At AlbaCore, we focus on the long-term. As one of Europe’s leading alternative credit specialists, we invest in private capital solutions, opportunistic and dislocated credit, and structured products.

Discover moreInvestment strategies

Insights

Specialist in Asia Pacific, Japan, China, India and South East Asia and Global Emerging Market equities.

Discover moreOur philosophy is very simple. We are constantly searching for high quality businesses and when we acquire them, we will work relentlessly with them to create long-term sustainable value through innovation, ESG-led and proactive asset management.

Discover moreInvestment strategies

Insights

formerly Realindex Investments

Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreInvestment strategies

Insights

At Stewart Investors, we believe in putting people first. Our investment world-view is of a series of partnerships – with each other, with our clients, with the companies we invest in, the people who buy their goods and services, and with the wider society in which we all live and work.

Discover more

After appreciating in 2021, corporate bonds have struggled in the first half of 2022. Corporate credit fundamentals still appear reasonably favourable, but corporate bond prices have declined owing to the prospect of rising borrowing costs in key regions and an increase in geopolitical risk. These developments have clouded the outlook and investors have understandably reined in their risk appetite.

For the two years or so following the initial Covid shock, credit spreads traded below their long-term average – this was a tailwind for the asset class and pushed corporate bond valuations higher. Sentiment was buoyed by the prospect of a post-pandemic boost to economic activity levels and corporate profitability, as well as the support of central banks; some of which were buying corporate bonds directly as part of their quantitative easing programs.

But the increasing default risk being priced into corporate bonds in the year to date – and the resulting negative returns from credit markets – means we are now being questioned again whether credit markets still offer value for long-term, income-oriented investors. With corporate bond valuations now back almost exactly in-line with their long-term average, now seems an opportune time to answer that question.

In this paper, we consider whether there’s a cyclical case for investing in credit markets at this point, with valuations where they currently are.

As we learned in our research paper The Structural Case for Global Credit, the performance of credit securities is cyclical in nature. Fluctuations in credit spreads will always be a feature of the market, but we don’t believe should be concerning for investors as long as default risk remains manageable. This is because credit valuations generally gravitate towards the par value as bonds approach maturity and as the perceived risk of owning the credit security falls.

During their life, conventional market theory suggests credit securities will perform well during periods of economic expansion, and less well as the economic cycle matures. Deciding whether now is a good time to make a new allocation to the credit market– or to maintain existing exposure – might therefore depend on investors’ views of where we are in the cycle.

Deconstructing credit spreads

Credit spreads compensate investors for various risk factors, but liquidity, default risk, and ratings migration risk are arguably the most important. With that in mind, it’s worth considering each of these four drivers individually to see how they might affect valuations in the remainder of 2022 and beyond.

Liquidity

Part of a credit security’s yield premium over comparable government securities compensates investors for liquidity risk – the prospect of buyers disappearing when investors want to sell their holdings. This phenomenon reared its head during the Global Financial Crisis in 2008 when, for a period, it was challenging to trade credit securities at any price. Liquidity dried up again in March 2020 during the Covid shock, although it recovered quite quickly.

Demand levels are mixed currently. Trading volumes in secondary markets were quite buoyant during 2021, but have moderated in the calendar year to date. We are keeping a close eye on fund flows in the sector, to see whether the negative trend in recent weeks worsens. It appears that some investors have become un-nerved by the negative returns from fixed income and credit markets over the past few months. In our view, redemptions are not too concerning at current levels, but any more severe and prolonged outflows from the asset class could impede valuations.

Default risk

A higher risk of default is arguably the most obvious reason why credit securities offer yields above comparable government securities. It also helps explain why credit spreads have widened in the first half of this year; the probability of rising borrowing costs and an increase in geopolitical risks – most notably the war in Ukraine – means investors have become more concerned about possible defaults. The concern is understandable, as corporate failures can result in permanent capital impairment and can erode returns from corporate bond portfolios. Ultimately, default risk is ever-present in credit markets, irrespective of the economic cycle and the anticipated performance of individual firms.

Persistently high inflation and rising interest rates arguably present the greatest risk for companies currently. Inflation remains well above target levels in almost all major regions and central banks are responding by raising official interest rates. Higher borrowing costs will undoubtedly be a headwind for some firms. Interest coverage – a measure of how comfortably companies can service their debt repayment obligations – could deteriorate if not actively managed by issuers and it’s plausible we could see a pickup in default rates over time.

This scenario underlines the critical importance of thorough credit research and ongoing monitoring. We are fortunate to have an experienced, in-house team of specialist credit analysts – their job is to relentlessly monitor the creditworthiness of issuers to detect early signs of financial stress. The intention is always to remove deteriorating companies from portfolios before default risk starts to be reflected in valuations.

Winners and losers

It’s important to note that higher interest rates will not affect all companies uniformly. As ever, there will be winners and losers in this environment. As well as assessing evolving risks for companies, our credit analysts are tasked with identifying which issuers might benefit from high inflation and rising interest rates. Some financial firms may be able to raise their margins in a higher interest rate environment, for example. Companies in other sectors that are able to pass through higher costs to consumers, and which are least exposed to rising commodity prices, might also fare well relative to the broader credit sector. We always seek to avoid concentration risk and seek a high level of diversification in portfolios at all times, but it’s still possible to minimise exposure to ‘at-risk’ areas of the market.

The most highly leveraged firms are often most at risk from higher borrowing costs. Selected Chinese property firms are a good current example. In some cases, these firms have struggled to refinance existing debt and have defaulted on existing securities, unable to source the cash to repay bondholders. There has been something of a domino effect in the sector; once one large developer defaulted, investors became increasingly concerned about the creditworthiness of others. In turn, credit spreads widened and valuations fell sharply owing to the increase in perceived risk. The limited availability and increased cost of new debt can result in a liquidity event, whereby even the most solvent companies can default. This phenomenon can result in default ‘clusters’, whereby several issuers in the same market segment default around the same time. Losses of capital can be significant in these environments. Consequently these are the kinds of firms and situations we identify and aim to avoid through the credit research process.

Some other firms are being hindered by issues in global supply chains. Most notably, Covid-related disruptions in China are affecting the availability of a wide range of products. Car makers, for example are struggling to produce enough vehicles to keep pace with demand owing to a shortage of computer chips and other componentry. Similarly the war in Ukraine is resulting in shortages and supply chain bottlenecks for some products in Europe, and skyrocketing energy prices are clouding the outlook for profitability among firms with energy-intensive production processes.

We are selective on geographic exposure too. The timing and extent of interest rate hikes will vary, affecting borrowing costs in different countries and regions. Interest rates are currently being raised very aggressively in the USA and New Zealand, for example, and more modestly in Europe.

Other factors affect geographic tilts too. Whilst interest rates remain lower in Europe than elsewhere, our portfolios are currently cautiously positioned in the region and we are remaining patient before adding any more risk here. Ukraine-related tensions remain unpredictable and energy costs are soaring. Additionally, it remains to be seen how credit spreads in Europe will behave when the European Central Bank ceases its quantitative easing program and stops buying corporate bonds on the open market. The central bank has been supporting credit markets in the region since the Covid-induced market dislocation, a process that has meaningfully changed the supply/demand dynamic in the local credit market over the past two years or so. Accordingly, there is a risk of some weakness when this very large, price-insensitive buyer withdraws from the market.

Ultimately, with credit valuations always fluctuating, there is scope for active managers to allocate strategically to regions and sectors where valuations are most attractive from a risk/return perspective.

Overall, default rates are expected to remain relatively low

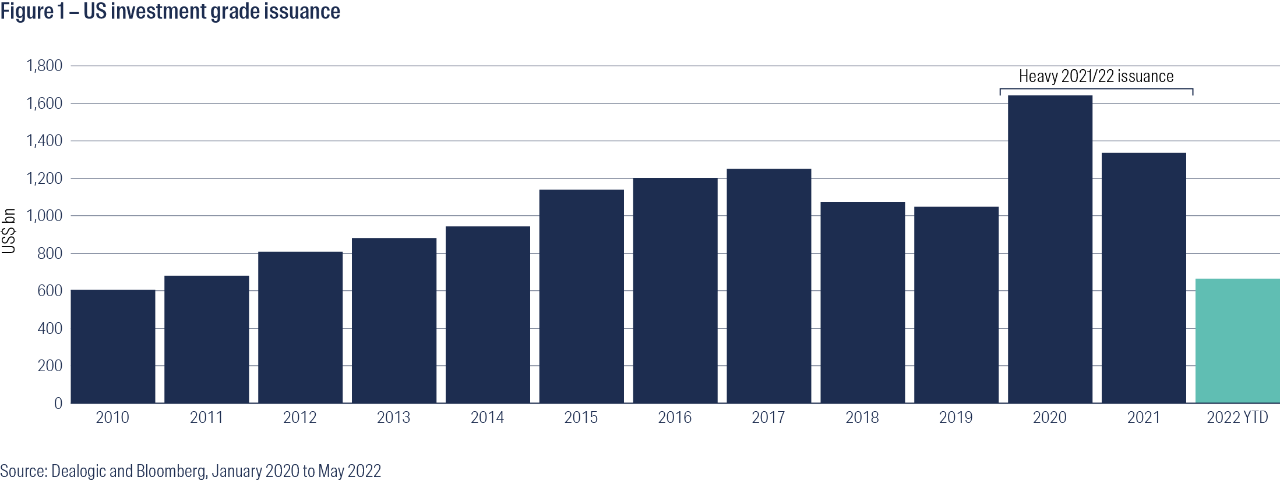

Despite an expected uptick in defaults over time, our analysis indicates that overall default rates in the market will remain below long-term averages. Higher borrowing costs will only really affect firms when existing bonds mature and need to be refinanced, or when companies look to issue new bonds to raise fresh capital. Importantly, many firms locked in long-term financing at very attractive borrowing costs over the past two years.

Figure 1 below clearly highlights the spike in issuance levels over the past two years.

Importantly, these low repayment costs are locked in for the life of the bonds, meaning higher official interest rates are not an immediate concern for some companies. Moreover, the recent trend in corporate bond issuance has been towards longer-dated securities. Whereas once the average duration – or life – of corporate bonds was around eight years, it has recently increased to between nine and ten years1. In other words, firms are coming to market for refinancing less frequently and many will not need to do so for many years.

In general, this provides us with some reassurance and suggests current credit spreads more than compensate investors for default risk. In turn, and in our view, global credit should continue to generate excess returns over comparable government bonds, as it has in eight of the past ten years (refer back to Figure 5 in The Structural Case for Global Credit research paper).

Ratings migration

The operational and financial performance of a firm, and its ability to service its debt repayment obligations, can result in upgrades or downgrades to credit ratings over time. This is known as ratings migration. A corporate bond currently rated ‘A-’, for example, might be upgraded to ‘A’ if the firm is performing well, or could be downgraded to ‘BBB+’ or lower if the outlook for profitability deteriorates. These ratings are important; they are an indication of default risk and therefore influence the cost of debt when new bonds are issued. In general, the lower the credit rating, the higher the yield required to attract investors.

In recent months we have seen quite an encouraging trend towards credit rating upgrades by independent rating agencies, like Moody’s and S&P. Low debt repayment costs on debt secured during the prolonged period of record low interest rates, combined with an upturn in revenues after Covid-related restrictions were eased in key regions, has supported company profitability and improved the creditworthiness of most firms. That said, there is certainly no room for complacency and we are mindful of the risk of a reversal in the upgrade cycle if conditions deteriorate.

The ongoing appeal of credit for long-term, income-oriented investors

As a result of higher risk-free rates and the recent uptick in credit spreads, ‘all in’ yields from credit are currently sitting around 4.3%2; the highest level for around five years. This is providing an increased risk/return payoff for credit investors and should help support the appeal of the asset class among long-term, income-oriented investors, particularly as the fundamental backdrop remains broadly supportive of credit as we have explained. To recap, our research shows most corporates remain well capitalised having raised ample capital at historically low borrowing costs over the past two years or so. In general, we believe interest coverage will remain comfortable for most firms. Accordingly, unless we see a more pronounced slowdown in major economies, default risk appears manageable in most areas of the market.

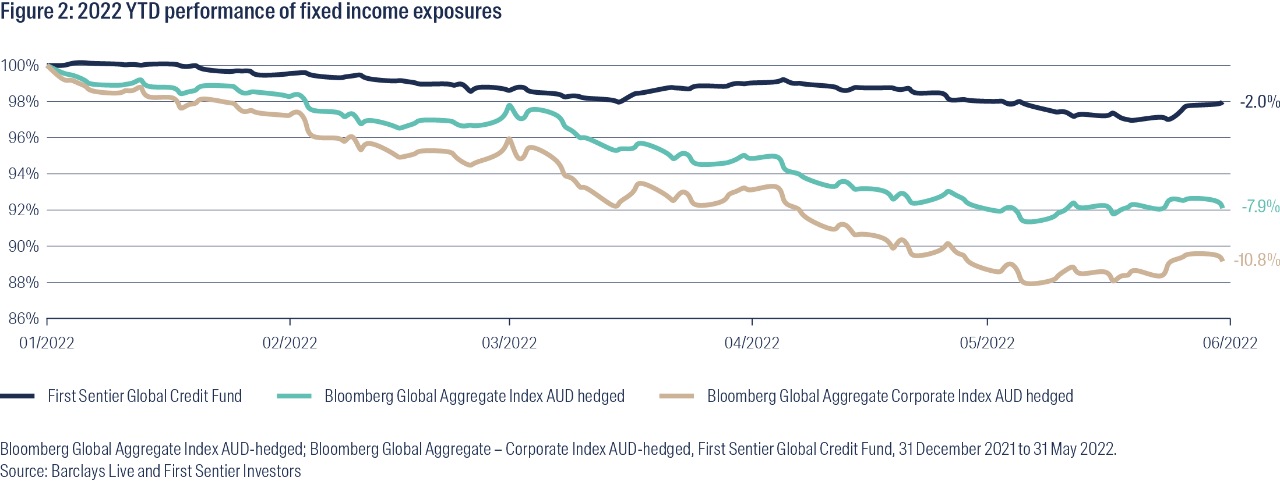

Finally, it’s important to understand how movements in government bond yields are affecting performance outcomes in fixed income portfolios, including fixed and floating rate credit products. The very sharp upward move in government bond yields worldwide has hampered the performance of traditional, aggregate style fixed income benchmarks like the Bloomberg Global Aggregate Index, outlined in dark blue in Figure 2 below.

Traditional fixed rate credit benchmarks – marked in grey – are down even more sharply in the calendar year to date. Volatility in credit spreads has been unhelpful, but most of the negative performance impact is attributable to higher Treasury yields.

In comparison, the performance of credit products with floating rate benchmarks – like the First Sentier Global Credit Fund – has been much better, as they are not directly affected by changes in government bond yields.

Even more importantly, the performance of floating rate credit products will remain largely unaffected by future movements in government bond yields. This is important to bear in mind given the possibility of even higher government bond yields if inflation remains elevated and if central banks respond by tightening policy settings more significantly.

Risks to the investment thesis

Before wrapping up, and in the interests of a balanced view, it’s worth looking at some of the factors that could prompt a change in our cautiously optimistic view.

A sharp downturn in economic growth

For now, the International Monetary Fund is forecasting global GDP growth of 3.6% for both this year and next3. If these projections prove accurate, credit could fare reasonably well. Corporate bonds have historically performed well in ‘goldilocks’ economic environments, where growth is not too hot, but not too cold either.

That said, credit markets could start to look expensive if economic growth falters. This is plausible if central banks tighten policy settings too aggressively and/or too quickly, triggering sudden and meaningful slowdowns in activity levels across most industry sectors. Further lockdowns owing to future strains of the Covid virus also cannot be ruled out, nor can an intensification of geopolitical tensions. The war in Ukraine, for example, could conceivably spill over into other parts of Europe – this would likely have a very damaging influence on the performance of risk assets globally, including credit.

Higher leverage

As we have seen with issues in the Chinese property sub-sector, leverage is an important metric for credit issuers. Increases can result in credit rating downgrades and, during periods of market stress, can pre-empt an increase in defaults.

Companies – certainly in the financials sector – appear to have learned lessons from the Global Financial Crisis and have lowered their leverage over the past decade or so. Nonetheless, there is always a risk that companies take on higher debt levels and stretch their balance sheets.

Any meaningful increase in borrowing levels and leverage would therefore be a red flag, as it could see spreads widen further and impede returns from the asset class.

More than two decades of expertise

First Sentier Investors has been constructing credit funds for more than 20 years, so we have the expertise and know-how to manage investment risks over the full credit cycle. Whilst we are always looking for value-adding opportunities within the asset class, we believe First Sentier Investors is among the most conservative credit investors in the Australian peer group.

Ultimately, we are mindful that a credit allocation sits within the defensive component of most investors’ portfolios, and is intended to provide some offset to potential volatility in growth assets. Accordingly, capital preservation is of paramount importance in our Global Credit strategy.

We invest a lot of time and energy researching issuers and monitoring their performance, to help detect any early signs of stress. The intention is to remove deteriorating issuers from portfolios before valuations are meaningfully affected. Responsible investment considerations also form an important component of the research and investment processes. Environmental, Social and Governance risks and how they are being managed by issuers help influence the assignment of internal credit ratings, which in turn drive portfolio construction decisions.

Want to know more?

If you’re considering an allocation to Global Credit, speak to your account manager to see whether First Sentier Investors’ Global Credit strategies might be suitable for you.

Our over-arching credit investment philosophy has been largely unchanged for more than two decades and has stood the test of time. Our Global Credit strategies have performed broadly in line with expectations over full credit cycles, capturing the credit premium available whilst avoiding permanent capital impairment, i.e. defaults.

The Global Credit strategy offers:

- A proven and differentiated investment philosophy: Since credit market returns are asymmetric, we focus on avoiding the losers through rigorous credit analysis, combined with sophisticated portfolio construction that’s focused on diversification.

- Consistent long-term performance track record: Favourable risk-adjusted returns generated over multi-year time horizons*.

- Multi-dimensional credit research: A proven credit research process focusing on assessing credit risk and identifying deteriorating issuers early.

- Best-in-class ESG integration: ESG risk factors are an important consideration in the assignment of credit ratings on individual issuers, which in turn drive portfolio construction decisions.

*Past performance is not indicative of future performance.

References

1 Duration of the Bloomberg Global Aggregate – Corporate Index. Source: Bloomberg, 16 June 2022

2 Source: Bloomberg, 31 May 2022

3 International Monetary Fund World Economic Outlook, April 2022

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (FSI AIM), which forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for FSI AIM is available from First Sentier Investors on its website.

This material is directed at persons who are ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) (Corporations Act)) and has not been prepared for and is not intended for persons who are ‘retail clients’ (as defined under the Corporations Act). This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation.

The product disclosure statement (PDS) or Information Memorandum (IM) (as applicable) for the First Sentier Global Credit Fund (ARSN 094 088 454) (Fund), issued by The Trust Company (RE Services) Limited (ABN 45 003 278 831, AFSL 235150), should be considered before deciding whether to acquire or hold units in the Fund(s). The PDS or IM are available from First Sentier Investors.

MUFG, FSI AIM, their respective affiliates and any service provider to the Fund do not guarantee the performance of the Fund or the repayment of capital by the Fund. Investments in the Fund are not deposits or other liabilities of MUFG, FSI AIM, their respective affiliates or any service providers to the Fund and investment-type products are subject to investment risk including loss of income and capital invested.

Any opinions expressed in this material are the opinions of the individual author at the time of publication only and are subject to change without notice. Such opinions: (i) are not a recommendation to hold, purchase or sell a particular financial product; (ii) may not include all of the information needed to make an investment decision in relation to such a financial product; and (iii) may substantially differ from other individual authors within First Sentier Investors.

To the extent permitted by law, no liability is accepted by MUFG, FSI AIM nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that FSI AIM believes to be accurate and reliable, however, neither MUFG, FSI AIM nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of FSI AIM.

Any performance information has been calculated using exit prices after taking into account all ongoing fees and assuming reinvestment of distributions. No allowance has been made for taxation. Past performance is not indicative of future performance.

Copyright © First Sentier Investors

All rights reserved.

|  |

|---|