At AlbaCore, we focus on the long-term. As one of Europe’s leading alternative credit specialists, we invest in private capital solutions, opportunistic and dislocated credit, and structured products.

Discover moreInvestment strategies

Insights

Specialist in Asia Pacific, Japan, China, India and South East Asia and Global Emerging Market equities.

Discover moreOur philosophy is very simple. We are constantly searching for high quality businesses and when we acquire them, we will work relentlessly with them to create long-term sustainable value through innovation, ESG-led and proactive asset management.

Discover moreInvestment strategies

Insights

formerly Realindex Investments

Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreInvestment strategies

Insights

At Stewart Investors, we believe in putting people first. Our investment world-view is of a series of partnerships – with each other, with our clients, with the companies we invest in, the people who buy their goods and services, and with the wider society in which we all live and work.

Discover more

We recently reviewed the Neutral Asset Allocation (NAA) for the First Sentier Multi-Asset Real Return Fund; an exercise that is undertaken twice a year. This note summarises the key drivers of investment markets over the most recent six month period and outlines the changes made to the NAA following this most recent formal review.

Just as a recovery from the Covid-19 pandemic lockdowns appeared to be an optimistic turning point, financial market volatility has intensified across all asset classes, exacerbated by rising inflation, interest rate hikes and a deteriorating growth outlook.

We have continued to closely monitor these themes since our last NAA review and have adjusted our allocations accordingly, as reflected in the below table.

What exactly is the NAA review?

The first step in our investment process is to determine the economic outlook, both globally and for individual countries. Twice a year, we formally review existing assumptions and determine the likely long-term values for inflation, risk free rates, long-term bond yields, and earnings growth.

Using the current valuations as a starting point, these detrminations enable us to calculate expected returns for various asset types globally. In turn, this helps inform the most appropriate mix of investments (NAA) that have the highest likelihood of achieving the Fund's long-term objectives.

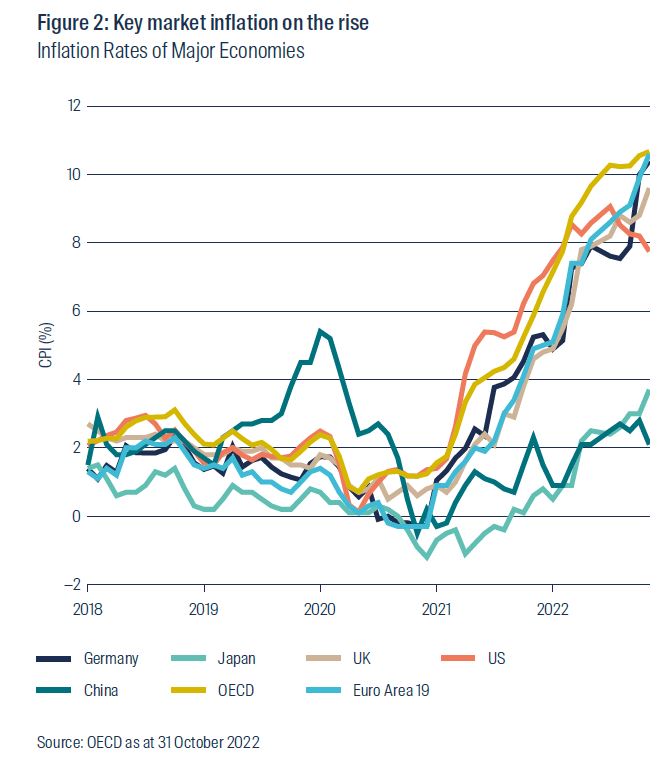

Central bankers continue the fight against inflation

It has been no secret that inflation has been a hot topic in 2022 across most major markets. While the Covid-19 pandemic related disruptions and the associated pent-up demand were initially to blame for the rising costs of living, the transitory narrative from central bank officials quickly changed tune when it became evident that without action, these pressures would likely linger. Beyond the recovery from the pandemic, the conflict in Ukraine has also contributed to these indicators rising. The European energy crisis – a by-product of the conflict in Ukraine – has seen the cost of energy in both Europe and the UK become a heavy burden. As we have seen, however, this problem is not unique to Europe.

US inflation rose at an annual pace of 7.7% for the year to October 2022 and had been rising quickly for most of the year, reaching an annual pace of 9.1% in June before starting to trend lower. While fortunately this change in direction may signal that the work of central bankers in quantitative tightening has started to have its desired effect, these readings are still significantly above the US Federal Reserve’s target of 2%.

While investor speculation suggests that the peak inflation rate for the US has passed, the same case is not yet evident in Europe and the UK. While increasing cash rates is driving caution among some investors, central bankers still appear committed to monetary policy tightening in order to regain control.

Where to from here?

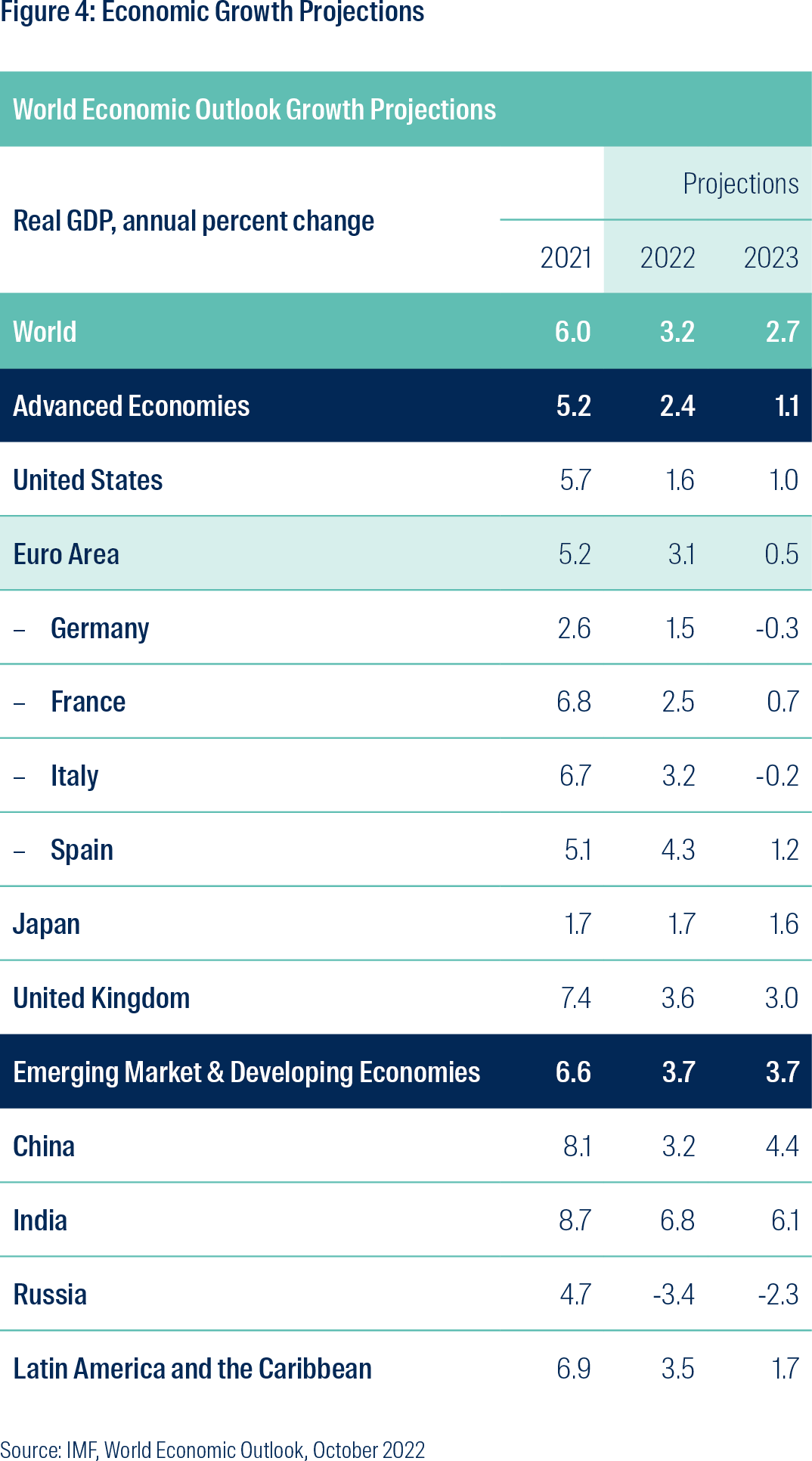

Widespread volatility was a feature of global markets this year, we expect this to continue in 2023 and bring ongoing dispersion of returns and greater investment opportunities. In particular, we note that higher interest rates can be beneficial for fixed income and corporate bond investors through higher income. Having said that, we also recognise the prospect of increased exposure to duration in a rising rate environment can erode some of the attractiveness of this asset. In corporate debt markets, defaults are increasing from historically low levels and are expected to reach long term averages, with Europe and emerging markets leading the way. The market however has already priced this in and we took advantage of the credit spreads widening earlier this year to add a duration-hedged exposure to Investment Grade Credit. We are retaining this exposure into 2023, including hedging out the duration risk.

Meanwhile, repricing in equity markets in recent months is leading to pockets of valuation opportunities emerging. However, these opportunities need to be considered in the context of ongoing volatility and the potential for deteriorating economic conditions. Global markets have seen selloffs and while valuations are more attractive than they were at this time last year, we are taking a cautious approach into 2023 and hold a slight underweight position to equities relative to our neutral view.

Within equities, we continue to view Australian equities as more attractive than global, which results in retaining an even split between these allocations. This has been a positive outcome since the beginning of 2022 as Australian equities have outperformed global equities on a relative basis. Year to date, emerging market equities have underperformed developed; weighed by higher inflation, financial conditions and a strong US dollar. More specifically, China’s ongoing zero-Covid policy continues to drag on economic growth and although there seem to be signs of this strategy coming to an end, how exactly this will play out remains unclear. Despite uncertainties relating to Chinese Covid-19 policies, valuations in these markets appear more attractive in a historical sense, and so we have sought further diversification within equities by reintroducing a small allocation to emerging markets. We are retaining all currency exposures from global equity allocations to provide diversification in a risk off scenario but will review this regularly as currency divergence is increasing relative to recent years.

We expect central banks to continue to implement quantitative tightening measures, including increasing interest rates in 2023 – albeit in smaller increments than in 2022 – as evidence of inflation growth remains but continues to plateau. While tightening has resulted in downward pressure exerted on equity valuations, corporate balance sheets have so far remained solid. Recession warnings have been gaining momentum, particularly as the US 2-year and 10-year yield curve spent a large portion of the year inverted – a phenomenon often viewed as a recessionary indicator.

Nonetheless, most recent macroeconomic data releases have not been as dire and so we remain cautiously optimistic into the new year. Thankfully, the flexibility of our objective-based strategies allows us to mitigate these risks and balance short-term dynamics with longer-term views, particularly relative to a static benchmarked approach to asset allocation.

Key Points from our Neutral Asset Allocation Review

The setting of the economic climate involves deciding on where we think the global economy is moving, and then for each country we determine the likely long-term values for inflation, risk free rates, long-term bond yields and earnings growth. By taking current valuations as a starting point, this allows us to determine expected returns for global assets from this point forward.

- Overall, we have made modest changes to the Neutral Asset Allocation. Our economic climate assumptions continue to evolve in response to the ongoing recovery from the Covid-19 pandemic, the implications of the conflict in Ukraine (particularly for Europe), the elevated levels of inflation and the impact of tightening monetary policy.

- In a rising interest rate environment, both fixed income and equity returns have experienced an increase in volatility. Our analysis suggests that most asset classes have slightly higher expected returns, driven predominantly by higher interest rates. Our volatility expectations have not meaningfully changed.

- Across the last three reviews, we have adjusted our inflation assumptions higher across all markets and anticipate higher interest rates and long-term bond yields to combat this. We removed the neutral allocation to global bonds in May 2022 due to this environment, however, given materially higher yields these assets have regained some of their attractiveness as part of this review. That said, we did not reintroduce long dated global bonds to our neutral allocation at this time. While the rate of interest rate hikes appears to be slowing; ultimately, they are expected to rise further and short term yields offer a similar yield without the term premium risks.

- While we are averse to an increase in the portfolio’s duration, we do remain cautious about the current environment. The reduction in Covid-19 lockdown measures has been positive for corporate earnings however, increasing costs of living and borrowing costs can be a concern for companies.

- As a result, we have increased the neutral allocation to cash by 10%. We have reduced our allocation to both Australian and Global Developed equities in order to support this reallocation. We have also reintroduced a small allocation to Global Emerging Market equities of 2%. This allocation provides the portfolio with an increase in diversification, but keeps the portfolio’s exposure between Australian and Global assets evenly split.

- Rising rates will put pressure on equity valuations and to provide diversification, all of the Fund’s global equity exposure is currently unhedged. This should provide a buffer in case the Australian dollar continues to weaken.

How do we determine the right mix of NAA (beta) and Dynamic Asset Allocation (DAA or alpha)?

Based on our assumptions for the economic climate, and our expected returns, we can determine the likelihood of meeting the portfolio’s objectives over the investment horizon. It is becoming increasingly likely that relying solely on the NAA in a constrained long only, unlevered environment will not be sufficient to meet the return objectives. This is where we use our DAA process, which takes shorter-term market dynamics into account and aims to deliver additional returns, as well as mitigate portfolio risks. By adding an uncorrelated return source (alpha) we can improve the likelihood of meeting the Fund’s investment objectives.

The combination of NAA and DAA requires the consideration of the current allocations; as the extent to which active management may be used is managed through the portfolio’s risk budget to avoid unwanted additional risks. We consider both the tracking error (as well as other risk metrics) and the expected return, in assessing the portfolio’s ability to meet its investment objective. The ability to add scalable alpha to portfolios provides flexibility to deliver on the investment objective; even in a lower return environment.

In the current low return environment it is critical to have the flexibility to blend beta and alpha to deliver a real return of 4.5% pa above inflation over rolling five year periods before fees and taxes. We believe our investment process and philosophy provides our clients the highest possibility of obtaining a real return and expect the DAA process to be of paramount importance given the current outlook for major asset classes.

Disclaimer

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (FSI AIM), which forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for FSI AIM is available from First Sentier Investors on its website.

This material is directed at persons who are ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) (Corporations Act)) and has not been prepared for and is not intended for persons who are ‘retail clients’ (as defined under the Corporations Act). This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation.

The product disclosure statement (PDS) or Information Memorandum (IM) (as applicable) for the First Sentier Multi-Asset Real Return Fund, ARSN 161 207 165 (Fund) issued by Colonial First State Investments Limited (ABN 98 002 348 352, AFSL 232468) (CFSIL), should be considered before deciding whether to acquire or hold units in the Fund(s). The PDS or IM are available from First Sentier Investors. The target market determination (TMD) for the Fund is available from First Sentier Investors on its website and should be considered by prospective investors before any investment decision to ensure that investors form part of the target market.

MUFG, FSI AIM, their respective affiliates and any service provider to the Fund do not guarantee the performance of the Fund or the repayment of capital by the Fund. Investments in the Fund are not deposits or other liabilities of MUFG, FSI AIM, their respective affiliates or any service providers to the Fund and investment-type products are subject to investment risk including loss of income and capital invested.

Any opinions expressed in this material are the opinions of the individual author at the time of publication only and are subject to change without notice. Such opinions: (i) are not a recommendation to hold, purchase or sell a particular financial product; (ii) may not include all of the information needed to make an investment decision in relation to such a financial product; and (iii) may substantially differ from other individual authors within First Sentier Investors.

To the extent permitted by law, no liability is accepted by MUFG, FSI AIM nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that FSI AIM believes to be accurate and reliable, however neither MUFG, FSI AIM nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of FSI AIM.

Any performance information has been calculated using exit prices after taking into account all ongoing fees and assuming reinvestment of distributions. No allowance has been made for taxation. Past performance is not indicative of future performance.

Copyright © First Sentier Investors

All rights reserved.

|  |

|---|