As Australia’s leading liquidity manager, we often find our cash fund offerings compared against bank term deposits. In this piece, we seek to evaluate the relative merits of each of these cash investment strategies, comparing returns from our First Sentier Active Cash Fund with those of a typical term deposit investor over the past 6 years. This period is well suited for this type of analysis, as it includes a several instances of risk-market weakness, and overnight cash rates spanning 0.10% to 4.35% (it also happens to coincide with the launch of the fund!).

To begin, let us overview the broad characteristics of the two different cash strategies in question.

| Strategy | Term Deposit Strategy | First Sentier Active Cash Fund |

|---|---|---|

| Description | 12-month rolling term deposits with Australian Major Banks. Fixed interest rate at inception with steady return profile. | Investment in the First Sentier Active Cash Fund; a highly liquid investment vehicle with exposure to high-quality money market securities, bank deposit product, and floating-rate notes. |

| Liquidity | Somewhat illiquid - cash at maturity or with 31-days’ notice, with an interest penalty. | Daily liquidity t+1. |

| Return | Long-dated term deposits may outperform cash funds in falling interest rate environments, or in challenged credit environments. Bank regulation incentivises competitive pricing of retail deposits, however banks are also known to take advantage of investor inertia with teaser rate strategies. | May outperform term deposits in rising interest rate environments, or alongside favourable credit conditions, and is typically quicker to adjust to changing interest rate settings. Manager has flexibility to take advantage of different security types and funding conditions as they arise. |

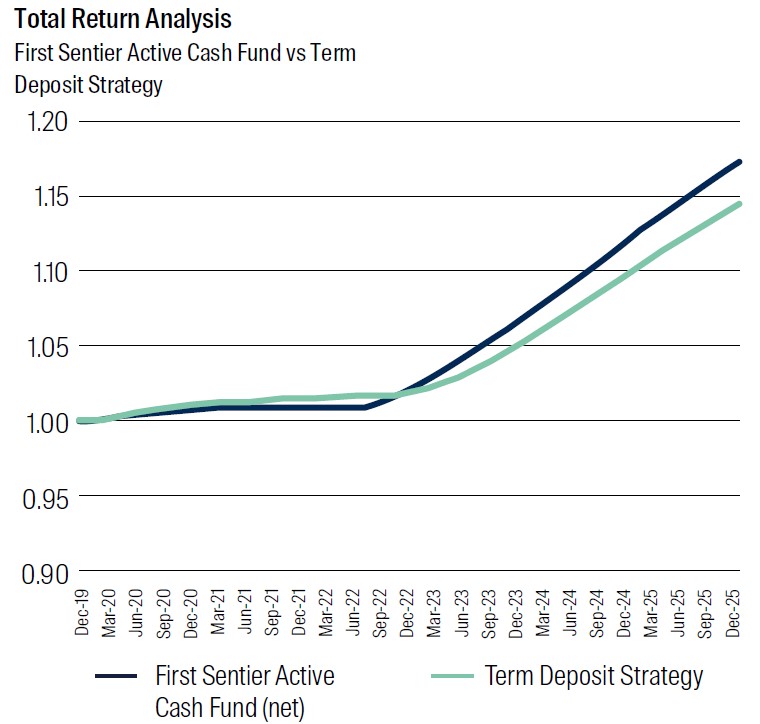

| Risk | No market-to-market volatility: term deposits are typically valued on a straight-line accrual basis, with the interest rate applicable for the life of the deposit known ahead of time. Small deposits benefit from the Financial Claims Scheme’s $250,000 deposit guarantee, with larger deposits above this amount subject to credit risk. | Very low mark-to-market volatility: cash funds, and indeed cash benchmarks, do exhibit a small level of volatility as tradeable money market instruments are revalued daily. A bank ‘negotiable certificate of deposit’ will revalue based on changes in interest rates, whereas a term deposit issued by the same institution will not ‘see’ this volatility. Investments in the First Sentier Active Cash Fund are typically very highly rated (A1+/AAA short-term/long-term average rating); however these investments are subject to credit risk. See Figure 2 for a total return comparison of both strategies. |

| Diversification | Typically concentrated with a small number of counterparty banks. | Higher level of diversification and security breadth compared to most term deposit strategies. Manager is empowered to alter the underlying investment mix through time to take advantage of different opportunities. |

| Administration | Can be onerous to ‘shop around’ and maintain an ongoing book of term deposits facing different counterparties. | Singular cash strategy available on all major investment platforms; SMA-friendly liquidity option. |

Having reviewed the broad characteristics of each approach, let us construct a term deposit return series to complete our analysis. Taking data from the RBA’s Advertised Deposit Rates tables1 – we model a typical term deposit investor, rolling a series of 12-month term deposits on a staggered basis at 6-month intervals. With this schedule, we construct a total return series and compare this to the net return outcomes seen in our flagship First Sentier Active Cash Fund. These returns outcomes are illustrated in Figures 1 and 2.

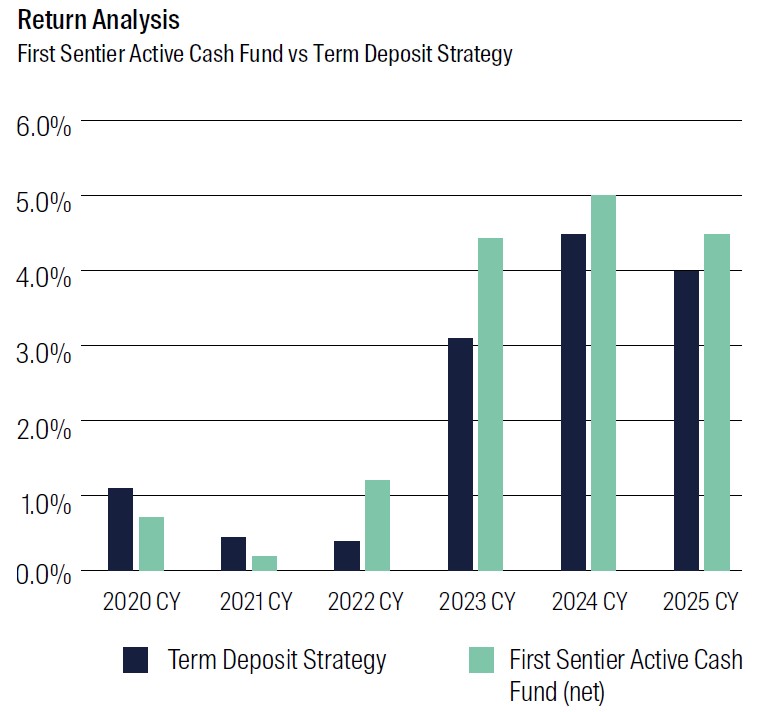

Figure 1 - Return Analysis

Figure 2 - Total Return Analysis

We can draw a number of observations from this analysis:

The Term Deposit Strategy and the First Sentier Active Cash Fund offered similar return outcomes over the analysis window, with the First Sentier Active Cash Fund offering slightly better outcomes overall.

a. Term deposits performed well in the early stages of the pandemic and during the zero-interest rate period of 2020-2022, as emergency liquidity support provided unlimited funding to the local banking sector, to the detriment of traditional institutional investors. The 12-month term deposit locked in at the beginning of the period (31/12/2019) also provided a return buffer as interest rates fell, demonstrating one of the advantages of this strategy in falling rate environments.

b. The First Sentier Active Cash Fund performed better as interest rates normalised, as it adjusted more quickly to changing levels, and subsequently benefited from normalised credit and funding markets. The First Sentier Short Term Investments team were also able to take advantage of their scale and relationships to secure better yielding investments in this period, as banks sought to re-establish funding with the institutional market away from the emergency liquidity conditions they had become used to.

- Whilst the First Sentier Active Cash Fund does exhibit low levels of volatility compared to the relative certainty of the Term Deposit Strategy, its returns remained remarkably stable throughout historically volatile periods such as the COVID pandemic, or the normalisation of interest rates and credit spreads in 2022.

- It is of course important to note the biggest difference between the two strategies – liquidity. The First Sentier Short Term Investments team regularly facilitate billions of dollars of daily transactional liquidity as the largest cash manager in Australia, including throughout extreme periods such as the early days of the COVID pandemic. Our focus on deep relationships with the strongest, most liquid counterparties protects what is arguably the most important characteristic of cash investing – liquidity. Whilst term deposits do offer limited liquidity at specified windows, they do not offer the flexibility that daily liquidity provides.

- To requote our opening line - cash investment focusses on three objectives: capital stability, liquidity, and income. Within these objectives, term deposits and cash funds both have a role to play, with different characteristics and advantages. Hopefully this analysis helps illustrates the difference between the two approaches, and helps the reader determine the best approach for their own circumstances.

1 Source: ‘Advertised Deposit Rates – F4’, https://www.rba.gov.au/statistics/tables/. “Figures for ‘banks’ term deposits’, where available, are averages of the five largest banks’ rates.”

Short Term Investments and Cash

We are Australia's largest cash manager

We manage a range of strategies, all of which provide a high level of liquidity and capital preservation. Our experience has seen us successfully navigate various market cycles with consistent delivery of strong performance since 1988.

Read our latest insights

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (FSI AIM), which forms part of First Sentier Group, a global asset management business. First Sentier Group is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. References to “we” or “us” are references to First Sentier Group. Some of our investment teams use the trading names First Sentier Investors, FSSA Investment Managers, Stewart Investors, Albacore Capital, Igneo Infrastructure Partners and RQI Investors. A copy of the Financial Services Guide for FSI AIM is available from First Sentier Investors on its Australian website.

This material is directed at persons who are wholesale investors or clients and is not intended for persons who are retail investors or clients. Any advice in this material is general advice only. It does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. The information in the material does not constitute an offer of, or an invitation to purchase or subscribe for any securities.

The product disclosure statement (PDS) or Information Memorandum (IM) (as applicable) for the First Sentier Active Cash Fund, ARSN 634 630 229 (Fund), issued by The Trust Company (RE Services) Limited (ABN 45 003 278 831, AFSL 235150) (Perpetual), should be considered before deciding whether to acquire or hold units in the Fund(s). The PDS or IM are available from First Sentier Investors. The target market determination (TMD) for the Fund is available from First Sentier Investors on its website and should be considered by prospective investors before any investment decision to ensure that investors form part of the target market.

MUFG, FSI AIM, their respective affiliates and any service provider to the Fund do not guarantee the performance of the Fund or the repayment of capital by the Fund. Investments in the Fund are not deposits or other liabilities of MUFG, FSI AIM, their respective affiliates or any service providers to the Fund and investmenttype products are subject to investment risk including loss of income and capital invested.

Any opinions expressed in this material are the opinions of the individual author at the time of publication only and are subject to change without notice. Such opinions: (i) are not a recommendation to hold, purchase or sell a particular financial product; (ii) may not include all of the information needed to make an investment decision in relation to such a financial product; and (iii) may substantially differ from other individual authors within First Sentier Group.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of a First Sentier Group portfolio at a certain point in time, and the holdings may change over time.

We have taken reasonable care to ensure that this material is accurate, current, complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material and we do not undertake to update it in future if circumstances change. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of FSI AIM.

Any performance information has been calculated gross or net of management fees (where indicated) and net of transaction costs (other than brokerage costs incurred when trading on the ASX). No allowance has been made for taxation. Past performance is not indicative of future performance.

Copyright © First Sentier Group, 2026

All rights reserved