations, but recent years were anything but normal. Companies that had robust balance sheets, such as James Hardie, sought to preserve capital in the face of the uncertainty and therefore cut dividends.

This allowed companies to remain flexible during a challenging period, avoid forced actions such as asset sales or capital raisings at depressed prices, and emerge a stronger company during the recovery. In the case of James Hardie, not only did it reinstate dividends in 2021 at a higher level on the back of stronger profitability, it was also able to pay a special dividend, in part to catch up on the ‘missed’ dividend payment.

This highlights that there may be occasions where dividend cuts can lead to better long-term outcomes, even for income-focused investors.

Putting these lessons into action in 2022

We believe income investors should focus on three things when designing their equity income strategy:

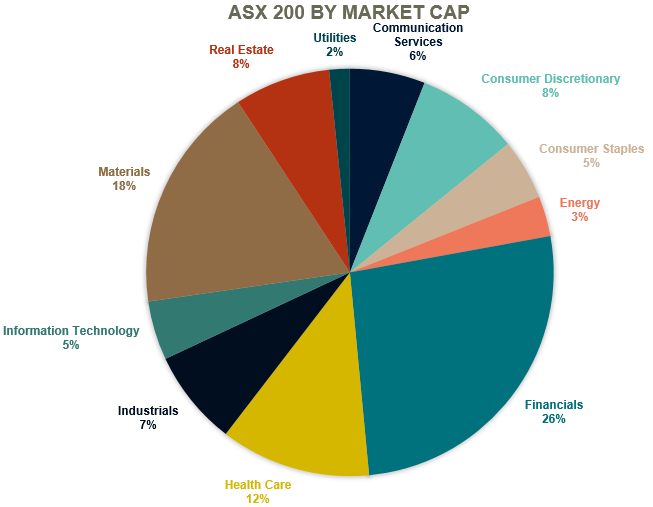

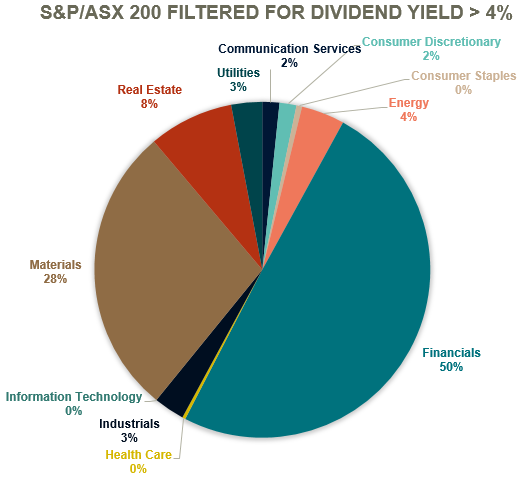

1. Build a resilient portfolio by avoiding concentrated risks – many of the high dividend yield stock names come from the same sectors. This can create three potential implications for investors. First, it can expose investors to concentrated sector risk. Second, in the longer term, portfolio returns could diverge from those of the broader share market as the investment is skewed towards a limited area of the market. Finally, restricting the size of the investible universe limits the opportunity to add value through active stock selection. The pie chart below illustrates how much more sector concentrated a portfolio becomes if we filtered for only higher yield stocks.

Source: Factset, Data as at 30 Nov 2021

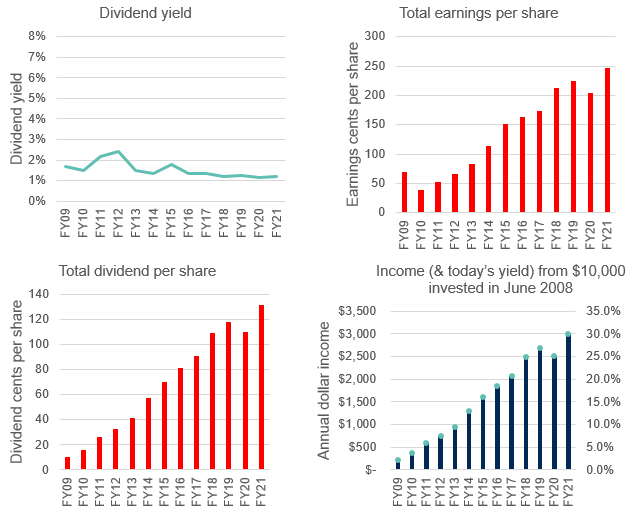

2. Avoid the temptation to screen/filter out low-dividend-yield stocks – We have written extensively about the need to distinguish between yield and income when thinking about generating income from equities, including previous Livewire pieces that you can read here and here. In short, we have shown that high-dividend-yield stocks do not ensure the generation of higher dividend income on a dollar basis over the long term. Attractive dividend income is actually delivered by the interaction of dividend yield and share price growth over time. The best way to understand this is to consider the example of REA Group (REA), the ASX-listed online property advertising business.

Source: REA Group Limited Investor and Analyst Presentation - Full Year Results June 2021, First Sentier Investors, IRESS, Factset. Total income over 13 years calculated assuming $10,000 is invested in June 2008.

REA is a stock that is typically ignored by income-focused investors due to its persistently low dividend yield. However, closer examination of the financial outcomes delivered to shareholders shows that the strong earnings growth has driven long-term income growth. Thought of another way, when we think about the income yield we are generating on an asset, we should measure this return using the price we paid to acquire the asset rather than the latest available price.

(Side note for property investors: When we think about the rental yield we are receiving on an investment property, we typically compare the annual rental income to the purchase price of the property. This is the most appropriate income measure. Using the latest available market price of the property is appropriate when we are seeking to determine the value of the asset, not measure the income return we are receiving.)

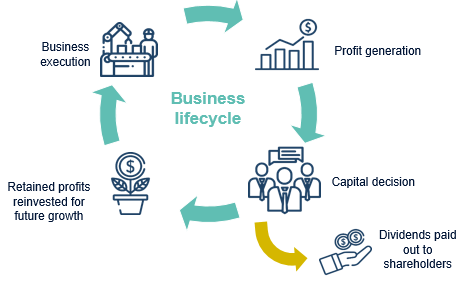

3. Return the focus back to company inputs, not outputs – When we simply focus on dividends, our attention is placed only on the output of the company. What drives the dividend outcome are the fundamentals of the business: how it generates a profit, what its operating environment is like; and the capital allocation decisions around paying a dividend and reinvesting in the business.

Returning to James Hardie as an example, the company decided that a lower dividend payout ratio is the optimal capital allocation decision to allow retained earnings to be reinvested in capacity expansion, new products, new geographies, brand building and continued research & development. This is highly relevant for income-focused investors because it’s this ‘business lifecycle’ that delivers the long-term, growing dividend income stream desired by shareholders.

Source: First Sentier Investors

But what if I want the higher income now in 2022?

You may have noticed that one common theme of the three suggested actions above is a focus on long-term outcomes. But the reality is that many investors need income in the ‘here and now’.

To achieve this, we believe a carefully implemented options strategy can generate a third stream of income (after dividends and franking credits). Together, these three sources of income offer the opportunity to generate above market income distributions through all market conditions.

Learn more in 2022

The disruption of the last two years has highlighted that the future is hard to predict, so investors need a strategy that cushions the downside, and helps to navigate an uncertain market outlook. This equity income approach allows an investment portfolio to be constructed based on fundamental research that identifies the best opportunities across the market, regardless of a stock’s dividend yield.

This article originally appeared on Livewire Markets as part of their 2022 Outlook Series.

Still curious? Hear more from our Equity Income team:

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (Author). The Author forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for the Author is available from First Sentier Investors on its website.

This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are the opinions of the Author only and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product.

To the extent permitted by law, no liability is accepted by MUFG, the Author nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that the Author believes to be accurate and reliable, however neither the Author, MUFG, nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of the Author.

|  |

|---|