Insulation from the effects of inflation is a key objective for many investors and global listed infrastructure has delivered returns in excess of inflation over the long term. But passively investing in this asset class does not guarantee a hedge to inflation.

Insulation from the effects of inflation is a key objective for many investors. Many pension and sovereign wealth funds specifically target long-term returns of CPI (Consumer Price Index) plus 5%.

Global listed infrastructure has delivered returns in excess of inflation over the long-term. Most infrastructure assets have an explicit link to inflation through regulation, concession agreements or contracts. Other assets without an explicit link often have the pricing power to deliver a similar (or better) outcome reflecting their strong strategic position.

This relationship between inflation and pricing is explored throughout this paper in a range of examples. It highlights that more than 70% of assets owned by listed infrastructure companies have effective means to passthrough the impacts of inflation to customers, to the benefit of shareholders.

Passively investing in the asset class does not guarantee a hedge to inflation and significant qualitative assessment is still required. Key issues to consider are the transparency of regulation and the risk of political interference. Infrastructure companies should maximise the link to inflation by (1) renegotiating contracts to pass-through variable costs to customers and (2) maintaining an appropriate debt structure so price increases fall to the bottom line.

And while listed infrastructure can provide a practical hedge to inflation, investors need to allow an investment time frame of three years or more.

Macroeconomic context

The outlook for inflation is one of the most important factors for financial markets, currencies and economic growth. Higher inflation erodes the purchasing power of wealth, and the value of investments. Today’s synchronised global economic growth rates, tightening labour markets and US corporate tax cuts are all conducive to rising inflation.

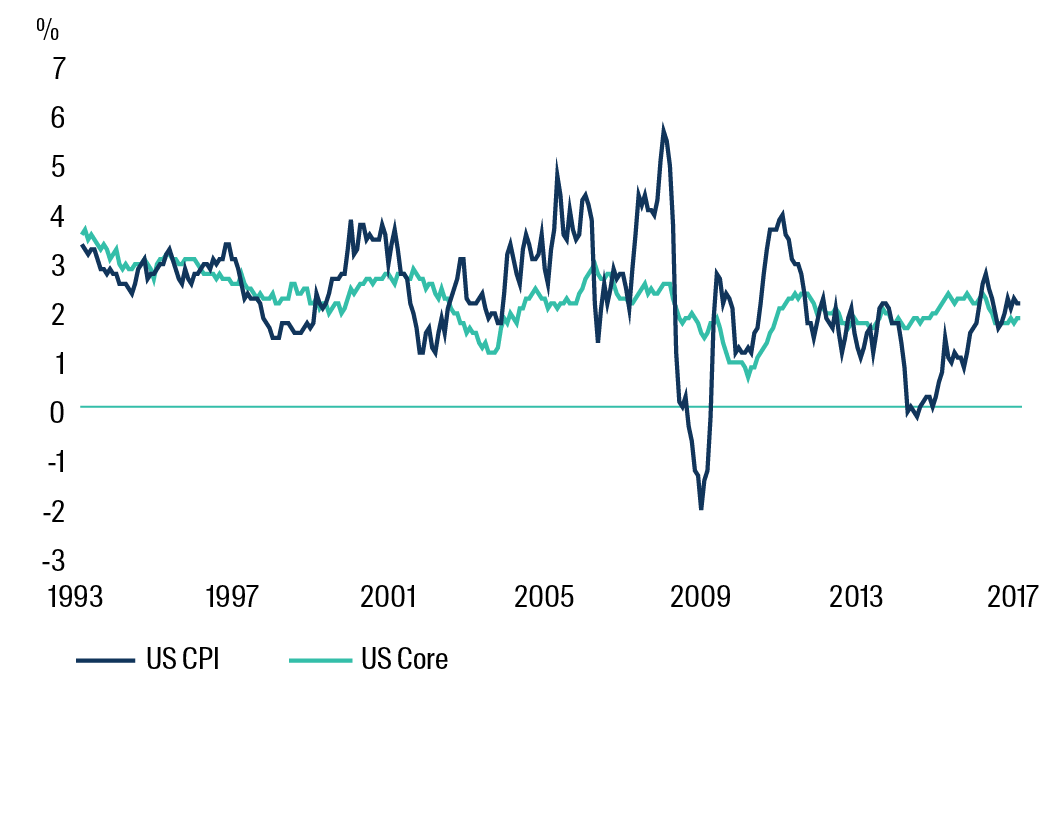

Low headline inflation rates around the world in recent years have partly been a reflection of weaker commodity prices. This is most evident when looking at US inflation and comparing the headline inflation rate with the core rate (i.e. ex food and energy). Commodity prices have started to rise again, potentially removing a brake from the inflation rate.

Infrastructure also plays a structural role in price stability. Well planned infrastructure can ease price pressures as it improves productivity. Infrastructure development in China, for instance, has played an important role in limiting inflation, despite periods of very strong growth in demand and economic activity.

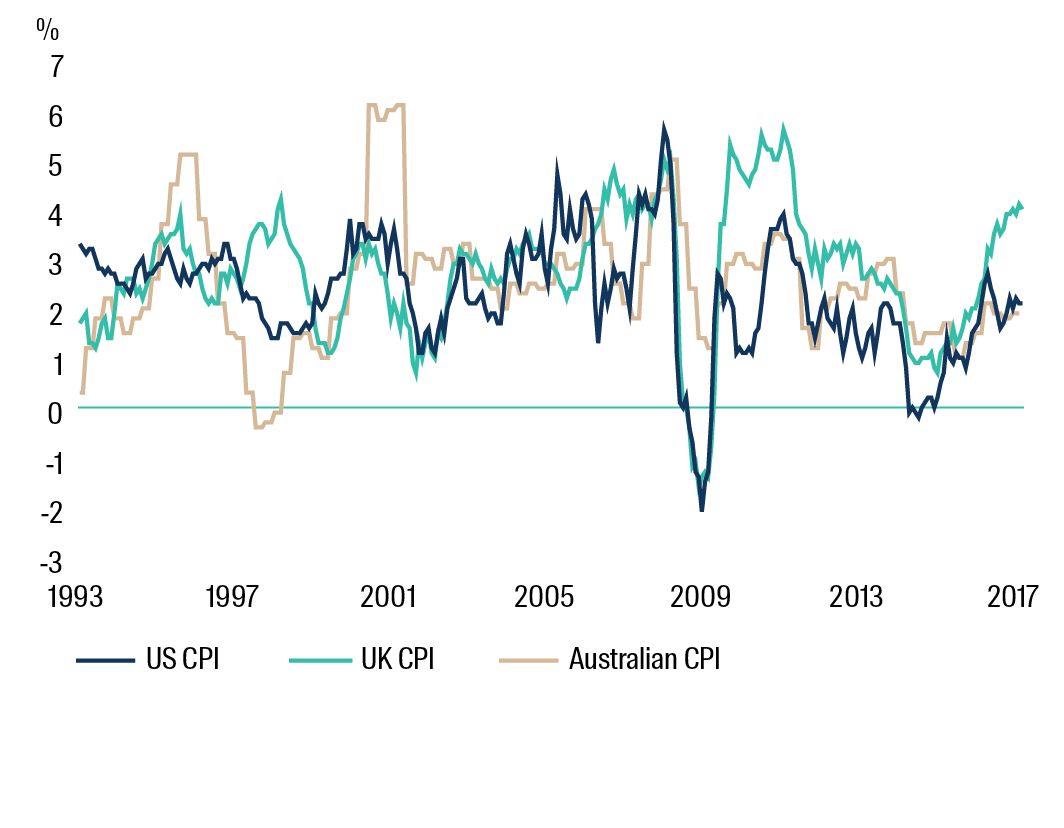

Headline inflation rates

US CPI Urban Consumers YoY NSA, UK RPI YoY NSA Australia CPI All Groups Component YoY. Source: Bloomberg, First Sentier Investors. As at 31 December 2017.

US inflation rates

US CPI Urban Consumers YoY NSA

US CPI Urban Consumers less food and energy YoY NSA

Source: Bloomberg, First Sentier Investors.

As at 31 December 2017.

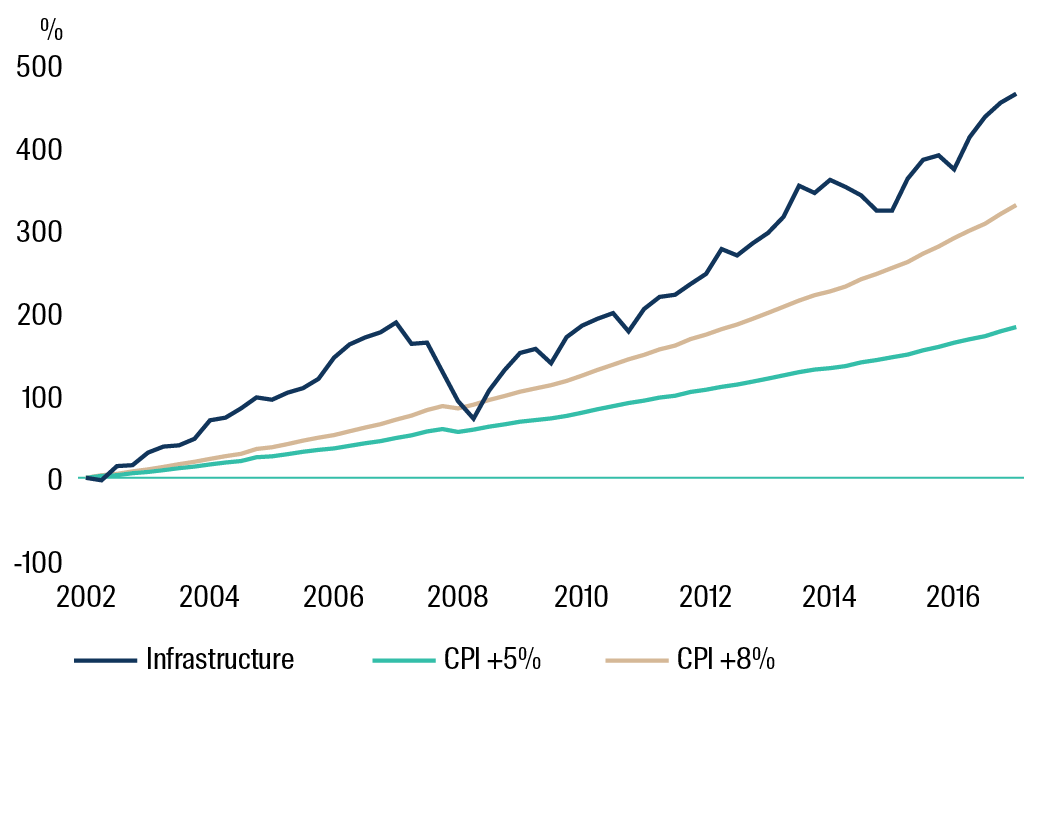

Performance of global listed infrastructure relative to inflation

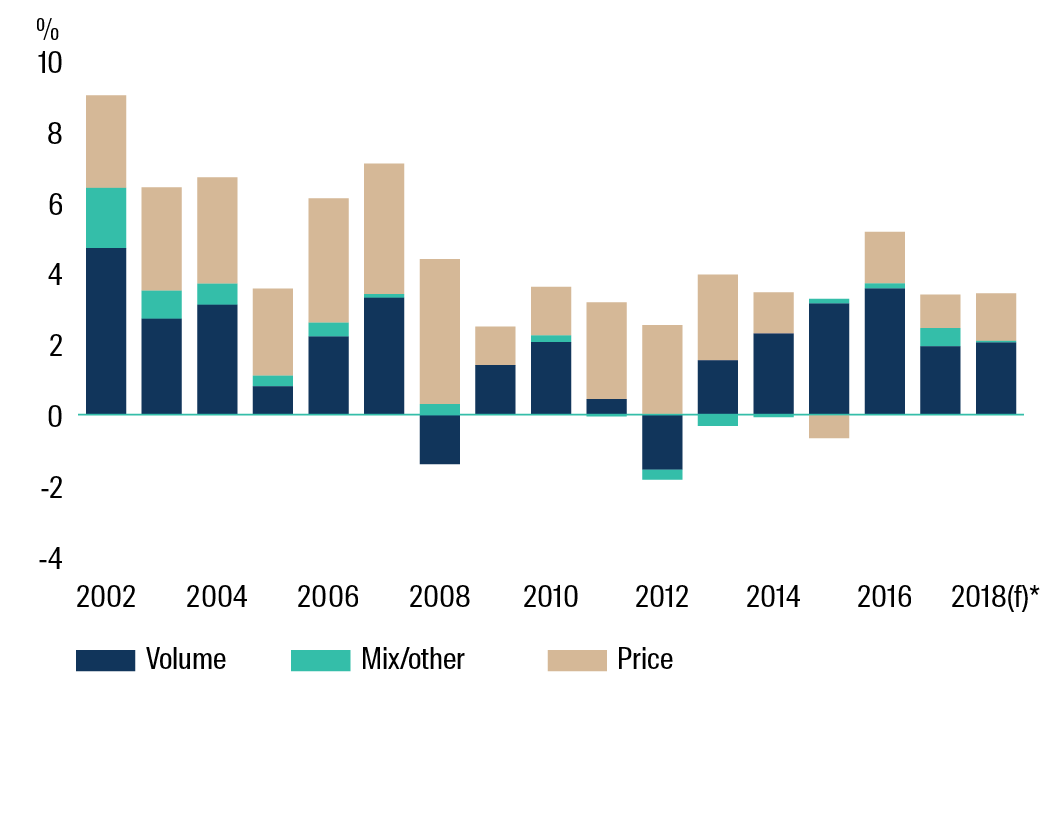

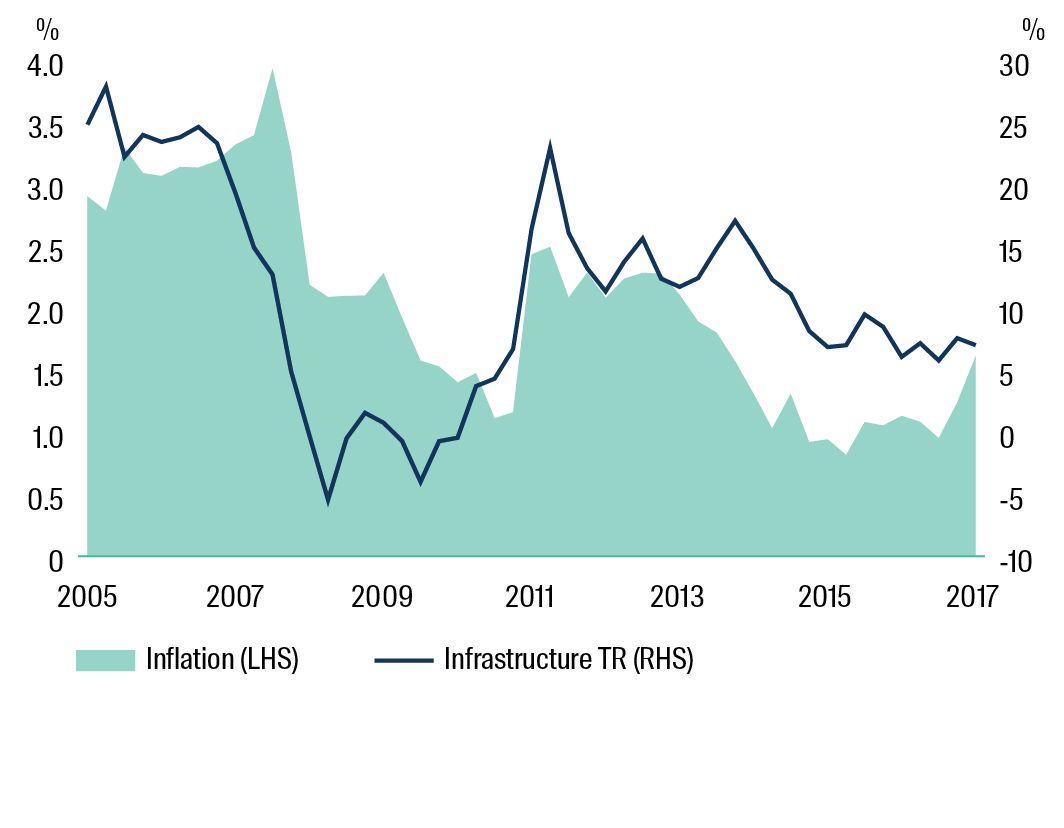

Global listed infrastructure has historically proved capable of delivering returns well in excess of inflation. For the 15 years to December 2017, listed infrastructure has delivered total returns of 12.2% pa, equivalent to CPI plus 10.1%.

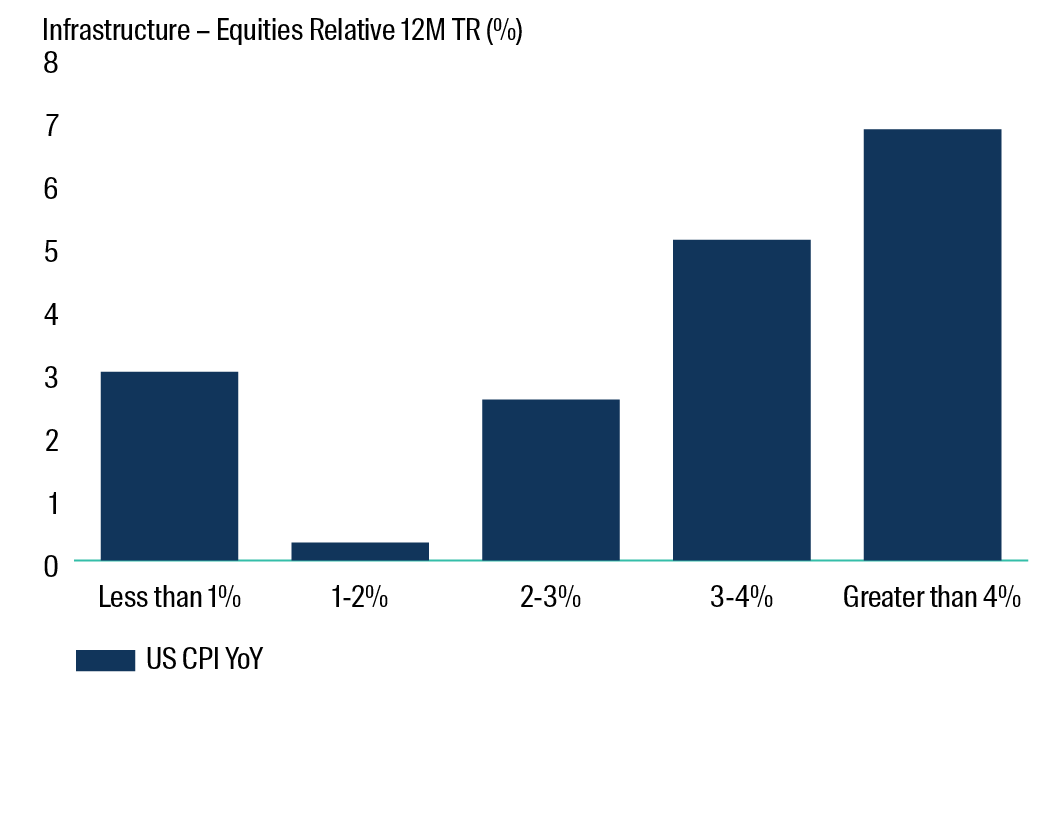

Over the same period, the performance of global listed infrastructure during periods of higher inflation provides further evidence of the benefits of this asset class. The chart below compares the relative performance of infrastructure to global

equities, when inflation is in a given band.

For example, when inflation is between 3% and 4% pa, global listed infrastructure has outperformed global equities by around 5% pa on average. Importantly, this outperformance increases to almost 7% pa when inflation is above 4% pa.

Listed infrastructure performance

Infrastructure: FTSE Global Core Infra 50/50 Net TR Index (USD) from Dec-05, prev Macquarie. CPI: US CPI Urban Consumers SA. Source: Bloomberg and First Sentier Investors. Quarterly time series from 2002-2017

Infrastructure performance during periods of inflation

Infrastructure: FTSE Global Core Infra 50/50 Net TR Index (USD) from Dec-05, prev Macquarie Equities: MSCI Daily TR Gross World (USD) CPI: US CPI Urban Consumers SA Source: Bloomberg and First Sentier Investors. Quarterly time series from 2002-2017

Inflation protection in infrastructure assets

Infrastructure generally offers inflation protection to investors, with the degree of protection varying by asset. Most infrastructure assets have an explicit link to inflation through regulation, concession agreements or contracts. Other assets without an explicit link often have the pricing power to deliver a similar (or better) outcome. This reflects their strong strategic position which limits competition. The relationship between inflation and pricing is explored through a range of examples below. The analysis highlights that more than 70% of assets owned by listed infrastructure companies have effective means to pass-through the impacts of inflation to customers, to the benefit of shareholders.

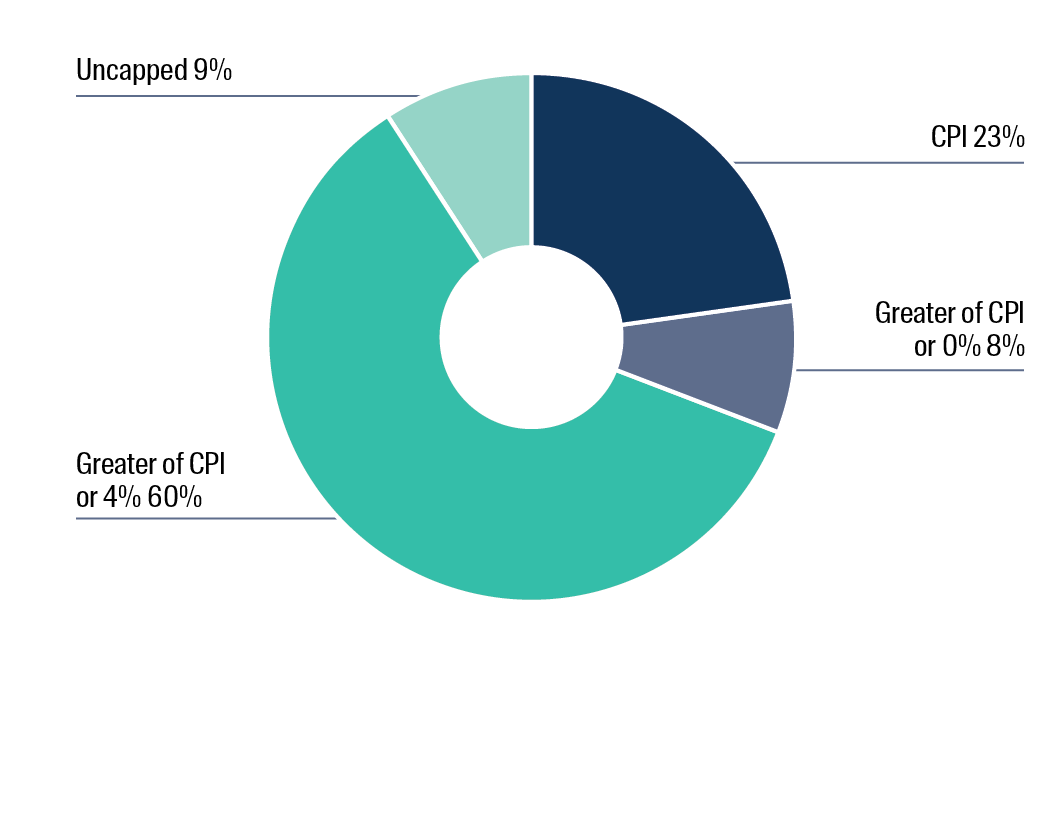

Toll road pricing is often explicitly linked to inflation. French motorways have concession agreements providing for annual toll increases at a minimum of CPI x 70%. In addition they have been able to negotiate higher outcomes for pricing as compensation for growth capital expenditure (capex), like a new section of road. Vinci subsidiary ASF, a network of more than 2,700km of motorways in south-west France, provides a good example of this. Inflation-linked toll increases have consistently boosted revenue growth over the long term. The terms of Australian toll road company Transurban’s concessions allow it to increase prices on many of its roads by the greater of inflation or 4% pa.

Similar concession agreements where tolls are explicitly linked to inflation exist in Brazil, Canada, Chile, Italy, Portugal, Spain, UK and the US.

Vinci’s ASF revenue growth

Please note that forecasts cannot be guaranteed.

Source: Autoroutes du Sud da la France, First Sentier Investors. As at 31 December 2017.

Transurban pricing agreements

Source: Transurban, First Sentier Investors. As at 31 December 2017.

Water, electricity and gas utilities often have an explicit link to inflation through regulated pricing. UK water utilities earn a real return on regulated assets, with prices increasing by Retail Price Index (RPI). Electricity transmission companies like National Grid in the UK, Red Electrica in Spain, Terna in Italy or AusNet Services in Australia have variations in the way regulated returns are calculated, but all can claim to recover inflation over time. US electric and gas utilities operate within regulatory frameworks which enable them to earn an allowed rate of return on money spent maintaining or improving their asset base. While this rate is fixed for each regulatory cycle (which usually lasts between one and three years), the allowed rate of return of the next cycle can be adjusted upwards if needed, to reflect a higher inflation environment.

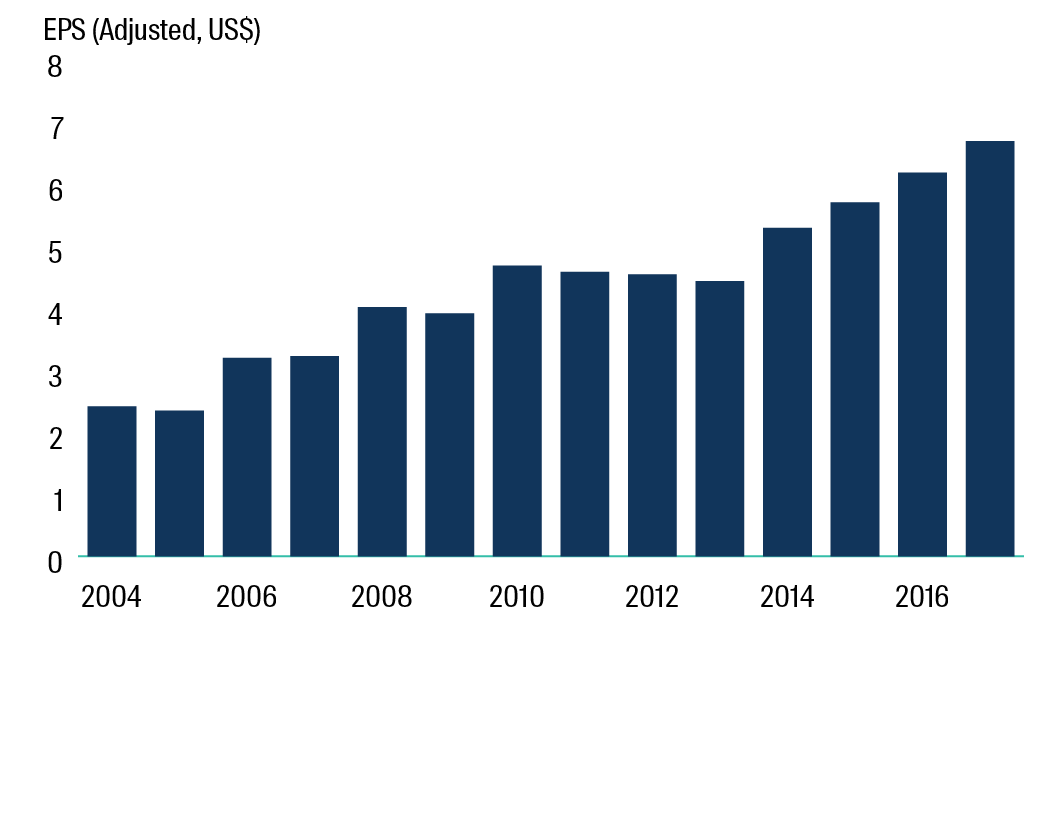

US electric utility NextEra Energy has grown its earnings by investing in the rate base of its regulated Florida utility business, and through the build-out of contracted wind and solar assets across the US. This approach has enabled it to grow its Earnings per Share (EPS) at a compound annual growth rate of 8% pa over the past 15 years.

NextEra Energy EPS growth

Source: Bloomberg, First Sentier Investors. As at 31 December 2017.

Integrated utilities combining transmission and distribution networks with energy retailing, power generation and even gas production would not be expected to have a high degree of inflation protection. It could be argued that rising commodity prices feed through to inflation as well as the value of power generation assets, but this link is less tangible than a regulated outcome and the benefit may be offset by the squeeze on retail margins.

Energy pipeline contracts vary in the way prices are set. Generally, oil pipeline contracts in North America are either linked to PPI (Producer Price Index) or allow annual tariff resets to recover changes in costs. Most gas pipeline contracts are fixed but others have no regulation at all. High operating margins and light-handed regulation on pipelines provide comfort that rising inflation would not pose challenges to these companies.

Bulk liquid storage companies typically charge capacity fees linked to local inflation rates. Contracts for storage products like bunker fuel, gasoline, industrial chemicals, biofuels or LNG (Liquefied Natural Gas) are negotiated with customers and extend for 1 to 15 years. Strong demand for refined product and the shortage of available land to unload/store hazardous liquids has given pricing power to industry leaders.

Port operators are generally not regulated and negotiate prices directly with shippers. Overcapacity in some regions (Northern Range and Pearl River Delta) has seen a number of ports reduce prices to attract volumes. Consolidation in the shipping industry has also tilted the balance of power. However over the long-term port companies have delivered reasonable pricing power to investors.

Mobile towers have contracted annual price escalators in the order of around 3% pa. Telecom service providers lease tower capacity to deploy antennae and radios for their wireless networks. They typically lease for an initial term of between five and fifteen years, with multiple five-year renewal options. Strict zoning requirements and community opposition impede competition and create high barriers to entry in the tower industry.

This helps the tower industry realise very high contract renewal rates and attract new business on existing sites. Airport pricing varies by country but the sector has shown a reasonable degree of inflation protection over time. UK airports

are fully regulated and receive a real return on assets with prices linked to RPI. Australian airports do not have an explicit link to inflation but enjoy a light-handed regulatory environment. Aeronautical price increases are negotiated directly with airlines to recover growth capex while retail, property, car parking and other commercial activities are not price regulated.

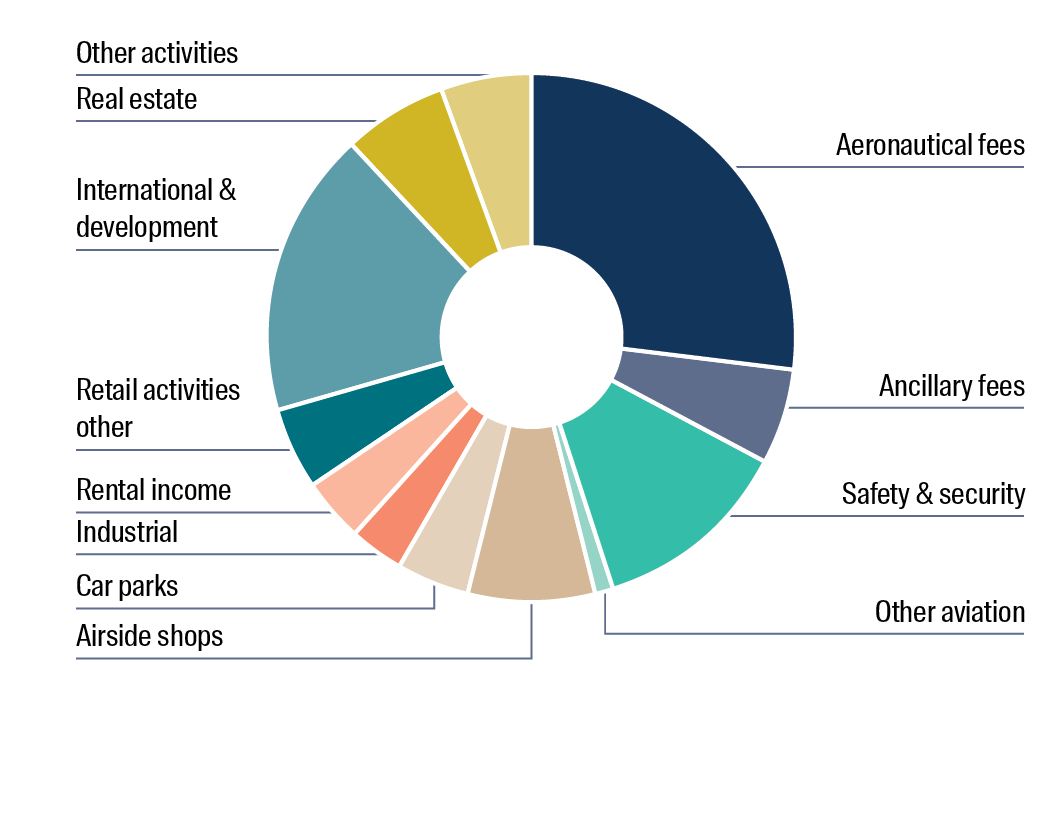

European airports have a range of regulatory structures which are tending to provide greater flexibility to recover inflation over time. For example, Aeroports de Paris (ADP) is allowed to increase Aeronautical fees by CPI +1% pa, while its real estate rents are linked to the France Cost of Construction Index.

Aeroports de Paris Revenue mix

Source: First Sentier Investors, ADP. As at 31 December 2017.

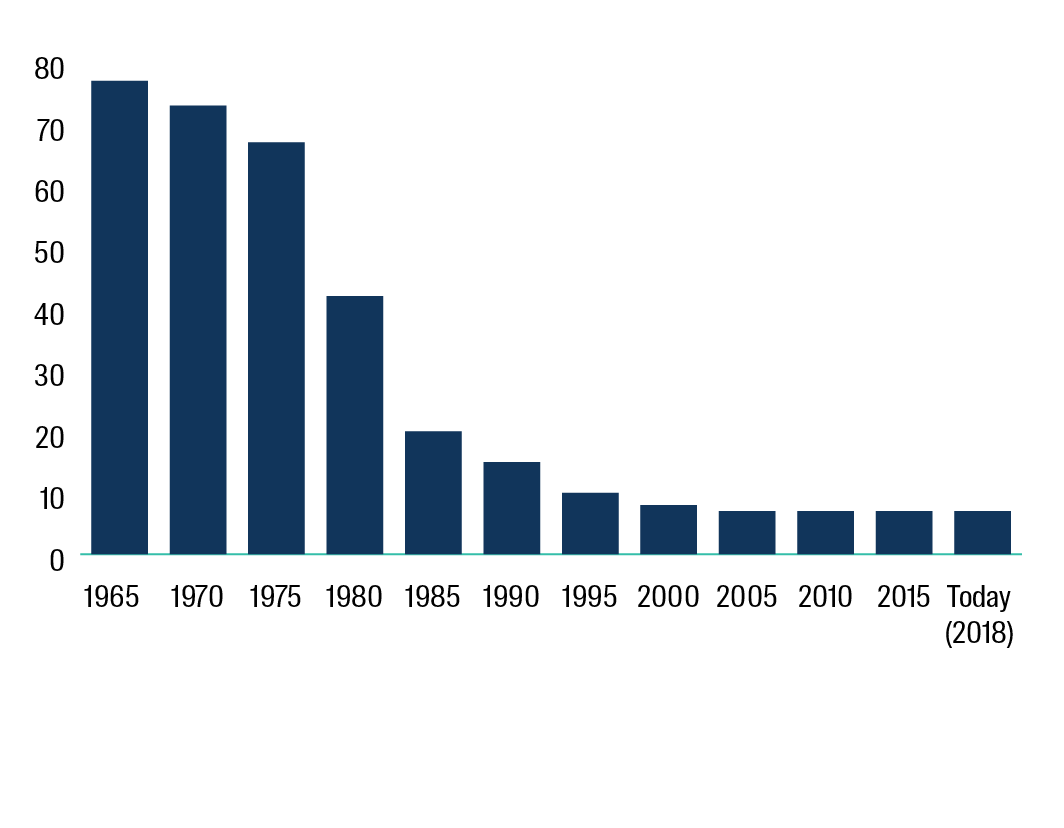

Rail companies have improved their pricing power in recent years. The US railroad industry has been through a significant period of consolidation following deregulation in 1980. The number of Class I railroads has fallen from more than 70 to just seven over this period. Rates for hauling freight are largely unregulated. Approximately 80% of freight is hauled under contract and these hauls are not overseen by the industry regulator, the Surface Transportation Board (STB). For the other freight movements where the STB does have oversight, it is incumbent upon the shippers to seek rate relief through rate cases (ie, the shipper needs to prove the railroad is charging unreasonable rates). US rail regulation relies on competition to prevent unreasonable rates, though in practice the railroads operate regional duopolies and the costs of seeking rate relief are often too high for shippers.

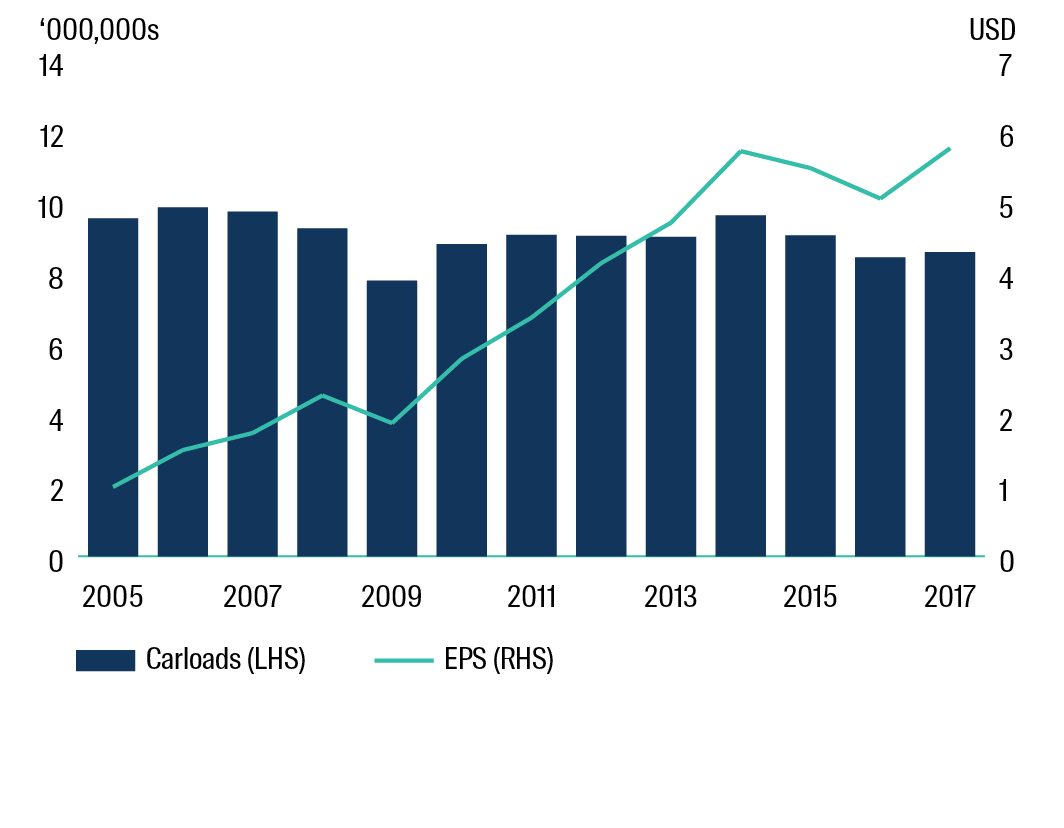

Strong demand has allowed Union Pacific to generate consistent core price increases of 2-4% pa in recent years and to fully pass-through many uncontrollable costs like diesel fuel. These price increases, combined with improvements in operational efficiency, have driven EPS growth despite broadly flat volumes. US railroads have consistently maintained price discipline and management teams at the railroads have guided for solid core price increases going forward.

Number of Class I railroads

Source: AAR. As at 31 December 2017.

Union Pacific volume and earnings increases

Source: Bloomberg, Union Pacific. As at 31 December 2017.

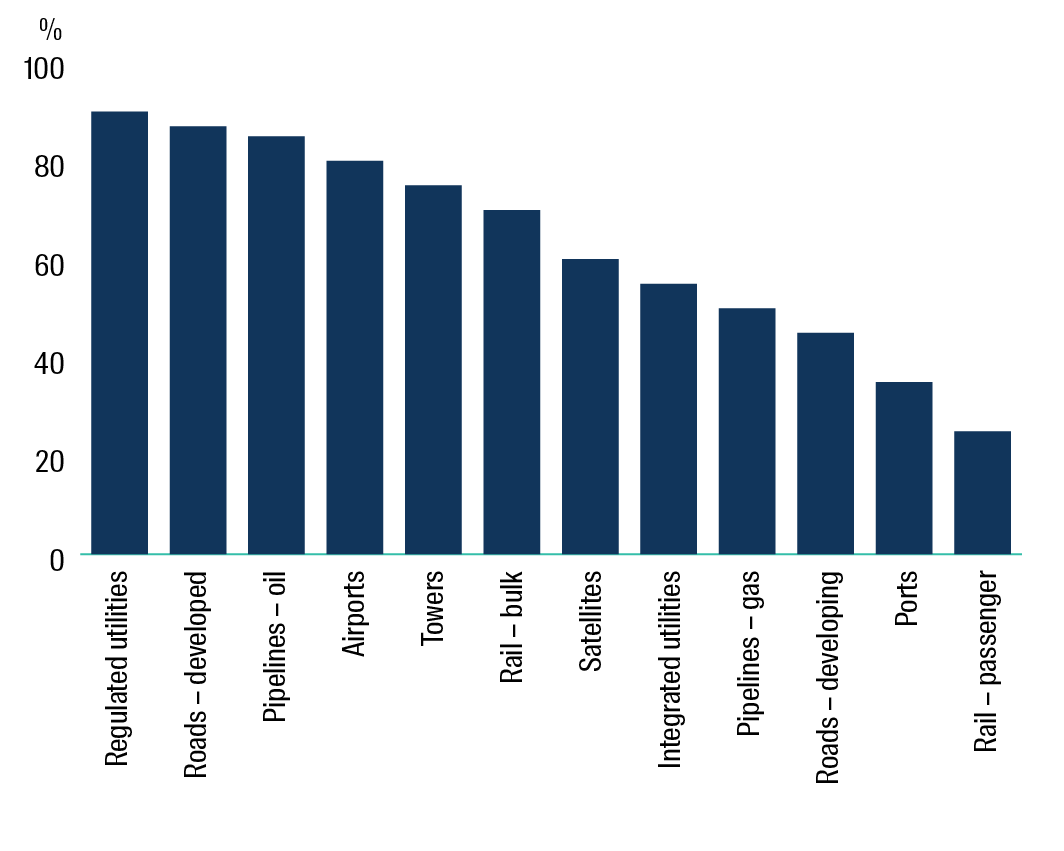

In summary, the degree of inflation protection varies by sector. Taking our focus list of around 120 listed infrastructure companies, including some of the examples outlined above, we have attempted to quantify the degree of inflation protection. The measure reflects our estimate of the proportion of the valuation that could reasonably be expected to recover inflation within a three-year investment horizon. It seeks to capture the theoretical relationships outlined above but also some of the practical risks discussed in the next section. Significant variances between outcomes in the same sector have been split, for example roads in developed vs developing countries, oil vs gas pipelines and bulk vs passenger rail.

Degree of inflation protection by sector

Source: First Sentier Investors. As at 31 December 2017.

Practical risks to the theoretical hedge

The infrastructure asset class covers a range of sectors and countries. Passively investing in the asset class does not guarantee a hedge to inflation and significant qualitative assessment is still required. The degree of inflation protection will depend on a number of factors and investors should look to address the following questions: Regulatory regime: Is the link to inflation explicit? Is the regulatory decision process transparent? What is the time lag between actual and recovered inflation?

As outlined in the previous section, there are various ways that inflation is captured in price increases. Regulated utilities and toll roads probably offer the clearest inflation protection, not only reflecting the explicit links in pricing formulas but also the long history and transparency of implementation in most countries. A lack of transparency is the key risk for investors in emerging markets infrastructure as highlighted in recent years by cuts in tariffs forced on China expressways and Brazilian power producers.

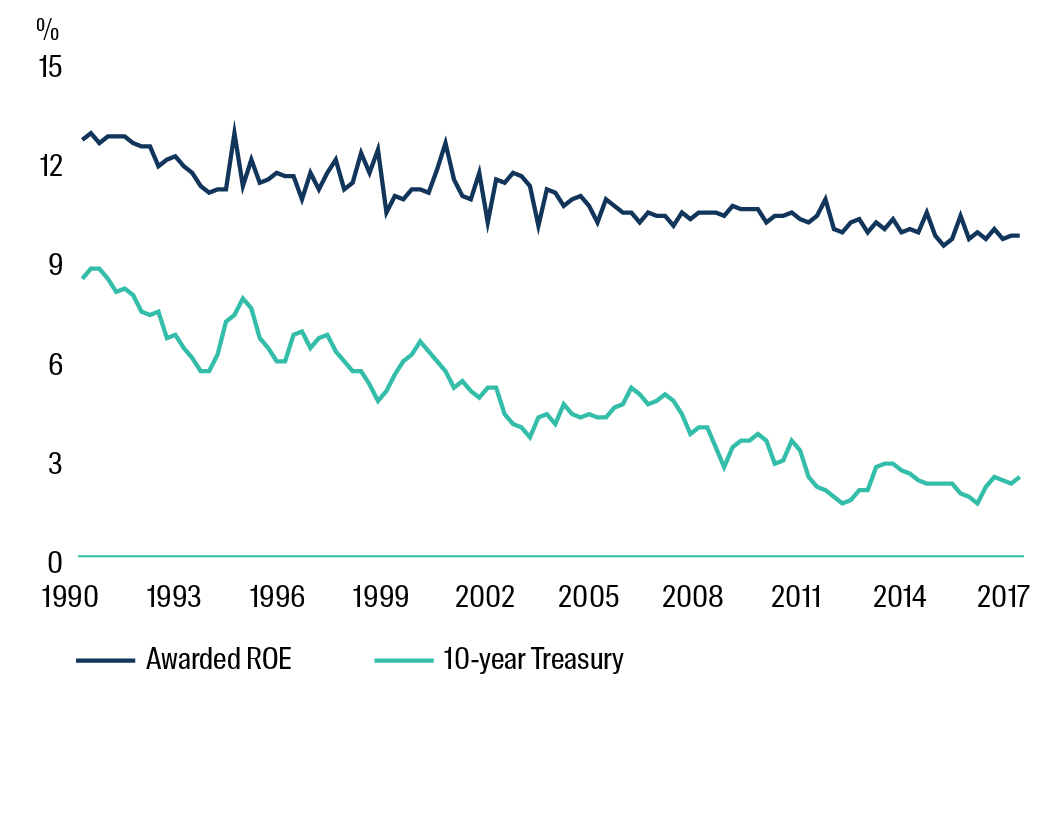

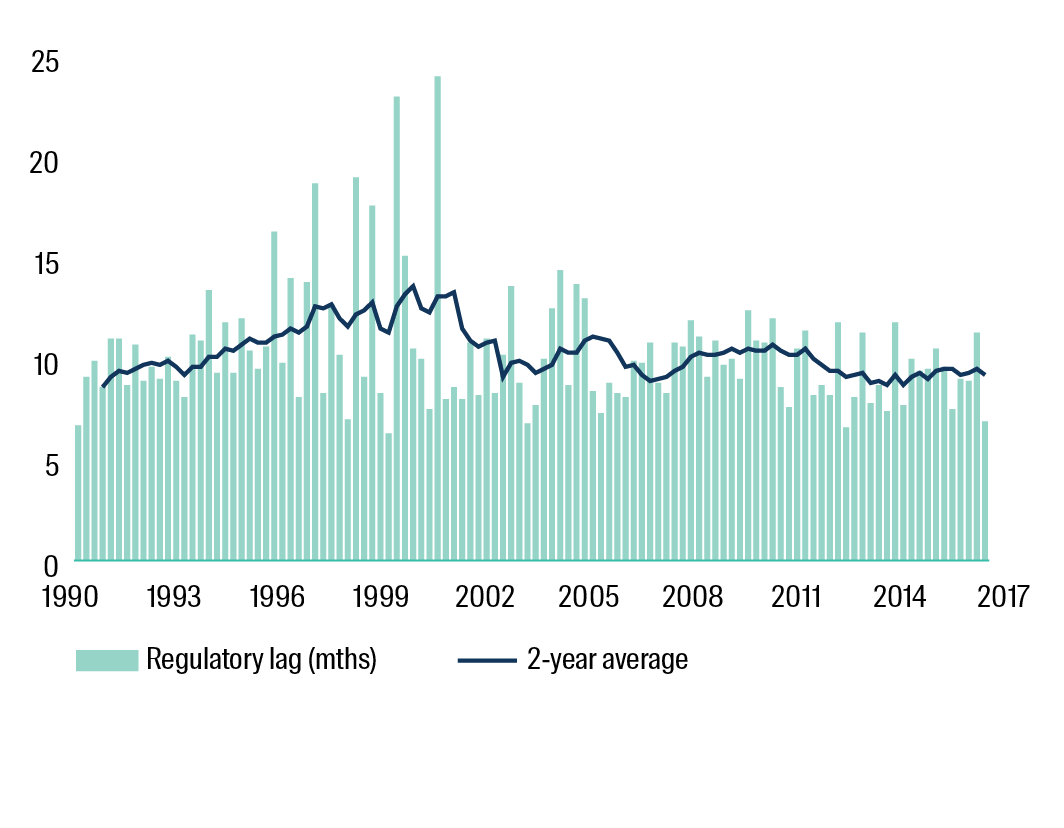

Generally US utilities do not offer explicit links to inflation but most regulators in the US have been sensible in their approach to rate cases. For example, awarded returns on equity for the industry have remained close to 10% despite the fall in risk free rates, regulators recognising that there needs to be a balance between consumer prices and utility investment. Regulatory lag (the time between rate cases being filed and awarded) has also remained below 12 months implying significant changes in cost inputs can be recovered in a reasonable time frame. This measure merits ongoing focus as investors do not want to return to the regulatory delays of the late 1990s.

US utility rate cases

Source: EEI, First Sentier Investors. As at 31 December 2017.

US utility rate cases

Source: EEI, First Sentier Investors.

As at 31 December 2017.

Political interference: Is the regulatory regime compromised by political bias? Can other regulatory inputs be adjusted to limit price increases? Can new taxes be levied without compensation? The risk of political interference has increased as leverage in the private sector has shifted to the public sector via government spending on bailouts and stimulus. Decisions taken by politicians including nuclear closures in Germany, renewable subsidy reductions in Spain, motorway and airport concession taxes in Italy, electricity and gas tariff freezes in France and port container handling tariff changes in China have already impacted investor returns.

The countries now facing the greatest challenges in meeting public spending requirements are likely to be the ones where investors face the greatest political risks. The safest returns are likely to come from infrastructure assets operating in stable political and legal systems, with customers that are corporations rather than voters.

Competitors and substitutes: What is the competitor response to price increases? Does a substitute become more viable? Consistent increases in price may trigger a competitive response in time. For most infrastructure sectors the barriers to entry provided by regulation, land availability or zoning laws make it very difficult to replicate existing assets or provide a reliable alternative. Some sectors do face a degree of competition and have to consider the response to price increases.

Port of Hamburg pushed pricing to a significant premium over competitors on the Northern Range because of its advantage accessing the hinterlands of Central and Eastern Europe. But this pricing was subsequently eroded as it encouraged Rotterdam and Antwerp to execute plans to double port capacity and improve intermodal links.

Freight rail operators including Union Pacific and Canadian Pacific in North America or Eurotunnel in UK/France face some substitution from trucks or ferries, particularly for shorter-haul intermodal. This threat diminishes at times when fuel costs are higher, due to the relative efficiency of rail as a mode of transport.

Variable costs: Are the revenue increases eroded by increases in operating costs like labour or fuel? Are interest costs fixed or variable? The capital intensive nature of the infrastructure sector means that depreciation and interest are usually the largest components of the cost base. EBITDA margins average 40-50% for the sector but can be as high as 80% for some roads, airports, regulated utilities and satellites. Many infrastructure companies operating on lower margins have reduced their exposure to variable costs by renegotiating contracts or introducing technology. For example, rail companies have renegotiated contracts with shippers to pass-through volatile diesel fuel costs while port companies have invested in automated gantries to lift containers, in some cases more than halving labour unit costs.

It is important for infrastructure companies to maintain an appropriate debt structure so that inflation-linked price increases flow through to the bottom-line. Experience has shown that inappropriate capital structures can override underlying asset quality and lead to poor equity performance. During the global financial crisis, some Australian infrastructure companies like Asciano and ConnectEast held excessive levels of gearing at more than 5x Debt/EBITDA or less than 2x EBITDA/Interest and were forced to raise equity. European integrated utilities, like Enel and Gas Natural, held a significant proportion of “acquisition bridging finance” and were not able to refinance at attractive rates Duration of investment: Does the investor holding period allow enough time for the underlying qualities of the asset to be reflected in equity returns?

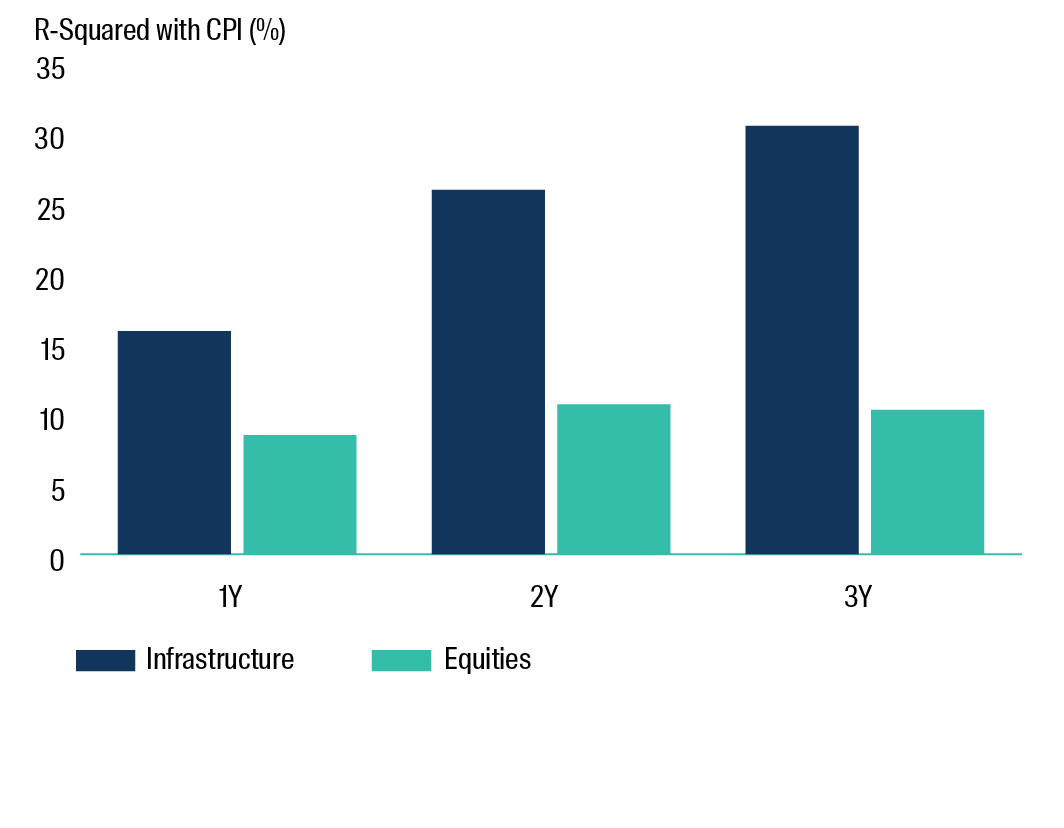

Listed markets offer liquid access to the infrastructure asset class but will not be immune to equity market volatility in the short-term. A regression of total returns against inflation highlights the importance of investing for the longer-term. That is, inflation can only explain 16% of the return on infrastructure over rolling 1 year periods but this rises to over 30% over 3 years. In contrast, inflation only explains 8% of the return for global equities over rolling 1 year periods, and this rises to just 10% over 3 years.

Inflation and infrastructure returns (3Y rolling)

FTSE Global Core Infra 50/50 Net TR (USD) from Dec-05, prev Macquarie Source: Bloomberg and First Sentier Investors. Quarterly time services from 2005-2017.

Total Returns explained by inflation

Infrastructure: FTSE Global Core Infra 50/50 Net TR Index (USD) from Dec-05, prev Macquarie Equities: MSCI Daily TR Gross World (USD)

CPI: US CPI Urban Consumers SA

Source: Bloomberg and First Sentier Investors.

Quarterly time series from 2002-2017

Conclusion

It remains important for investors to insulate their portfolios from the impact of inflation. Global listed infrastructure has delivered returns equivalent to CPI plus 10.1% over 15 years and outperformed global equities by almost 7% pa when inflation is above 4% pa. However, please do remember that past performance is not a guide to future performance. The analysis highlights that more than 70% of assets owned by listed infrastructure companies have effective means to passthrough the impacts of inflation, but significant qualitative assessment is still required.

Institutional investors looking to maximise inflation protection could consider an infrastructure portfolio with:

- Higher weights in regulated utilities, developed roads, oil pipelines, airports, mobile towers, bulk rail

- Lower weights in integrated utilities, developing roads, gas pipelines, ports, satellites, passenger rail

- Higher weights in US, UK, Australia, Canada, northern Europe

- Lower weights in southern Europe, Japan, Emerging Markets

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (Author). The Author forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for the Author is available from First Sentier Investors on its website.

This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are the opinions of the Author only and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product.

To the extent permitted by law, no liability is accepted by MUFG, the Author nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that the Author believes to be accurate and reliable, however neither the Author, MUFG, nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of the Author.