Livewire interviews Dawn Kanelleas and Michael Joukhador from our Small Companies team about their views on Australia's technology sector, the 'WAAAX stocks', and their high conviction investment positions.

Many of Australia’s listed technology companies including WiseTech Global, Afterpay Touch Group, Altium Limited, Appen and Xero (forming the WAAAX acronym) have seen significant share price performance

in recent years, with many investors suggesting that perhaps their valuations have been running ahead of business fundamentals. For others, these stocks offer significant revenue and profit growth for years to come and may therefore still look attractive. For us, our disciplined bottom up process leads us to assess each WAAAX stock on its individual merits.

While most WAAAX stocks have some attractive characteristics, we don’t consider every WAAAX stock an attractive investment. We have invested in the WAAAX companies with long term competitive advantages, sustainable and predictable earnings, excellent management and strong free cash generation. We take a long term view on value creation, seeking companies that have a disciplined growth strategy and a laser-like focus on their core market.

Our process gives us the opportunity to look past the short term valuation metrics if we can have confidence a business has the platform and management team to create a more valuable business on a medium and long term basis. What we are looking to identify, is a business that might look expensive on short term valuation metrics (like a one year forward price-to-earnings (PE) ratio[1]), but offer value in three to five years on the back of strong compound revenue and profit growth.

What are some of the things that investors on the other side of the trade fail to appreciate with these companies?

While high performance, high growth stocks are attractive to investors, the large PE ratios these names trade on can be unappetising, as investors are being asked to pay a price for future growth that may not eventuate. We believe investors often fail to appreciate the ability of an exceptional business run by exceptional people to continue to create long term value. Companies that are the market leaders within a sector can often leverage that market leadership, strong free cash flow, strong intellectual property (including staff) and pricing power to further grow market share. Operating leverage (and therefore profit margins) as revenues grow can often be underestimated.

In our view, the market can often overlook the importance of compound profit growth and how quickly the compounding of growth can lead to a change in company valuation metrics. To demonstrate, it’s worth observing that a company that can grow its earnings at a compound rate at 20% for 6 years will be 300% more profitable at the end of that period.

Of course, growth is often not free and comes with risk and also often requires significant capital deployment. For all of the upside, there is significant downside for investors if these companies fail to execute. It’s for this reason, we continue to stress the importance of a disciplined investment process that carefully assesses risk. The objective, is to identify those few great companies that offer the predicable long term growth that can justify the short term valuation measures.

Can you illustrate your bull or bear case for the next 3-5 years?

Two high performance growth stocks that we believe have long term competitive advantages, sustainable and predictable earnings, excellent management and predictable cash generation include Altium and Xero.

We believe Altium, the world leader in software that designs circuit boards, has an exceptional management team and a laser-like focus on its core market. In our opinion, there are very few businesses as well positioned to

benefit from the explosion of growth in connected devices and artificial intelligence as Altium. For every traditional device that is redesigned to talk to other devices – and for every new device brought to market – there sits an engineer heavily reliant on Altium (or competing software).

We like Altium because:

– It has quietly grown to become the market leader in the space and continues to drive significant market share gains.

– It has leveraged its strong market share and strong free cash flow into product development to drive further share gains and price growth.

– It has demonstrated a disciplined approach to investment to deliver excellent margin growth (highlighting the available operating margin as the revenue increases).

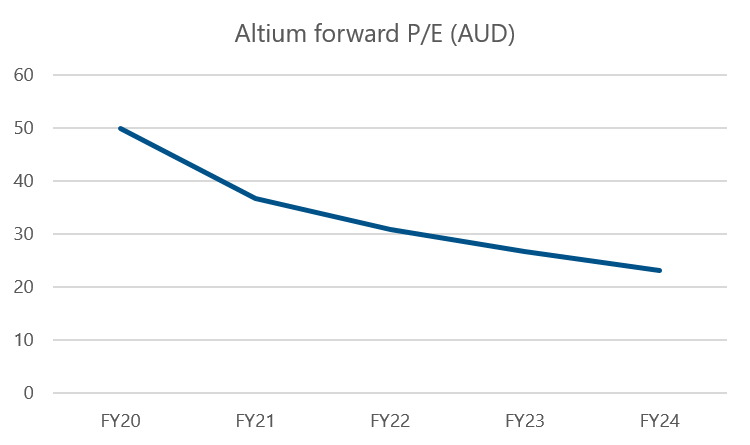

The half year result to end 2018, as a good example, demonstrated 24% revenue growth, margin expansion and 58% profit growth. While many investors would baulk at the PE multiple, we have been able to look through this short term valuation measure and focus on the significant value creation opportunity for the business over the coming three to five years.

These are expected earnings based on First Sentier Investors forecasts and are predictive in nature and therefore not guaranteed to occur. They may be affected by inaccurate assumptions, known or unknown risks and uncertainties and may differ materially from results ultimately achieved.

June year end. Source: First Sentier investors. Forecast data as at 4 June 2019. Shown in AUD terms.

[1] A company’s P/E Ratio is calculated by dividing its market value per share by its earnings per share. A relatively higher PE ratio than the market suggests investors are anticipating relatively higher future growth.

We hold a long term position in cloud-based accounting software provider Xero because we believe they offer a strong management team prepared to invest for the long term.

The business has built a globally scalable software that, in our opinion, is the most compelling offering in the markets in which it operates. Xero is in the enviable position of being able to leverage a recurring revenue base to cement its competitive advantage by driving investment in product development harder every year.

We would expect the Xero software suite to evolve over coming years to take full advantage of the Artificial Intelligence and Data Analytic macro trends. As an open platform, it will also be able to leverage third party applications to cement its competitive advantage. While it is very difficult to specifically articulate how and when such products might be commercialised, what we can do is identify the fact that Xero have the platform, the management and the vision to crystallise the available opportunity if it presents itself.

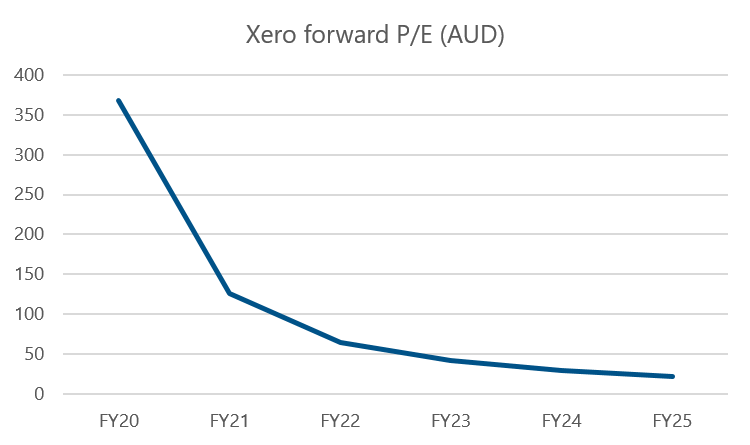

These are expected earnings based on Factset consensus forecasts and are predictive in nature and therefore not guaranteed to occur. They may be affected by inaccurate assumptions, known or unknown risks and uncertainties and may differ materially from results ultimately achieved.

March year end. Source: Factset consensus. Forecast data as at 4 June 2019. Shown in AUD terms.

Xero is in an excellent positon to offer investors both free cash flow generation and continued strong double digit revenue growth across the globe. The total addressable market is significant and good execution offers investors significantly larger margins and profit over the longer term. By example, Xero leveraged into the UK what started out as a New Zealand and Australian business. It is now the dominant accounting platform in the UK (a market three times larger than Australia and New Zealand’s) and has delivered strong subscriber growth over the last six months. Once again, focusing on short term valuation measures can distract from the significant value creation opportunity ahead for the business.

Important Information This material has been prepared and is issued by Colonial First State Asset Management (Australia) Limited AFSL 289017 ABN 89 114 194311 (CFSAMA). CFSAMA, forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG). This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product. To the extent permitted by law, no liability is accepted by MUFG, CFSAMA nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that CFSAMA believes to be accurate and reliable, however neither CFSAMA, MUFG nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of CFSAMA. In Australia, ‘Colonial’, ‘CFS’ and ‘Colonial First State’ are trade marks of Colonial Holding Company and are used by First Sentier Investors under licence. Copyright © CFSGAM Services Pty Limited 2019, (part for First Sentier Investors) |

All rights reserved.