Incorporated in 1885, BHP began as a silver, lead and zinc mine in Broken Hill, Australia. Over the next century the company grew into one of the largest diversified resource companies in the world with operations including oil and gas, steel production and mining of a variety of commodities including copper, potash, coal and diamonds. It listed on the Australian stock exchange in July 1961, making it the oldest company currently trading, and throughout much of this time it has been the largest company on the ASX by market capitalisation (currently it is ranked third).

In 2001 BHP announced it would merge with fellow resource powerhouse Billiton. Billiton also had a long history dating back to a single tin mine in 1851 before growing into a major producer of aluminium, alumina, chrome, manganese, steaming coal, nickel and titanium. The company was Dutch controlled from inception before being acquired by South African firm Gencor in 1994.

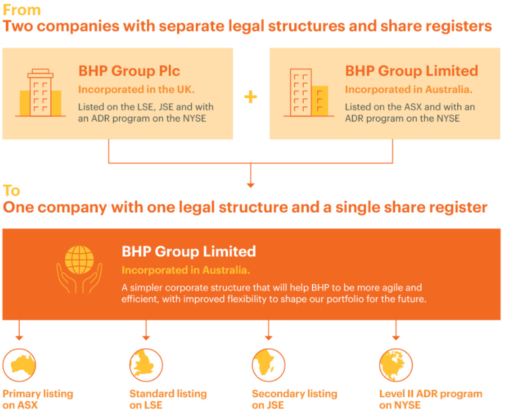

As the world’s largest metals and mining corporation, BHP Billiton began trading in July 2002 and operates as a dual listed company (DLC) – a corporate structure in which two companies have merged into a single operating business but retain separate legal identities and stock exchange listings (in this case Australia and the United Kingdom[1]).

The DLC was the most effective way at the time to execute the merger of two very large companies in different jurisdictions, however over the years it has frequently drawn confusion and criticism particularly as the business changed. Most notably in 2017 some institutional shareholders, led by US based Elliot Corporation (who held 5% of the company) began strongly advocating to collapse the DLC.

In August 2021 the company announced its intention to ‘unify’ or collapse the dual listing, consolidating into one company, BHP Group Limited, incorporated in Australia. This will see BHP Group PLC delist from the London Stock Exchange (LSE) in the UK and the shares transferred to the Australian ASX listing of BHP Group Limited.

This has impacts for both the composition of benchmark indices and the Realindex funds.

The changes proposed by the company

The picture below illustrates the proposed changes. Note that BHP will still trade in the UK but it will be a ‘cross listing’ of the Australian shares as is currently available via South Africa and the US.

BHP unification explained

Source: BHP Company Website, December 2021.

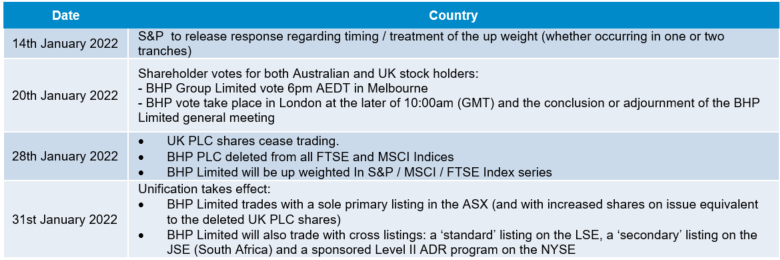

Key dates as released by the company and benchmark index providers are detailed below.

BHP unification timeline

Source: BHP Company Website, UBS, December 2021.

The benefits of ending the dual listing include:

1. Simplicity

Currently BHP has to adhere to both Australian and UK corporation laws and as such must duplicate a lot of functions e.g. produce 2 separate annual reports (and 1 consolidated), have 2 boards and hold 2 separate annual general meetings. Unification will result in these functions only being required once.

2. Flexibility

Dual listings make it difficult to use shares as consideration in mergers, in fact BHP has used cash in all its mergers and acquisition (M&A) activity since 2002 whereas scrip funding globally is over 40% for other Resource companies and 38% in the broader market2.

For example BHP has announced it will merge its petroleum business with Woodside Petroleum after unification to make it easier to complete as Woodside scrip will be issued to BHP shareholders.

3. Benefits of the DLC have been removed

In 2017 BHP resisted collapsing the DLC by claiming it would cost around US$1.7b. The company now claims costs will be around US$400m. The reduction is largely due to the removal of Australian corporate tax benefits that the company was receiving through the DLC structure (that allowed the paying of some tax in lower offshore jurisdictions).

4. Better use of Franking Credits

At the time of merging both companies contributed similar amounts to earnings. Since then due to asset sales, changes in commodity prices and the South32 demerger the UK assets now only produce 5% of the companies’ earnings. However under the DLC shares in both companies have equivalent economic interests in BHP Group. As a result since 2016 BHP Ltd. has had to pay fully franked dividends to BHP PLC. As BHP PLC is UK company, it cannot distribute Australian franking credits.

For example in FY21 BHP Ltd paid US$3.525bn in dividends with US$1.504bn in franking credits to BHP Plc, with these franking credits expiring within the DLC structure as they could not be passed onto non-Australian shareholders3.

As upon unification all BHP shares will be BHP Ltd shares and hence all dividends will be fully franked.

5. End of the difference in share prices between Australia and London

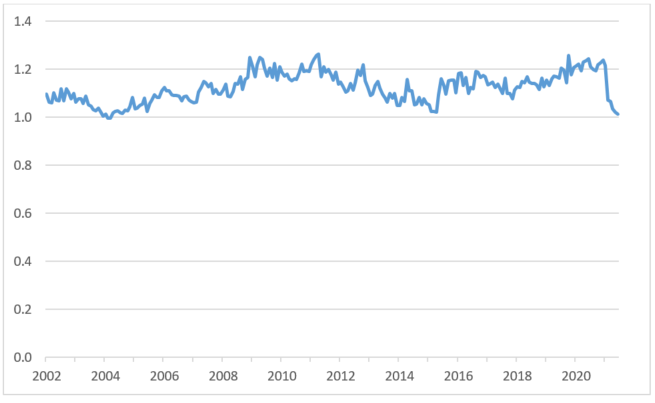

After merging in 2001 the 2 companies maintained two separate non-fungible listings which, after adjusting for currency, should have traded in line with each other given each company had the same economic and voting rights. However, except for a brief few months of parity in 2004 the Australian line has always traded at a premium to the UK line. Even more confusing is that the amount of this premium has varied significantly over time (as much as 25% in 2011) as can be seen in the following chart.

BHP listings (Australian listing / London listing)

Source: Factset. Data as at 31st December 2021.

Reasons for the pricing differences have never been clearly agreed upon but include the following reasons:

- The presence of franking credits in Australia

- Larger relative inflows into the ASX due to compulsory superannuation in Australia and a stronger Australian economy

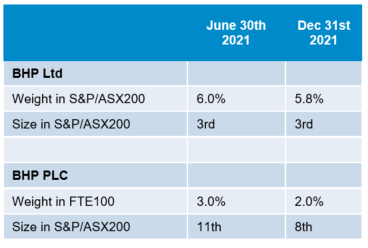

- BHP has a much larger weighting in the Australian equity market than the UK as shown the table below. This results in more buying by both passive funds and by active managers.

This share price differential has attracted more than its fair share of hedge fund activity with traders attempting to profit from change in the levels of the spread between the two listings, resulting in increased price volatility.

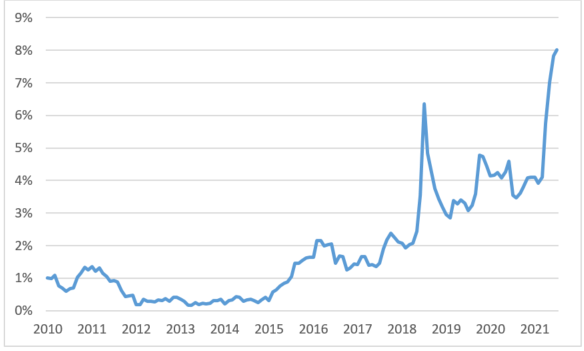

The chart above also shows this spread has continued to close since the August announcement but a different trade is now in play. Since announcement traders have heavily shorted the ASX-listed BHP shares and purchased up the cheaper PLC shares (which will convert to the ASX line on January 31st if the vote is successful). As the chart below shows short interest in BHP is currently at all-time highs (since data was available in 2010).

BHP short interest (Australian listing)

Source: Factset, ASX, Data as at 31st December 2021.

Dual listed structures fall out of favour

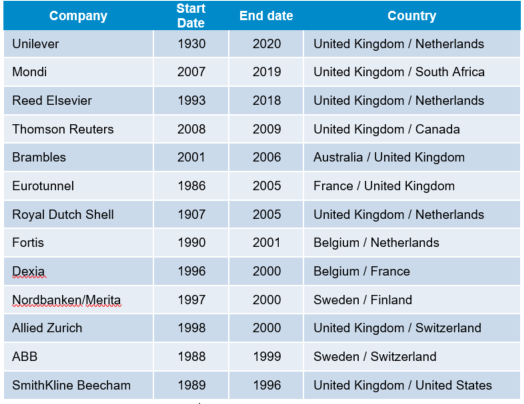

At their peak in the 2000’s there were up to 15 dual listed companies however only five (including BHP) currently remain as listed below.

Current dual listed companies

Source: Factset. Data as at 31st December 2021.

Previous DLCs are listed below. A common reason many have said for ending is that M&A such as scrip based acquisitions and demergers are more difficult to execute. For example as highlighted with BHP above DLC companies have used cash in 99.5% of their transactions4.

Previously dual listed companies

Source: Factset. Data as at 30th June 2021.

Impact on benchmark indices

Unification will result in a single Australian company with this listing only eligible for inclusion in the Australian benchmark indices (as index inclusion is based on country of domicile). As shown in the timeline earlier, if approved, MSCI and FTSE will delete BHP Group PLC and upweight BHP Group Limited in the respective indices as at close 28th January.

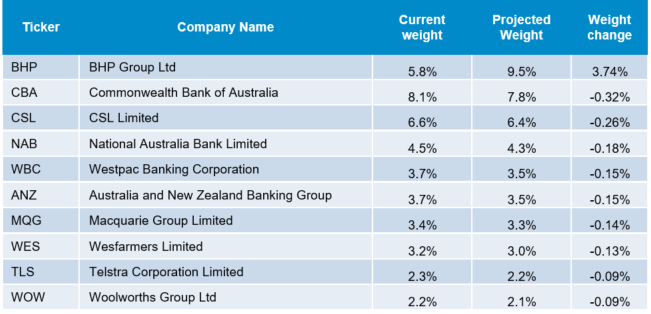

S&P will announce on 14th January whether they will make these changes in one or two tranches due to the large size of the upweight in the S&P/ASX200 and the amount of money benchmarked against this (and the S&P/ASX300) indices. As the table shows below (data from December 31st) BHP’s weight in the S&P/ASX200 will increase by 3.7% (from 5.8% to 9.5%) and it become the largest company in the benchmark. S&P estimate buying of BHP of $10.8 billion or around 34 days volume5 as in addition to required buying by passive funds many active managers will need to purchase the stock in order to maintain the size of their active positions.

If completed in one tranche it will also be done at close 28th January. Should S&P decide to split the changes over 2 tranches it is expected that a 50% upweight will occur on 28th January with the remaining upweight included with the quarterly March rebalance.

S&P/ASX200 – largest stock changes due to BHP upweight

Source: Realindex, S&P. Data as at 30th December 2021.

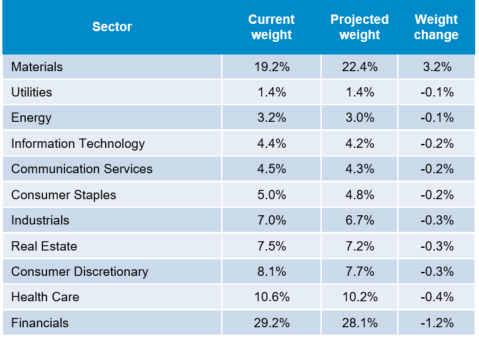

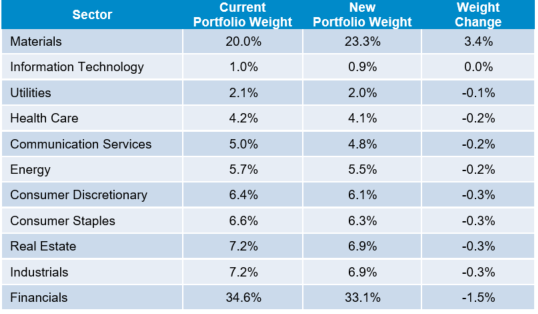

At a sector level Materials will increase by over 3% with the dominant Financials sector proportionally downweighted.

S&P/ASX200 – sector changes due to BHP upweight

Source: Realindex, Macquarie Research. Data as at 31st December 2021.

Impact on Realindex accounting weighted funds

Most quantitative investment strategies calculate signals on a per share basis (e.g. EPS rather than total Earnings). As the overall shares on issue for the company will not change such metrics will be unaffected.

Our accounting weighted fund weights however are constructed differently, using the entire reported metric (e.g. total reported dividends as opposed to reported dividends per share). As a dual listed structure has one set of accounts shared by two companies the Realindex process currently pro rates the accounting values between the two companies based on the amount of shares on issue in each country.

In the case of BHP Group as the table below shows currently 58% of the issued shares are listed in Australia. Hence this proportion is what is applied to the overall economic weight of BHP when currently calculating the portfolio weight in the Australian funds.

Our global funds exclude Australia hence hold BHP Group PLC with the 42% inclusion factor. (A global fund that includes Australia would hold proportionately both lines of the stock).

Portion of BHP listed in Australia and the UK

Source: Realindex, Factset. Data as at 30th December 2021.

After unification as all shares will be listed in Australia and BHP Limited will be like any other Australian company where 100% of the accounting value will be used to determine the portfolio weight.

As such the Realindex Global ex Australia funds will no longer hold the company (BHP Plc currently has a weight of 0.41%) whilst within our Australian portfolios a large upweight of the company similar in size to the benchmark will occur.

Largest stock changes post BHP unification – Australian share fund

Source: Realindex, Factset. Data as at 31st December 2021.

Aggregated to the sector level is shown below.

Sector changes post BHP unification – Australian share fund

Source: Realindex, Factset. Data as at 31st December 2021.

Will Rio Tinto be next?

Similar to BHP, Rio Tinto is also an Anglo-Australian multi-national resource company. It was formed as a dual listed entity in 1995 through the merger of Rio Tinto Zinc (a UK company) and the smaller Australian firm CRA Limited. The ratio of the listing has changed since 1995 due to shares buybacks in Australia reducing the shares on issue on the ASX as shown below.

Sector changes post BHP unification – Australian share fund

Source: Realindex, Factset. Data as at 30th December 2021.

Despite pressure on dual listed companies to simplify we would not expect Rio Tinto to unwind its DLC structure in the near term. This is because such an attempt would likely see it shift its primary listing to the UK, where 77% of the entity is listed (and hence a larger proportion of its shareholders). However a large portion of its profits come from Australia (due largely to record Iron Ore prices in recent years) and hence the majority of corporate tax is paid in this country. As such a move would likely see major pushback from both the Australian government and local shareholders.

The most recent comments from Rio Tinto management indicates they have no plans in the near term to follow in the footsteps of BHP.

Conclusion

When BHP and Billiton merged in 2001 the creation of the dual listing company was a creative and effective arrangement. However the changing nature of BHP since 2001 means this structure is now highly inefficient and costly (particularly in relation to Australian credits) whilst offering few advantages. Unification will provide a simpler corporate structure that will make BHP simpler and more agile for the future.

References

- The move of the primary listing of Billiton from South Africa to the UK is consistent with the actions of other South African companies such as Anglo American and SAB. Reasons cited included better base for expansion and a greater access to capital markets.

- Source: FTI consulting, 2017 based on M&A deals 1995-2017

- Source: Ownership Matters, January 2022

- Source: FTI consulting, 2017 based on M&A deals 1995-2017

- Source: S&P consultation paper, November 2021.

Important Information

This material has been prepared and issued by First Sentier Investors Realindex Pty Ltd (ABN 24 133 312 017, AFSL 335381) (Realindex). Realindex forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group.

This material is directed at persons who are professional, sophisticated or ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) (Corporations Act)) and has not been prepared for and is not intended for persons who are ‘retail clients’ (as defined under the Corporations Act). This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are the opinions of the Realindex only and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product.

The product disclosure statement (PDS) or Information Memorandum (IM) (as applicable) for those registered managed investment schemes mentioned herein that are managed by Realindex (Funds), which are issued by Colonial First State Investments Limited (ABN 98 002 348 352, AFSL 232468) (CFSIL), should be considered before deciding whether to acquire or hold units in the Funds. The PDS or IM are available from First Sentier Investors.

CFSIL is a subsidiary of the Commonwealth Bank of Australia (Bank). First Sentier Investors was acquired by MUFG on 2 August 2019 and is now financially and legally independent from the Bank. Realindex, MUFG, the Bank and their respective affiliates do not guarantee the performance of the Fund(s) or the repayment of capital by the Fund(s). Investments in the Fund(s) are not deposits or other liabilities of MUFG, the Bank nor their respective affiliates and investment-type products are subject to investment risk including loss of income and capital invested.

To the extent permitted by law, no liability is accepted by MUFG, Realindex, the Bank nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that Realindex believes to be accurate and reliable, however neither Realindex, MUFG, the Bank nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of Realindex.

In Australia, ‘Colonial’, ‘CFS’ and ‘Colonial First State’ are trade marks of Colonial Holding Company Limited and ‘Colonial First State Investments’ is a trade mark of the Commonwealth Bank of Australia and all of these trade marks are used by First Sentier Investors under licence.

Total returns shown for the Fund(s) are gross returns and do not take into account any ongoing fees. No allowance has been made for taxation. Past performance is no indication of future performance.

Copyright © First Sentier Investors (Australia) Services Pty Limited 2022

All rights reserved.