Andrew Greenup and George Thornely explore the performance of the Global Listed Infrastructure Securities asset class and look ahead to the main themes expected to impact this asset class over the years ahead.

Introduction

The past decade has witnessed the birth of a new asset class: Global Listed Infrastructure Securities (GLIS). While investors have embraced infrastructure as an asset class since the 1990s, the idea of investing in infrastructure via listed securities was developed by a small number of Australian asset managers in 2005-2007.

GLIS is now widely acknowledged as a standalone asset class by asset consultants, investors and the funds management industry. Today we estimate funds under management in GLIS to stand at around US$100 billion; not bad from a standing start just over a decade ago. This paper1 reviews the performance the asset class has achieved for investors so far;2 analyses the steady increase in investible assets;3 reviews major trends that have affected GLIS thus far and4 looks ahead to the main themes we expect will impact GLIS over the years ahead.

Performance is everything

GLIS provides investors with a liquid and globally diversified means of gaining exposure to essential service infrastructure assets. These assets are relatively uncorrelated with other asset classes, provide investors with inflation linked income and have the potential for modest capital growth. GLIS has become a successful standalone asset class because its risk-adjusted investment returns have exceeded investors’ expectations.

Use of GLIS within investor portfolios has varied over time. Initially we saw GLIS used as a defensive, low volatility equity. This expanded to see it used as a source of income, as declining bond yields increased the relative appeal of its growing and relatively secure dividend streams. Most recently, we have seen listed infrastructure form part of the real assets segment of investors’ portfolios, due to the nature of its long-life, hard assets and ability to provide insulation from the effects of inflation. We have also seen investors utilise GLIS as a diversified, liquid and lower fee alternative to unlisted infrastructure allocations.

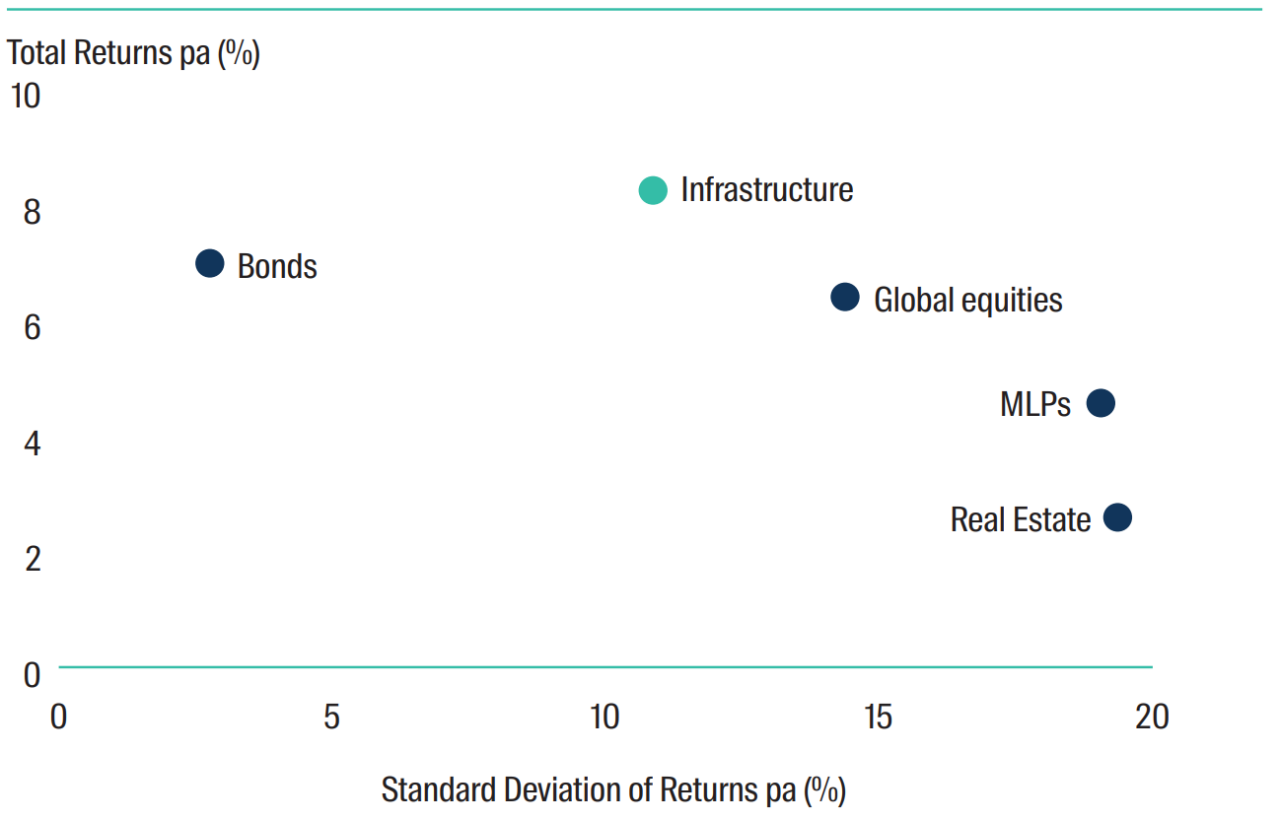

Since June 20071 , the GLIS asset class has generated returns of 8%2 p.a. with a standard deviation of return of 11% pa. This compares favourably to global equities (6% pa3), global property securities (3% pa4), Master Limited Partnerships (MLPs, 5% pa5) and global bonds (7% pa6).

Relative Risk/Return

FTSE Global Core Infrastructure 50/50 100% Hedged to AUD Net Tax.

FTSE EPRA/NAREIT Developed hedged in AUD Net TRI.

MSCI World hedged to AUD, Net TR.

Alerian MLP Total Return Index.

Bloomberg Barclays Global-Aggregate TR Index Value Hedged AUD.

Source: Bloomberg and First Sentier Investors. Monthly data from June 2007 to April 2018.

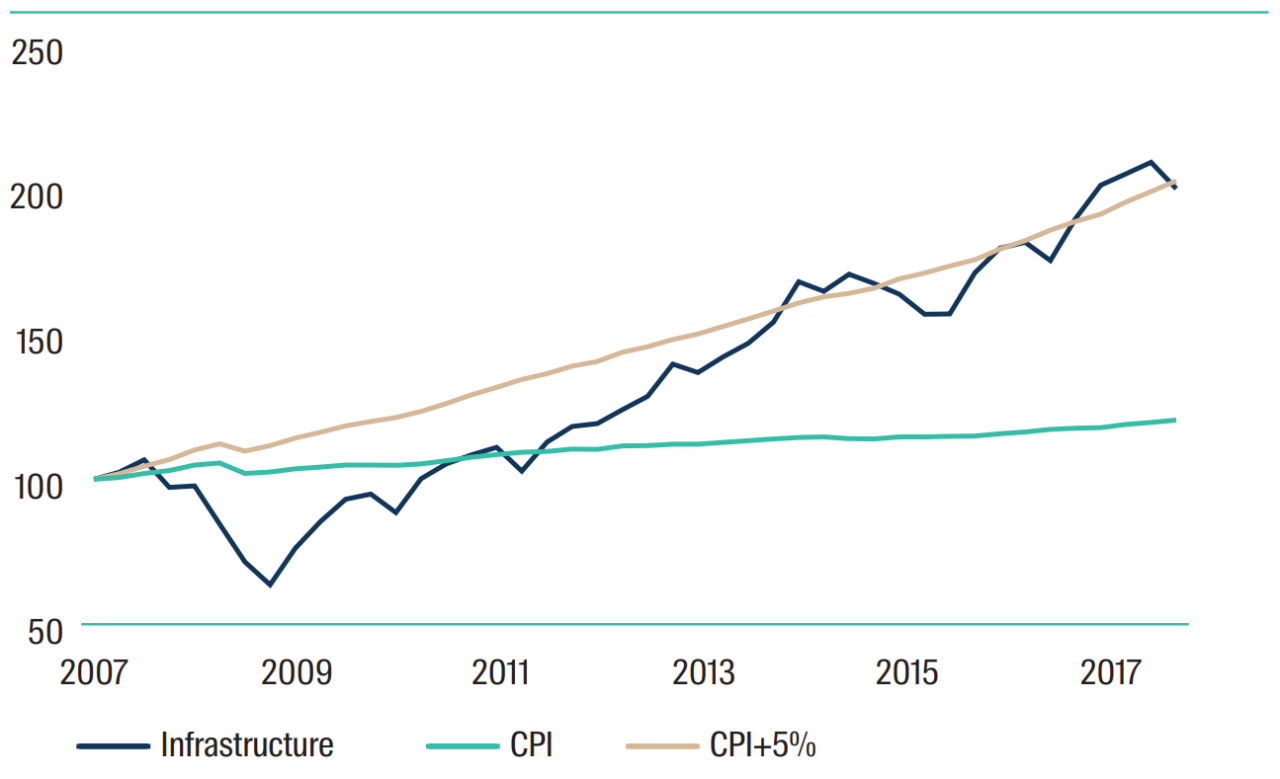

The chart above uses hedged or local currency data to show the performance of the underlying assets, regardless of currency impact. When currency is taken into account, listed infrastructure has returned 8% pa in AUD hedged terms; 6% pa7 in USD terms and 10% pa8 in GBP terms over this period. Relative to inflation, GLIS has provided investors with returns close to CPI plus 5% pa since June 2007.

GLIS performance compared with CPI

Infrastructure: FTSE Global Core Infrastructure 50/50 Total Return Index in USD.

CPI: US CPI Urban Consumers SA.

Source: Bloomberg and First Sentier Investors.

These strong risk-adjusted returns were delivered by a portfolio of listed companies that own essential service infrastructure assets that have high barriers entry, strong pricing power, structural or sustainable growth and highly predictable cash flows.

In addition to providing investors with an attractive beta, specialist fund managers in the GLIS asset class have consistently been able to deliver alpha through a wide range of market conditions. For example, the Colonial First State Wholesale Global Listed Infrastructure Fund has outperformed its index by over 1.4% pa since inception in 20079. Importantly this Fund has delivered very consistent outperformance by beating its benchmark index after fees in 8 of the 11 financial years since launch.

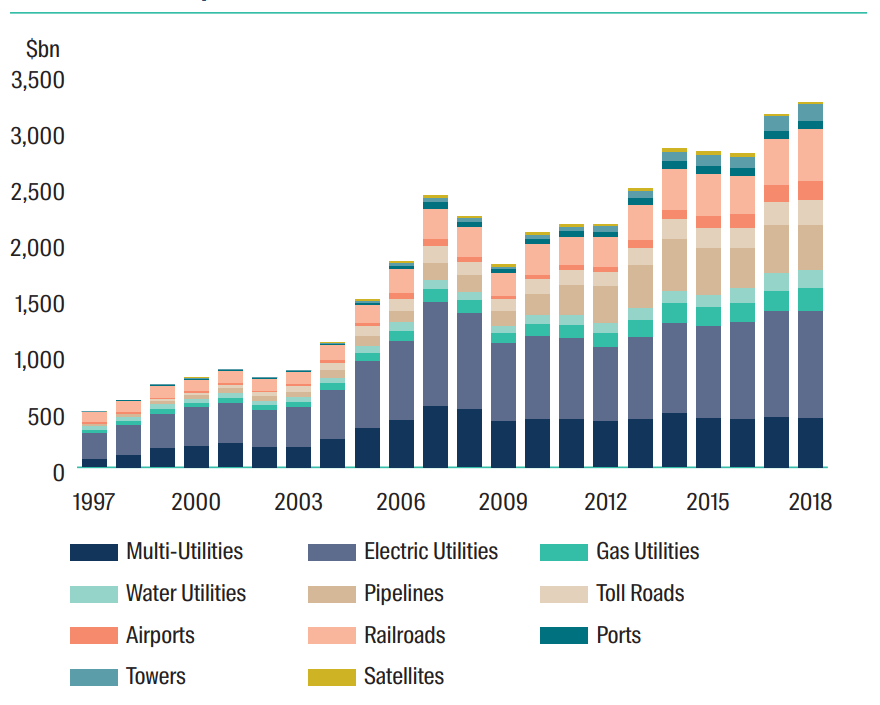

Growth in investible assets for GLIS

The amount of investable assets within the GLIS asset class has grown significantly in the past decade, in terms of both number and size of companies to invest in. This growth has come from three main areas: corporate restructurings; government privatisations; and new equity needed to grow existing infrastructure businesses.

Corporate Restructurings

Many infrastructure assets reside within large, vertically integrated corporations, conglomerates and private equity. In the lower growth world post the Global Financial Crisis (GFC), companies have increasingly looked to streamline and optimise their capital structures. This has often led to the divestment of their highly valuable infrastructure assets. Key examples of this include:

- Integrated oil and gas majors BP, Royal Dutch Shell, Total, Exxon Mobil, Canadian Natural Resources et al selling energy pipeline and distribution infrastructure assets to Enterprise Products Partners, Enbridge Inc., Pembina Pipeline, UGI Corp and Rubis.

- Telecommunication firms including AT&T, Verizon, Sprint, T-Mobile, Telefonica, Telecom Italia and Bharti Airtel selling mobile towers to American Tower, Crown Castle, SBA Communications, Cellnex, Inwit and Bharti Infratel.

- Shipping companies CMA CGM, Maersk, China Shipping and COSCO Shipping divesting container terminals to China Merchants Port Holdings and COSCO Shipping Ports.

- Construction companies including ACS, OHL and Odebrecht divesting various infrastructure assets including toll roads, ports and renewables to focused infrastructure firms including Vinci and DP World.

- Conglomerate restructurings resulting in the divestment of infrastructure assets into the listed market including Hutchison Ports, American Water Works, Westports and the Longhorn pipeline sale to Magellan Midstream Partners.

- Private equity selling infrastructure assets into the listed market. Examples include US private jet airport operator Landmark being sold to the listed company BBA Aviation; and the Initial Public Offerings (IPOs) of the world’s second largest satellite owner, Intelsat, and fourth largest US waste utility, Advanced Disposal Services.

Government Privatisations

The second major source of additional GLIS assets has been the privatisation of government owned infrastructure. Government debt has risen significantly post the GFC. This, combined with increased government spending on healthcare and social security, has led governments to dispose of high quality infrastructure assets to help maintain financial stability. Key examples of this around the world include:

- Europe: AENA (Spanish airport owner), Hamburger Hafen und Logistik (Germany’s largest port), Nice Airport, Bologna Airport, Rai Way (Italian communications towers), Enav (Italy’s airport control operator), Piraeus Port (Greece’s largest port), Greece’s airports (ex-Athens), PKP Cargo (Poland’s freight railway).

- Asia: DP World (Dubai’s global port operator), Kansai Airports; Kyushu Railway; Qingdao International Port; Qinhuangdao Ports, sale of Chinese provincial toll roads to listed companies.

- North America: Hydro One (Canadian electric utility), Ohio River Bridges East End Crossing Public Private Partnership (PPP) by Vinci, NTE and LBJ Express Lane PPPs in Dallas by Ferrovial, 95 and 495 Express Lane PPPs in Virginia by Transurban.

- South America: the sale of Brazilian airport and toll road concessions.

- Oceania: Aurizon (Australian freight rail firm), Queensland Motorways Ltd, TransGrid (Australian electric transmission company), Meridian Energy and Mercury NZ (New Zealand integrated utilities).

The above list includes 14 new global listed infrastructure companies, as well as increasing the asset base of existing listed infrastructure companies that acquired some of these assets.

Equity needed to grow existing infrastructure businesses

In order to grow existing infrastructure asset bases while maintaining balanced capital structures, listed infrastructure companies have issued large amounts of new equity over the past decade. This has resulted in significant growth in the size of the existing listed equity base of the GLIS asset class.

The main areas of asset growth that have been funded by expanded equity bases include renewable energy; oil & gas pipelines & storage; electricity transmission and distribution buildouts; upgrades of gas distribution networks; Liquefied Natural Gas (LNG) export terminals, new toll roads, airport terminal and runway expansions; upgrading freight railway track and rolling stock as well as the expansion and automation of container ports

GLIS market cap US$bn

Source: Bloomberg, First Sentier Investors.

Key GLIS trends over the last decade

Over the past decade GLIS has lived, thrived and survived in a variety of economic and financial market conditions. Following are some of the key trends we have observed in GLIS throughout this past decade.

Earnings resilience and growth

The business models of listed infrastructure companies have, on the whole, delivered resilient and growing earnings streams over the past decade despite the GFC and subsequent sluggish economic recovery. This earnings resilience is due to the essential service nature of the demand, structural volume growth drivers, high degrees of pricing power, strong barriers to entry and high operating margins.

Structural growth delivered

GLIS companies have delivered a high degree of structural, rather than cyclical, growth over the past decade. This structural growth has come from several areas, notably:

- Catch-up replacement capital expenditure in electric, gas & water utilities,

- The growing viability and expansion of renewable energy,

- Mobile tower & small cell infrastructure to support society’s increasing demand for mobile data,

- Airport passengers have grown at 2.6x global Gross Domestic Product (GDP) over the past decade10,

- The North American shale energy revolution, which has required new oil & gas pipeline, storage and export infrastructure, and

- The globalisation of LNG and Natural Gas Liquids (NGLs) has required significant infrastructure expenditure.

Of course not all structural growth stories played out the way we forecast. Global container trade volumes have disappointed with growth of only 1.7x11 GDP over the past decade (compared to 3.4x GDP for the 30 years prior to 2007).

Governments can interfere but rule of law (usually) prevails

Over the last decade we have witnessed various attempts by governments around the world to interfere with infrastructure assets. We are happy to report that the vast majority of these attempts have failed as political rhetoric has fallen short of economic and judicial reality.

Minimal business model disruption

The speed of business disruption has accelerated to a frightening pace over the past decade. Within the GLIS space however, business model disruption has been minimal. The two main areas in which disruption has occurred are:

- Renewable energy destroying the economics of unregulated power generation assets within integrated utilities and

- Over The Top (OTT) television delivered via the internet impacting the pay television video revenue streams of satellite infrastructure companies.

Takeovers add alpha to GLIS

High quality infrastructure assets are scarce. This, combined with the large sums of money that have been raised by private market infrastructure funds, has made GLIS the frequent target of takeovers.

Since inception, eleven of our Fund’s holdings have been taken over. Of these eleven, seven (Kelda Water, Intoll Group, Brisa, Forth Ports, Northumbrian Water, ConnectEast, Asciano) were acquired by private market infrastructure investors while the other four (Central Vermont Public Service, ITC Corp, Columbia Pipeline, Spectra Energy) were industry consolidation transactions. The premiums paid in these takeover transactions added alpha to our GLIS investors.

“Listed infrastructure companies have, on the whole, delivered resilient and growing earning streams over the past decade"

No substitute for on-the-ground research

We believe our greatest risk management tool over the last decade has been on-the-ground research. There is simply no substitute for robust and regular in-country due diligence of management, assets, regulators, customers, suppliers and government bodies.

Source: Bloomberg, First Sentier Investors.

What does the next decade hold?

As bottom up stock pickers, we always regard big picture crystal ball gazing with a large degree of apprehension. With that disclaimer, following are a few key issues that we believe will impact GLIS over the next decade.

Higher allocations to liquid real assets

We believe the fund flows into GLIS will continue over the next decade due to:

- increased demand for low volatility, income producing assets as baby boomers begin to draw down on their retirement savings and put a greater emphasis on capital protection

- increased penetration of the US pension and retail investor markets by the GLIS asset class

- increased demand for wealth products, including GLIS, from a growing middle class population in emerging markets and

- increased global demand for liquid real assets as a portfolio diversifier and inflation hedge.

Structural growth

We are as excited today about the structural growth drivers that underpin many GLIS assets as we were in 2007. That said, the structural growth drivers for the next decade will not be the same as for the previous one.

Key structural growth themes we believe will be relevant for the GLIS asset class over the next decade include the following:

- A continuation of the replacement cycle of aged infrastructure assets (especially roads, bridges, water, electric & gas utility assets) in many parts of the developed world with greater opportunities in North America relative to Europe and Japan

- Urbanisation and the growth of mega cities will require greater investment in passenger railways, toll roads and essential service utilities

- Economic development and the integration of emerging markets into the global economy will require further infrastructure investment

- China’s ‘One Belt, One Road’ development strategy has the potential to deliver significant infrastructure investments across Eurasia and Africa (albeit we are highly sceptical about some of the returns these projects will achieve)

- We expect airport passenger growth rates to remain at multiples of GDP growth rates, driven by the declining real cost of travel, the growth of the global middle class and an acceleration in baby boomer retirements

- We are still at the early stages of LNG & NGLs becoming a truly globalised industry. More investment in infrastructure will be needed to support this structural change

- We expect renewable energy and battery storage investment will continue to grow over the next decade, albeit at a slower rate due to the law of large numbers and a gradual reduction in subsidy levels, and

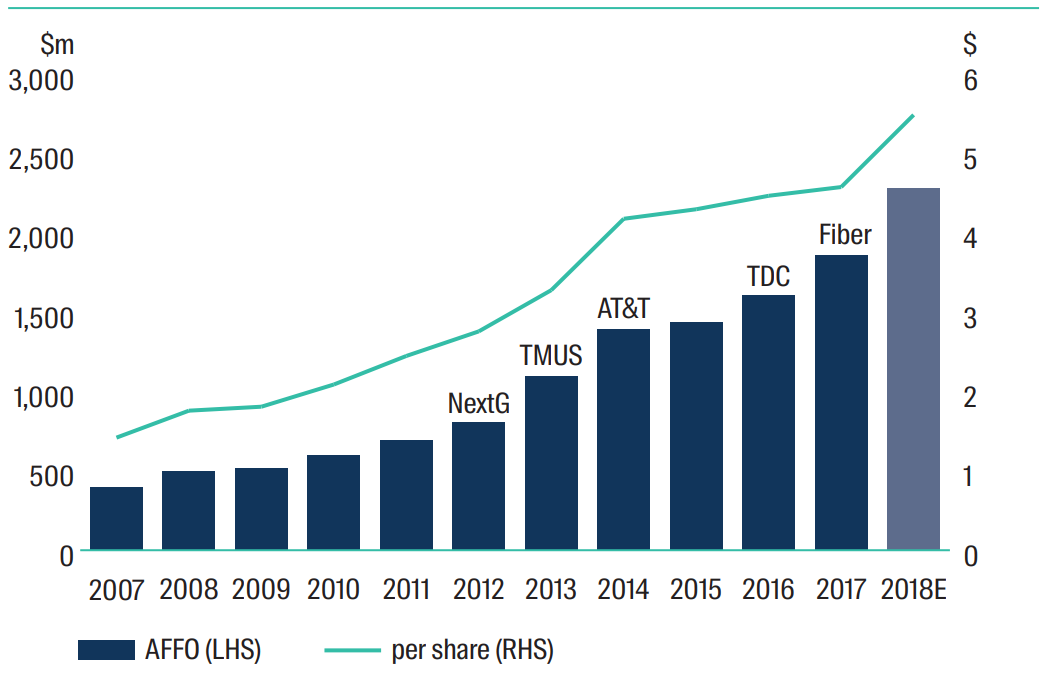

- Mobile communications should remain a strong structural growth area which will require mobile tower and small cell infrastructure to support the exponential increase in wireless network usage.

Crown Castle’s Adjusted Funds From Operations (AFFO)

Source: Company, First Sentier Investors.

De-globalisation and the return of economic nationalism

Brexit and Trump make it hard to ignore the potential impact of rising economic nationalism and de-globalisation, especially when it comes from the two countries – the United Kingdom (UK) and the United States of America (USA) – that have done the most to construct the global liberal order.

In the context of the GLIS asset class, this has the potential to increase political and legal risks if this populism continues or spreads. In the past year we have seen government intervention in electricity and gas markets in countries we usually consider as having low political risk like Australia, Canada, UK and USA.

De-globalisation has the potential to reverse well established trade flows, which in turn could reduce the value of infrastructure assets that support global trade including ports, freight railways and some toll roads.

Disruption

Just because business model disruption in infrastructure has been limited over the last decade, does not mean it won’t happen in the future. We remain alert, but not alarmed, about potential areas of disruption to infrastructure business models posed by issues including:

- The potential effect that distributed generation combined with battery storage may have on electric transmission & distribution grids.

- Renewable energy and battery storage are in a virtuous cycle of declining costs and growing market share which will further disrupt the old business models of coal and nuclear power producers as they suffer from increasing costs and lower volumes.

- OTT television via the internet will continue to be a major disruptive theme over the next decade for satellites (as well as leading to a generational change in television viewing habits by millennials).

- The rollout of 5G by wireless telecoms in the early 2020s has the potential to take market share away from mobile tower macro sites.

- 3D printing may alter global trade flows, which could in turn affect the infrastructure supporting this trade, such as ports and freight railways.

- A growing take-up in electric vehicles could adversely impact the oil price which would reduce the value of oil pipeline infrastructure assets.

- Autonomous cars could change society’s travel patterns with potential implications – both positive and negative – for toll roads and passenger railways. As experienced infrastructure specialists, it is our job to understand the impact of these potential future issues and to continue to protect and grow our clients’ wealth.

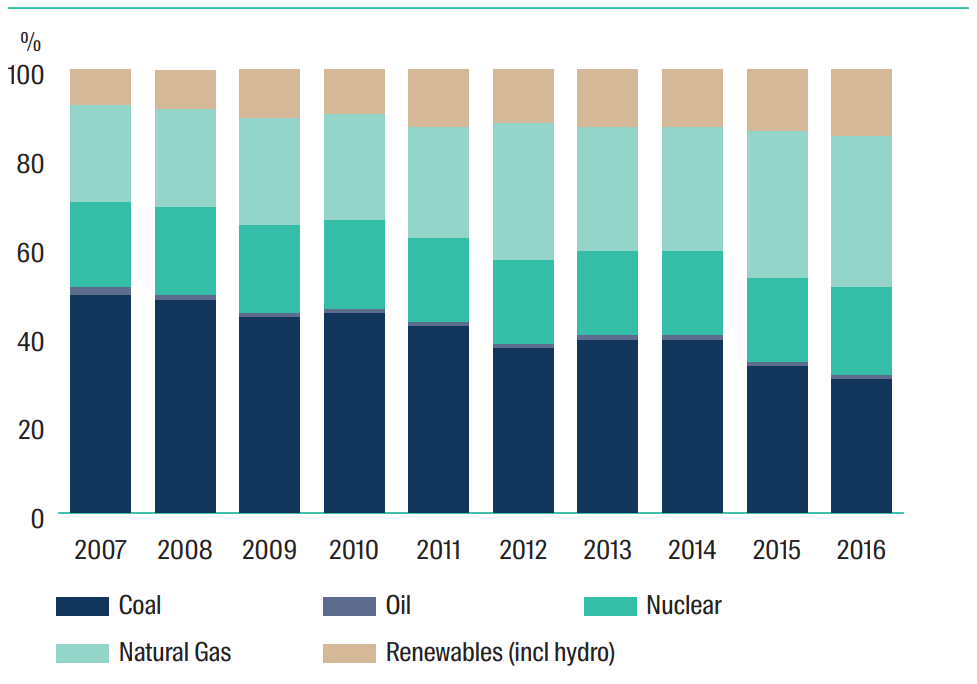

Growth of renewables US electricity generation by fuel type (%)

Source: Bloomberg, First Sentier Investors.

New supply of infrastructure assets to GLIS

Over the next decade we see the potential for many significant infrastructure assets to find their way into the GLIS investible opportunity set. In China, high government and State Owned Enterprise (SOE) debt levels could see equity raisings from utilities, passenger railways, toll roads as well as further port consolidation. A large amount of the Canadian utility sector remains in state government hands with the 2015 IPO of Ontario’s Hydro One offering a roadmap to the monetisation of these valuable infrastructure assets. The holy grail of new assets for GLIS remains the USA’s toll roads, airports and ports which are for the most part firmly entrenched in government ownership. However we are seeing some interesting signs in airports with St Louis Lambert International Airport up for privatisation and the announcement of a $10 billion PPP upgrade of New York’s John F. Kennedy International airport.

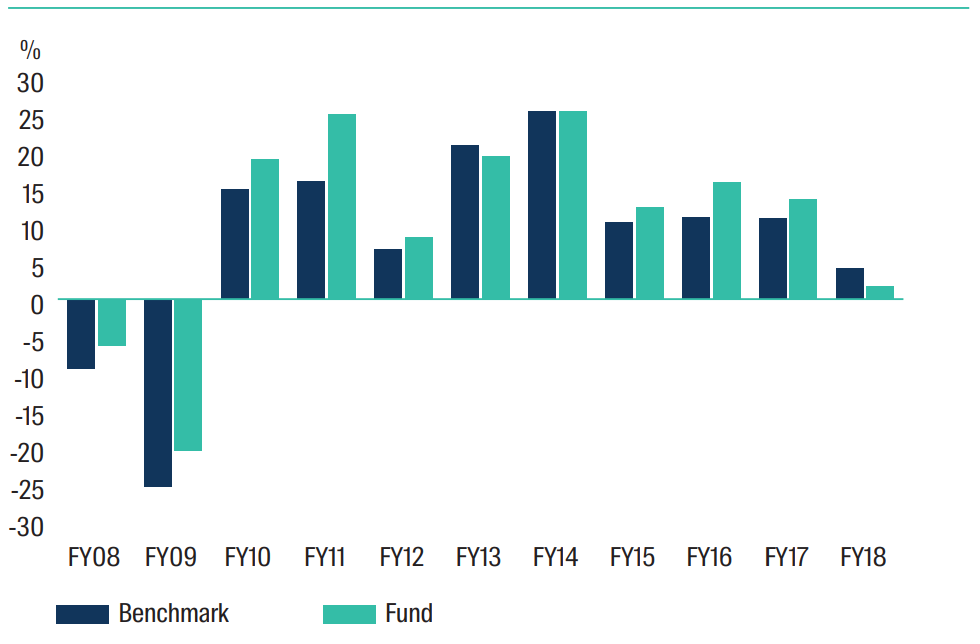

The need to be active

The past decade has seen our active bottom-up stock picking fund deliver over 1.4% pa outperformance, after fees over its benchmark. Over the next decade we believe active funds management will be more important than ever. Firstly, we believe increasing allocations to passive investment funds will create greater opportunities for experienced, specialist active fund managers like ourselves to create alpha. Secondly, as we are eight years into a bull market we believe alpha will become a larger component of investors’ total return over the next decade. Thirdly, we strongly believe that active management reduces risk by focusing on protecting our clients from potential permanent loss of capital (as opposed to index funds which buy more of a stock as its price increases and vice versa). These three factors mean that active management should provide our clients with higher total returns at lower levels of risk.

Fund performance vs benchmark, by financial year

Colonial First State Wholesale Global Listed Infrastructure Securities Fund, after fees and expenses. Benchmark is the FTSE Global Core Infrastructure 50/50 Net TR index (AUD hdg), previously UBS. Source: First Sentier Investors. Data as at 30 June 2018.

Conclusion

Within the relative short time of a decade, GLIS has become a widely recognised mainstream asset class. In our view this is due to the asset class delivering strong risk adjusted returns which have exceeded investors’ expectations. We believe our learnings from the past decade see us well placed to protect and grow our clients’ wealth in GLIS over the next decade.

1 To 30 June 2018

2 As measured by the FTSE Global Core Infrastructure 50/50 index, Net TR, AUD hedged.

3 As measured by the MSCI World hedged to AUD, Net TR

4 As measured by the FTSE EPRA/NAREIT Developed Index, Net TR, AUD hedged

5 As measured by the Alerian MLP TR Index

6 As measured by the Bloomberg Barclays Global-Aggregate TR Index Value AUD hedged

7 As measured by the FTSE Global Core Infrastructure 50/50 index, Net TR, USD

8 As measured by the FTSE Global Core Infrastructure 50/50 index, Net TR, GBP

9 To 30 April 2018

10 International Civil Aviation Organization

11 Alphaliner

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (Author). The Author forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for the Author is available from First Sentier Investors on its website.

This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are the opinions of the Author only and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product.

To the extent permitted by law, no liability is accepted by MUFG, the Author nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that the Author believes to be accurate and reliable, however neither the Author, MUFG, nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of the Author.