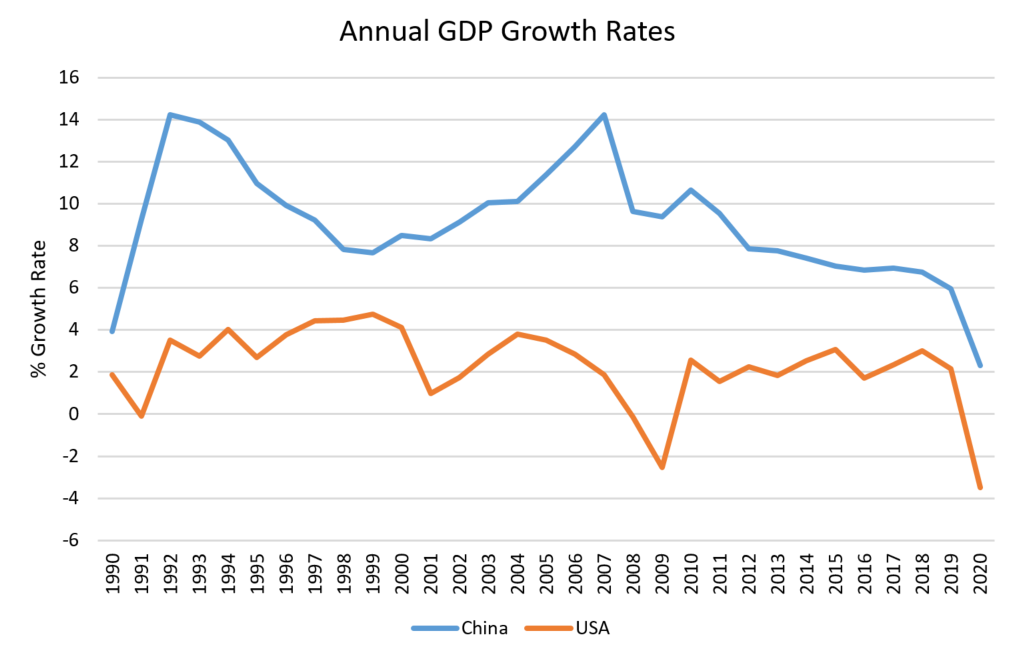

Over the last 5 years, China has been on the rise within the Emerging Markets. We have all heard the story of the China Dragon and the impressive growth that the Chinese economy has been able to achieve relative to other large economies since the early 1990s (see chart below). Even more recently as its growth has reduced it is still achieving more than double the growth of the United States.

Source: World Bank, Realindex, data as at 31 December 2020.

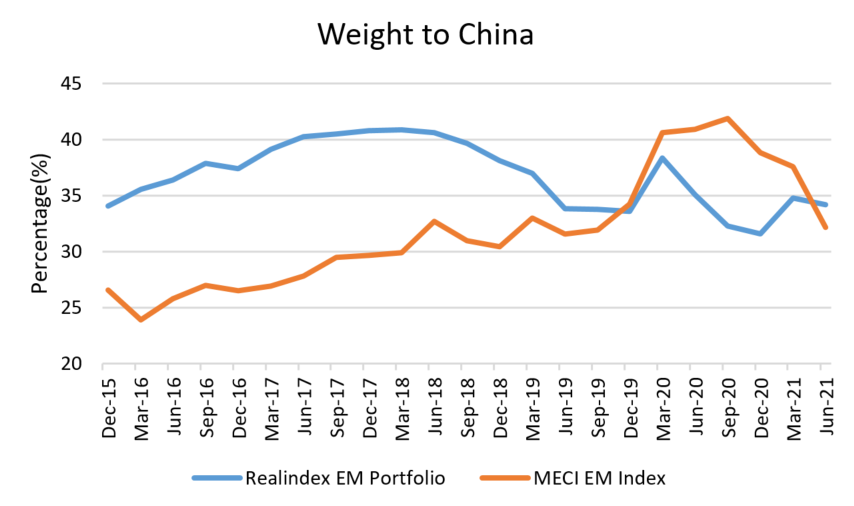

This dominance has also been reflected in the importance of China within the Emerging Markets. At the beginning of 2016 it had a weight of 26.5% in the MSCI Emerging markets index, by September 2020 this had grown to just under 42%. Yet in the last 10 months we have seen that fall back to under 30%. What has this fall of close to 30% in its weight within the index been attributed to?

We believe the increase in regulatory risk from both the US and domestically in China has been a large contributor to this fall. The question for investors is this: will it continue and where does the next risk lie?

- We believe that the US will continue to place pressure via its sanctions and disclosure requirements.

- We believe that we are likely to see some further regulation domestically from China as they seek to ‘grow sustainable’.

- We are therefore likely to still see some big falls in individual Chinese stocks when the final version of the regulation is revealed.

Regulations from both sides - US and China

There are two forces of regulation that are having an impact on the Chinese market at the moment- internationally from the US and domestically via the Chinese government.

The US has issued sanctions targeting those companies that it views as being connected to the Chinese Military and intelligence services and that pose a potential threat to the US homeland and US forces overseas. These sanctions have gone through a number of iterations between the Trump and Biden administrations. The latest, Executive order 140321, sanctions only those companies specifically named in the order. This was a slight change to previous orders (EO 139592) which had included all related companies. This list however has been extended beyond the initial Chinese military industrial complex to also include a greater emphasis on human rights via targeting surveillance companies. These orders stop US citizens from holding these companies after a certain date and have resulted in a number of the companies being removed from major global stock indexes. For further details see Realinsights - Sanctions3

Beyond the companies that have been named in these orders, the US has also signed into law the Holding Foreign Companies Accountable Act4. This requires publicly listed companies in the US to declare they are not owned or controlled by a foreign government. They are also required to submit to an audit that can be reviewed by the Public Company Accounting Oversight Board. If they do not comply over a 3 year period they can be delisted in the US. At present many listed Chinese companies do not comply with these audit regulations as access to China based audit work papers is refused for fear of violating China’s State secrecy laws. For further details please see Realinsights - Forced Delisting of Chinese ADRs from US Exchanges –Is a market dislocation coming?5

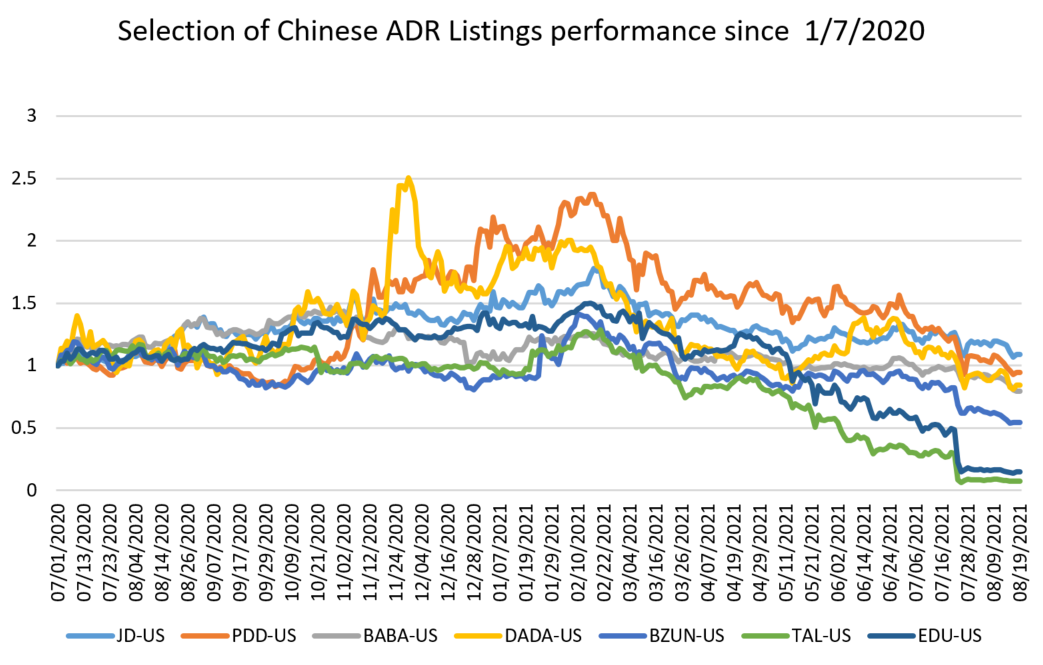

These laws will have a greater impact in the internet and technology sectors which have a large number of Chinese ADRs listed in the US. There continues to be messaging from the SEC6 regarding the disclosure from these companies and we have seen this pressure reflected in the pricing of a number of the ADR’s since the start of this year (see below). These have fallen between 20% and 80% since their height in February this year.

Source: Factset, Realindex, data as at 19 August 2021.

Increased local listings

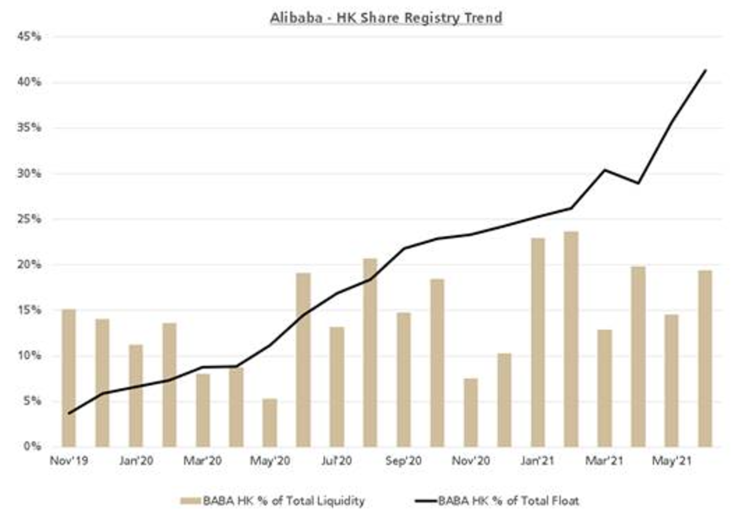

We have recently seen an increase in those companies with ADR listings subsequently listing back in Hong Kong (e.g., New Oriental Education & Technology (Nov 2020), Baidu (Mar 21), Alibaba (Nov 19), JD.com (Jun 20) and Baozun (Sep 20)). This increase in local listings is due to a number of reasons including

- The improvement in the Chinese domestic regulatory framework.

- Concerns in relation to the use of the VIE (variable interest entity structure7).

- Increased US regulations on Chinese listed companies.

Companies are starting this listing process now as it allows them enough time for the liquidity in the HK line to increase to the level required to be swapped as the official line for the index providers. We have already seen this occur for Alibaba where MSCI moved the official benchmark from the ADR line to the HK listing earlier this year. Whilst the US line still has plenty of liquidity, we can see in the chart below the increasing proportion of the float in the HK line compared to the US line.

Source: UBS, Bloomberg, CCASS

Finally, effective January 13 2021, the US has also issued a Withhold Release Order (WRO) for all cotton and tomato products produced in China’s Xinjiang Uyghur Autonomous region. A WRO is made under the Tariff Act of 1930 and is against the importation of goods determined to be mined, produced or manufactured in whole or part by the use of forced labour. This is in response to the issue of ‘forced labour in Xinjiang, where the Chinese government continues to execute a campaign of repression targeting the Uyghur people and other ethnic and religious minority groups’8. Whilst this will also impact many US companies that rely on this cotton (as this region produces 20% of the world’s cotton), this will impact the export businesses of many Chinese apparel companies.

What about domestic Chinese regulation?

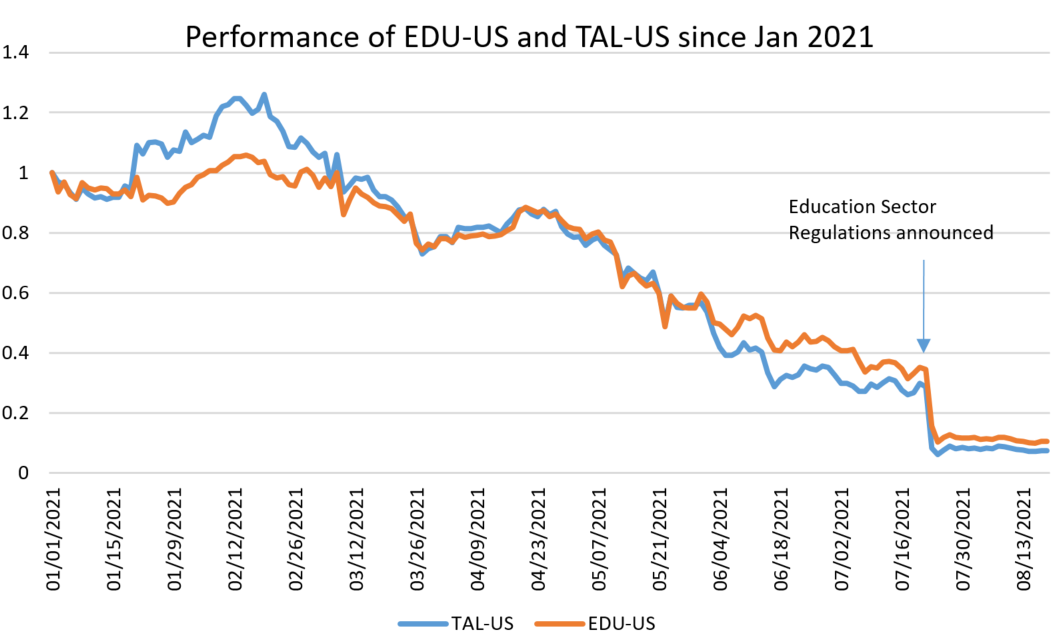

Recently we have seen what some have termed a ‘regulatory reset’ from China with a focus on balancing both growth and sustainability. This has led to an increase in regulation on some of the largest growth areas in China – fintech, big tech, after-school tutoring and internet platforms. This has resulted in some very large stock price falls as these new regulations have been announced. Most recently we have seen falls in the after-school tutoring stocks when China announced that companies were not to profit in the provision of services for core school subjects. Two companies impacted by this, EDU-US and TAL-US, had falls of approx. 70% over a two day period.

Source: Factset, Realindex, data as at 13 August 2021.

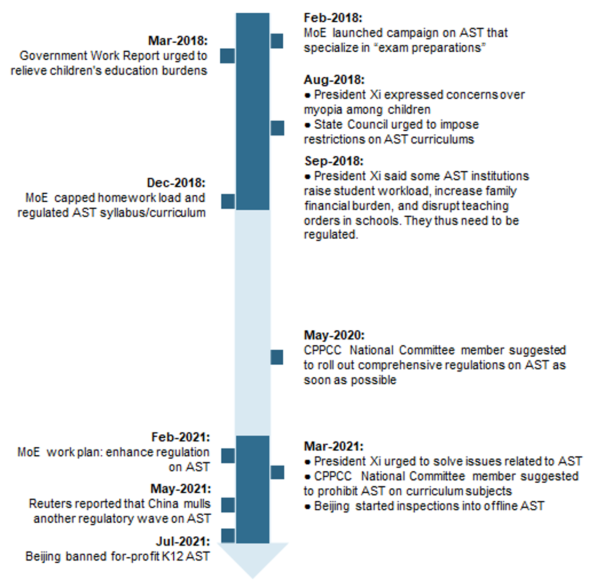

Although the exact form of the regulation may have come as a surprise, there had been suggestions of increased regulation in this sector for a period of time. A case study put together by Morgan Stanley9 shows that there has been increased scrutiny since 2018 from the Chinese authorities.

Exhibit 19: Case study: origin and develop of after-school tutoring (AST) regulation

Source: Morgan Stanley Research

This sector was put on notice back in 2018 with increased focus earlier in 2021. This is not to say that we can determine exactly what China is going to do before it is announced, but with most sectors that have experienced increased regulation, there has been a period of increased focus and scrutiny on the sectors by the Chinese government before any new regulation is announced. Often this scrutiny has followed an extended boom period in the sector e.g. regulation on mining (2006-2009), on dairy (2008-2010) and more recently gaming in 2018.

Is regulatory risk priced into Chinese stocks? The EDU-US and TAL-US examples show us that although some risk has been priced in (with the steady declines since January) there is still the market surprise once the announcement is made. This can mean a continued risk for these growth stocks and sectors under scrutiny.

With an increased focus on balanced growth and sustainability we expect there to be a focus on healthcare, semiconductors, decarbonisation and a continued check on the rise in corporate power. Why these sectors? China is looking to reduce its reliance on the US and acknowledging the importance of technology in any future growth, it will want to favour the domestic semi-conductor industry. As the population ages, it will want to make sure that all income groups can have access to the new therapies and drugs and hence the focus on the healthcare sector. China has also acknowledged the increasing environmental risk and we have already seen mandates on electric vehicle production by the Chinese government. We believe there will be continued focus on these sustainable industries and the promotion of renewable power development.

This check on corporate power, the increased tension between the USA and China as well as the increased scrutiny on the ability of companies to list overseas has also put increased light on the VIEs structures currently used. As these are prominent in many of the internet and telecommunications names, the recent growth in these companies has probably heightened the regulatory risk on them.

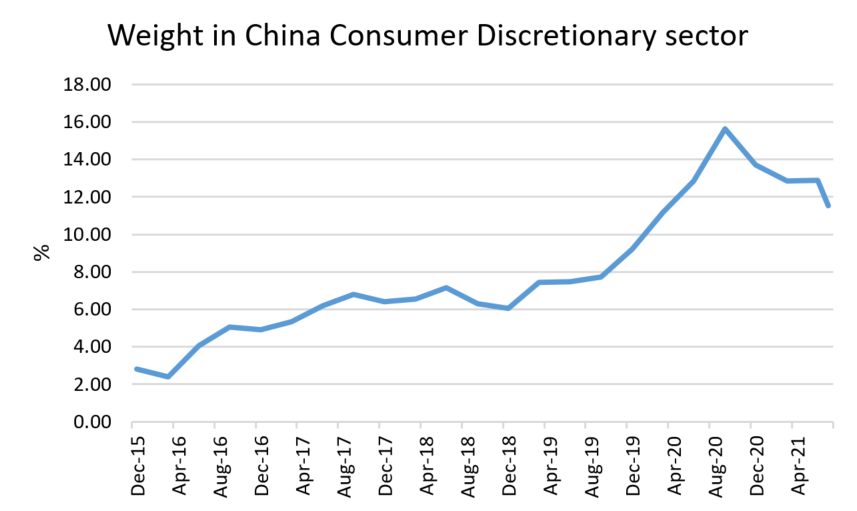

How much have they grown? If we look at the weight of the consumer discretionary sector within the emerging markets universe, which is where most of these internet stocks are classified, it has grown from 2.81% of the universe at the start of 2016 to above 15.5% by September 2020. There has subsequently been significant falls in these stocks with their weight just over 11.5% at the end of July 2021. As shown below since February 2021, some of these stocks have fallen by more than 50% as the increased threat of regulation starts to be priced in.

Source: Factset, Realindex, data as at 31 July 2021.

We have seen further regulation on data security with the passing of the Data Security law (to be implemented on September 1 2021) and the Personal Information Protection law which is to be implemented on 1 November 2021. The Data Security laws sets a framework for companies to classify data based on its economic value and relevance to China’s national security and the Personal Information Protection law sets a framework for user privacy10. These regulations are likely to further limit tech platforms’ perceived abuse of market power which is a continuation of the anti-trust regulation that was published in February.

Is there a way to reduce this regulatory risk? Monitoring the information from China helps but given the focus on balanced growth and sustainability, this provides some idea of the sectors to focus on that are likely to have less regulatory risk. They also are potentially likely to be promoted versus some of the big tech growth companies where we have seen significant price growth over the years.

How do you achieve this reduced regulatory risk? Market cap indices are susceptible to concentration bias11, and will, by their nature, tend to overweight expensive stocks and underweight cheaper stocks, embedding growth and momentum styles to the investment. This is likely to lead to a greater risk in being caught up in stocks exhibiting ‘unbalanced’ growth. It is also vulnerable to pricing bubbles, where prices are unsustainably high, and subsequent corrections which is what we are seeing within these internet sectors.

The Realindex Emerging Markets Fund looks to weight stocks based on metrics that reflect company size but are not correlated with prices. The core components it considers when calculating weights for the stocks are adjusted sales, adjusted book value, cash flows and dividends. By its nature this makes it value-tilted relative to the cap weighted benchmark but this is an outcome not a goal. Like a cap weighted index, it has the positive aspects of index investing (systematic, lower cost and lower turnover) but not the unintended exposure to expensive stocks. Over time its exposure to China has been relatively consistent as it seeks to reflect the importance of China by economic size. This has helped it avoid some of the bubbles in sectors that we have recently seen within China.

Source: Factset, Realindex, data as at 31 July 2021.

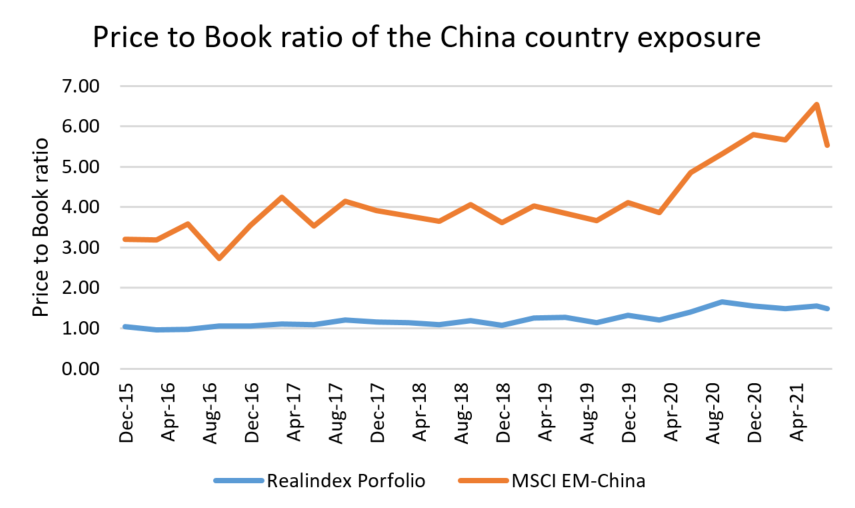

We can also see this difference if we look at the Price to Book12 valuation metric of China country exposure within the MSCI EM vs China in the Realindex Emerging Markets Fund. Whilst the Realindex Emerging Markets Fund has a fairly consistent Price to Book metric we can see that the MSCI EM-China exposure has risen especially since March 2020 showing the increasing influence the growth, or more expensive, stocks have had on the index.

Source: Factset, Realindex, data as at 31 July 2021.

Conclusion

We will continue to monitor the news out of China as the tussle between the US and China continues. We do not believe the current Biden administration will back down from some of the policies implemented under the Trump administration in this area and we believe that China will continue to look domestically as it seeks to reduce its reliance on the US. We believe this is likely to have a continued influence of individual stock names as well as the significance of China within the Emerging Markets.

References

- https://www.federalregister.gov/documents/2021/06/07/2021-12019/addressing-the-threat-from-securities-investments-that-finance-certain-companies-of-the-peoples

- https://www.federalregister.gov/documents/2020/11/17/2020-25459/addressing-the-threat-from-securities-investments-that-finance-communist-chinese-military-companies

- https://www.firstsentierinvestors.com.au/au/en/institutional/our-funds/realindex-investments/realinsights.html

- https://www.congress.gov/bill/116th-congress/senate-bill/945

- Ibid.

- https://www.sec.gov/news/public-statement/gensler-2021-07-30

- A Variable Interest Entities (VIE) is a structure where an operating company typically establishes an offshore shell company in another jurisdiction, such as the Cayman Islands, to issue stock to public shareholders. That shell company enters into service and other contracts with the operating company, then issues shares on a foreign exchange, like the New York Stock Exchange. While the shell company has no equity ownership in the operating company, for accounting purposes the shell company is able to consolidate the operating company into its financial statements. This arrangement creates exposure to the operating company through a series of service contracts and other contracts but does not provide ownership in the underlying operating company

- https://www.cbp.gov/newsroom/national-media-release/cbp-issues-region-wide-withhold-release-order-products-made-slave

- Global Insight, China’s Regulatory Reset, Morgan Stanley, August 1, 2021

- https://www.reuters.com/world/china/china-passes-new-personal-data-privacy-law-take-effect-nov-1-2021-08-20/

- This refers to a few stocks making up a large percentage of the index weight.

- A valuation metric that compares a company’s market capitalisation with its book value.

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (FSI AIM, Realindex), which forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for FSI AIM is available from First Sentier Investors on its website.

This material is directed at persons who are ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) (Corporations Act)) and has not been prepared for and is not intended for persons who are ‘retail clients’ (as defined under the Corporations Act). This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation.

The product disclosure statement (PDS) or Information Memorandum (IM) (as applicable) for the Realindex Emerging Markets Fund ARSN 140 973 075 (Fund), issued by Colonial First State Investments Limited (ABN 98 002 348 352, AFSL 232468) (CFSIL), should be considered before deciding whether to acquire or hold units in the Fund(s). The PDS or IM are available from First Sentier Investors.

MUFG, Realindex, their respective affiliates and any service provider to the Fund do not guarantee the performance of the Fund or the repayment of capital by the Fund. Investments in the Fund are not deposits or other liabilities of MUFG, Realindex, their respective affiliates or any service providers to the Fund and investment-type products are subject to investment risk including loss of income and capital invested.

Any opinions expressed in this material are the opinions of the individual author at the time of publication only and are subject to change without notice. Such opinions: (i) are not a recommendation to hold, purchase or sell a particular financial product; (ii) may not include all of the information needed to make an investment decision in relation to such a financial product; and (iii) may substantially differ from other individual authors within First Sentier Investors.

To the extent permitted by law, no liability is accepted by MUFG, Realindex nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that Realindex believes to be accurate and reliable, however neither MUFG, Realindex nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of Realindex.

Any performance information has been calculated using exit prices after taking into account all ongoing fees and assuming reinvestment of distributions. No allowance has been made for taxation. Past performance is not indicative of future performance.

Copyright © First Sentier Investors, 2021

All rights reserved.