The listed infrastructure sector in North America contains many world leading assets, operated by world class companies - and it's growing - with over US$50 billion in assets being added to the asset class.

After three years of pain, the energy infrastructure sector has healed itself and is ready to expand again, this time using more sustainable corporate structures.

Green is good, with utilities investing successfully in renewable energy, battery storage, electric vehicle chargers and energy efficiency – with NO impact from recent electricity market interventions by the Trump administration.

Over US$50 billion in assets is being added to the global listed infrastructure asset class, via the build-out of infrastructure to export hydrocarbons from booming North American oil and gas fields.

Although populism and NIMBYism¹ are rearing their ugly heads in different parts of the continent, this is not affecting the thriving economy.

¹NIMBY is an acronym for “Not In My Back Yard”.

During my recent two week visit to North America (Toronto, New York, Boston, Kansas City, Topeka, Houston & San Diego) I met with many management teams across a variety of infrastructure sectors. The following article provides a brief update on what we are seeing from our boots-on-the-ground research across this dynamic and diverse continent.

American infrastructure exceptionalism

The North American listed infrastructure sector has many positive attributes, relative to the rest of the world. Firstly these companies operate in jurisdictions with relatively low political, legal and regulatory risk, and a high degree of transparency. Secondly they are part of a dynamic, high growth economy, characterised by creative disruption and underpinned by positive demographics, labour market flexibility, low taxes and small government. Thirdly, corporate governance practices and the skills and experience of company Board members, tend, in our view, to be superior to those found in many other parts of the world. Fourthly, North American firms are for-profit companies where shareholders are key stakeholders. Accordingly, management’s interests tend to be reasonably well aligned with those of the company’s shareholders. Finally, the domestic focus of most North American infrastructure firms, and their willingness to carry out share buybacks, greatly reduces the risk of capital reinvestment from overpaying for acquisitions, especially in foreign markets.

These attributes lead us to believe that North America has world leading infrastructure assets operated by world class companies, notably in the freight rail, energy pipeline, mobile tower, utility and waste industries.

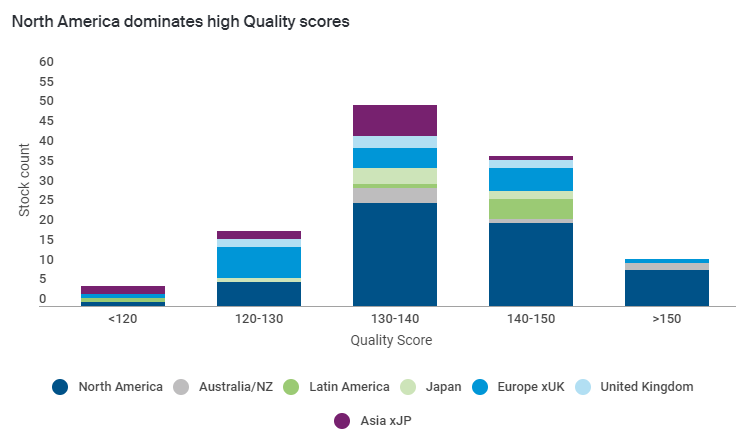

This American exceptionalism is evident in our investment process’ higher Quality scores for North American listed infrastructure companies. These scores are based on 25 qualitative criteria that we believe influence stock returns in general and infrastructure securities in particular. The average Quality score for North American listed infrastructure firms is 141, compared to an average Quality score of just 136 for non-North American firms. If we control for differences in infrastructure sub-sectors and consider utilities only, the difference remains material (143 for North American utilities verse 136 for non- North American utilities). Quality score criteria that North American companies rate highly on include Management; Financials and Regulation & Operational Risks.

Source: CFSGAM

Energy infrastructure healed

The United States (US) and Canada have global competitive advantages in energy production and infrastructure. These stem from ongoing improvements in drilling techniques, lower production costs, generally stable geopolitical environments and the ability to quickly harness large pools of human and financial capital. This is in stark contrast to poorly run government-owned competitors, which suffer rising production costs, limited investment and increasingly unstable political environments. The below chart highlights that the US is now the world’s largest liquids producer with Canada placed fifth.

* Liquids includes productions of crude oil (including lease condensates), natural gas plant liquids, biofuels, other liquids, and refinery processing gains.

Source: Plains All American Pipeline 2018.

The collapse of the oil price in 2014-15 left many energy infrastructure companies with lower-than-forecast earnings, over-extended balance sheets, distribution payments that exceeded cashflows, and counterparties with impaired credit worthiness. This was followed by a gruelling three-year process of distribution cuts, asset sales and equity raisings.

On this research trip, we saw clear signs that the energy infrastructure sector has now healed, following this painful but necessary course of action. The financial metrics of the sector have been brought back to a sensible, manageable range. Kinder Morgan has even started a US$2 billion share buyback. The underlying economics of their (and their customers’) businesses have vastly improved, owing to higher oil and Natural Gas Liquids (NGLs) prices over the past year. We are seeing strong pipeline demand from both supply push (energy producers) and demand pull (electricity generators, gas utilities, petrochemical complexes & NGL exporters) customers.

Massive production growth in regions such as the Permian Basin in West Texas has driven an urgent need for additional infrastructure investment (more pipelines and storage) to enable the crude oil and NGLs to reach end markets. Canada faces the problem of trapped oil and gas trading at large discounts to global prices, as the building of new energy infrastructure has proved slow and politically problematic. This lost revenue is estimated to cost Canadians C$20 billion in 2018.

Lack of infrastructure hurting Canadian prices

Source: Pembina Pipeline 2018

Our portfolio focuses on mispriced energy infrastructure firms which service low-cost production basins like TransCanada and Dominion Energy in the Marcellus for natural gas; and Plains All American Pipeline and Kinder Morgan in the Permian for oil and NGLs.

Green is good

Despite efforts by the US federal government to roll back environmental rules, and their attempts to support uneconomic coal and nuclear power plants, we observe NO change in the structural shift towards renewable energy across North America. Xcel Energy’s CEO was quoted in June as saying “It is not a matter of if we are going to retire our coal fleet in this nation, it’s just a matter of when”. While renewables subsidies are being phased out, wind and solar remain utilities’ preferred option for new-build power generation. To quote one CFO I spoke with “West Texas and Kansas are the Saudi Arabia of wind”. Battery storage, electric vehicle charging stations and energy efficiency programs remain very well supported in many states.

No holding back the wind

Source: American Wind Energy Association

Portfolio holdings benefiting from the greening of the grid include NextEra Energy, Alliant Energy, PG&E Corp and Portland General Electric.

New Jersey’s Clean Energy Future program

Source: Public Service Enterprise Group 2018.

Low electric and natural gas prices are keeping customer utility bills low. As a result, state regulators - and their political masters - remain highly supportive of electric and gas utilities spending capital to expand green energy initiatives, as well on repairing, replacing, upgrading, smartening and hardening their utility infrastructure.

Low customer bills enable capital expenditure

*For all years the billing assumes 7,200 kwh for electric and 1,010 therms for gas annually. E = Estimate.

Source: Public Service Enterprise Group 2018.

We view this sort of investment led earnings growth by electric and gas as very low risk given North America’s generally robust regulatory constructs. These strong capital expenditure levels are supporting earnings growth for portfolio utility holdings of 6-8% for Dominion Energy, 5-7% Alliant Energy, 6-8% Evergy Inc, 6-8% NextEra Energy and 7% plus for National Grid’s US operations.

Energy export infrastructure adds US$50 billion in assets to listed infrastructure

The North American energy export boom of Liquefied Natural Gas (LNG), Liquefied Petroleum Gas (LPG), refined products and crude oil has been accompanied by a large build-out of enabling infrastructure. The most recent project to go into service is Dominion Energy’s Cove Point LNG terminal, which began despatching commercial deliveries in April 2018.

Having agreed take-or-pay tolling agreements with highly quality, low risk counterparties and fixed price turnkey construction contracts, these US LNG megaprojects are delivering good risk-adjusted return outcomes².

Much of this infrastructure has been built by listed infrastructure companies, which has grown the overall asset base of the entire sector. We estimate that listed infrastructure firms are spending a combined US$50 billion on the following series of projects:

–$32 billion by Cheniere Energy on the Sabine Pass and Corpus Christi LNG terminals,

–$10 billion by Sempra Energy on the Cameron LNG terminal,

–$4 billion by Dominion Energy on the Cove Point LNG terminal,

–$1 billion by Kinder Morgan on the Elba Island LNG terminal and

– Several billion more for LPG, crude and refined oil export facilities from the likes of Enterprise Products Partners, Targa Resources, Energy Transfer Partners, Magellan Midstream, Plains All American Pipeline and AltaGas.

Portfolio holdings which are participating in energy export infrastructure build-out are Kinder Morgan, Dominion Energy and Plains All American Pipeline.

Politics – populism & NIMBYism

It seemed wherever I went on this trip that politics was impacting listed infrastructure companies. Crass conservative populism in Ontario, Kansas, Missouri and South Carolina has seen politicians targeting local utilities for short term political gain. On the topic of crass conservatives, I did enjoy laughing (and crying) while reading Fire and Fury - Inside the TRUMP White House. While in Kansas doing due diligence on the local utility, the political environment and wind farms, I dropped into the statehouse in Topeka and snapped the below photo at the governor’s (ceremonial) office.

² Unlike the LNG export projects in my native country, Australia, which suffer from large cost over-runs and the volatility of oil price-linked offtake agreements.

Playing Governor in Kansas

Source: CFSGAM

Populism is not the only political issue facing North American infrastructure. NIMBYism recently won out in British Columbia, where Kinder Morgan gave up on the controversial Trans Mountain oil pipeline. We believe Kinder Morgan’s decision to sell the project for C$4.5 billion was a good outcome for its shareholders. I doubt any of the listed infrastructure firms will buy this problematic project as the Canadian government tries to find a new owner. NIMBYism is also affecting the ability to expand other oil pipeline capacity out of Canada. Both TransCanada’s Keystone XL and Enbridge’s Line 3 Replacement projects are currently suffering delays, albeit we expect both will eventually get built.

It is not all doom and gloom on the political front. We applaud Missouri Governor Greitens, who on his last day in office, signed a utility bill into law which will greatly improve returns and earnings for local utility and portfolio holding Evergy Inc. Governor Brown in California is working hard with the legislature to fix the inverse condemnation liabilities facing that state’s utilities. We have also been impressed at how quickly New Jersey’s Governor Murphy has developed win-win, carbon friendly energy policies. While on the topic of politics, Foreign Affairs has an excellent article this month by Walter Russell Mead titled ‘The Big Shift – How American Democracy Fails Its Way to Success’.

Booming economy is a helpful tailwind

In the 11 years we have covered global listed infrastructure, we have neither seen the North American economy stronger than it is today, nor its infrastructure management teams more optimistic. While infrastructure demand is related primarily to the essential services it provides, GDP sensitive infrastructure sectors are enjoying a helpful tailwind.

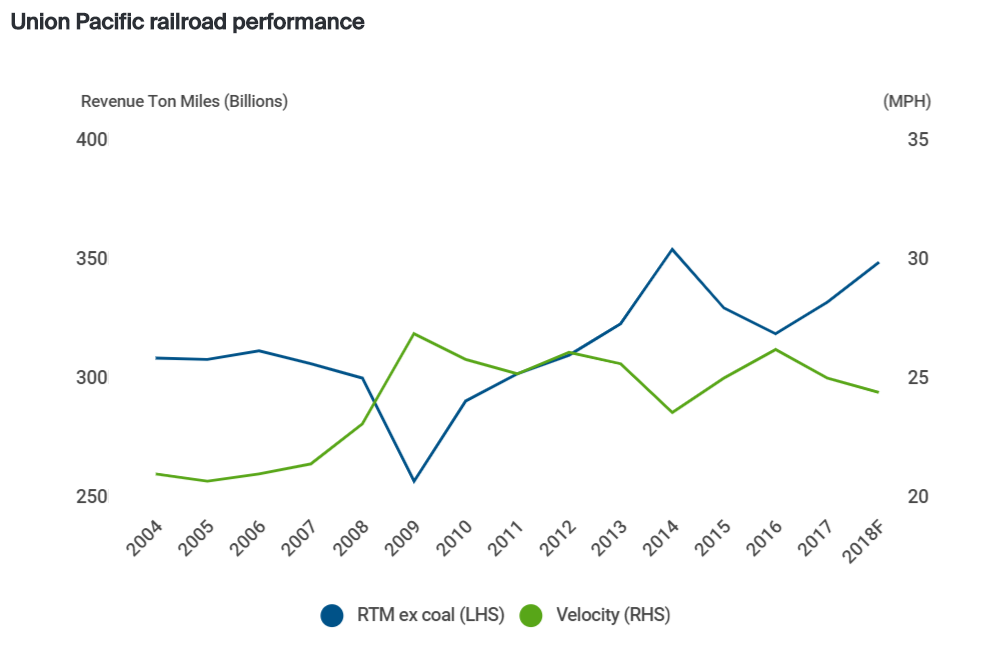

Freight railway volumes are very strong, growing at between 4% and 5% year over year (yoy); growth in waste volumes is well above trend (between 1% and 2% yoy); and industrial electricity load growth for utilities is robust. This, combined with oligopoly industry structures, is leading to above-trend pricing growth. However we note that freight railways have historically encountered operational obstacles when they have grown at this pace previously.

Union Pacific railroad performance

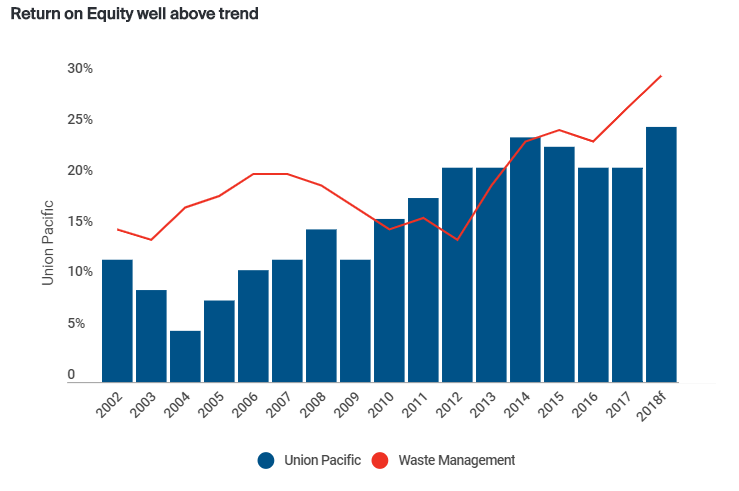

As you would expect, strong volume and pricing environments have seen Operating Margins and Return On Equity (ROE) reach unprecedented levels within the freight railway and waste sectors. The below chart illustrates the ROE improvement that industry leading firms Union Pacific and Waste Management are currently enjoying.

Return on Equity well above trend

Source: Company records, CFSGAM.

While we believe the North American freight rail and waste companies are world-leading businesses (and hence rate very highly on our Quality scores in the investment process), we believe earnings are above trend. Our base case scenario is that earnings momentum will slow from these elevated levels as we move into 2019.

Conclusion

The North American infrastructure sector has world leading assets, managed by world leading companies. The greening of the grid, healing of the energy infrastructure sector and a booming economy are all supportive of the sector’s investment fundamentals.

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (Author). The Author forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for the Author is available from First Sentier Investors on its website.

This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are the opinions of the Author only and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product.

To the extent permitted by law, no liability is accepted by MUFG, the Author nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that the Author believes to be accurate and reliable, however neither the Author, MUFG, nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of the Author.